Gatekeeper of the financial system

;%20}%20.cls-2%20{%20fill:%20url(%23linear-gradient-2);%20}%20.cls-3%20{%20fill:%20url(%23linear-gradient-4);%20}%20.cls-4%20{%20fill:%20url(%23linear-gradient-5);%20}%20.cls-5%20{%20fill:%20url(%23linear-gradient);%20}%20%3c/style%3e%3clinearGradient%20id='linear-gradient'%20x1='8.089'%20y1='-4.628'%20x2='8.089'%20y2='17.703'%20gradientTransform='matrix(1,%200,%200,%201,%200,%200)'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20offset='0'%20stop-color='%23005eff'/%3e%3cstop%20offset='1'%20stop-color='%2300b2ff'/%3e%3c/linearGradient%3e%3clinearGradient%20id='linear-gradient-2'%20x1='12.007'%20x2='12.007'%20xlink:href='%23linear-gradient'/%3e%3clinearGradient%20id='linear-gradient-3'%20x1='12.007'%20x2='12.007'%20xlink:href='%23linear-gradient'/%3e%3clinearGradient%20id='linear-gradient-4'%20x1='15.926'%20x2='15.926'%20xlink:href='%23linear-gradient'/%3e%3clinearGradient%20id='linear-gradient-5'%20x1='12'%20x2='12'%20xlink:href='%23linear-gradient'/%3e%3c/defs%3e%3cpolygon%20class='cls-5'%20points='6.413%209.134%206.413%2015.125%209.765%2012.129%206.413%209.134'/%3e%3cpath%20class='cls-2'%20d='M12.492,13.663c-.302,.255-.747,.248-1.04-.018l-.698-.632-3.062,2.737h8.631l-3.062-2.737-.769,.649Z'/%3e%3cpolygon%20class='cls-1'%20points='16.613%208.25%207.402%208.25%2012.007%2012.366%2016.613%208.25'/%3e%3cpolygon%20class='cls-3'%20points='17.601%2015.125%2017.601%209.134%2014.25%2012.129%2017.601%2015.125'/%3e%3cpath%20class='cls-4'%20d='M19,2H5c-1.66,0-3,1.34-3,3v14c0,1.66,1.34,3,3,3h14c1.66,0,3-1.34,3-3V5c0-1.66-1.34-3-3-3Zm0,14.08c0,.51-.41,.92-.92,.92H5.92c-.51,0-.92-.41-.92-.92V7.92c0-.51,.41-.92,.92-.92h12.16c.51,0,.92,.41,.92,.92v8.16Z'/%3e%3c/svg%3e)

Our purpose, Banking for better, for generations to come, guides us in everything we do. We want to be a reliable and trustworthy bank for our clients and society. To this end, we do our utmost to safeguard the financial system from financial crime. As a gatekeeper of the financial system, ABN AMRO aims to prevent, detect and respond alertly to financial crime risks. We are strongly committed to this role and are aware of the high standards society expects us to live up to.

Continuously improving the bank’s functioning as gatekeeper

Taking ownership and setting clear targets are key elements of combating money laundering and of our licence to operate – as are risk management and compliance. We are fully committed to our moderate risk profile and to our role as a gatekeeper of the financial system. Our culture and licence to operate are clear priorities for us.

To ensure the bank properly fulfils its gatekeeper role and complies with all regulations and internal rules, ABN AMRO has put in place a ‘three lines of defence’ model across the organisation. This model sets out a clear relationship between risks and the different internal control functions, and provides clarity for all ABN AMRO employees on their risk management responsibilities.

Challenges & Ambitions

On 25 September 2019, the Dutch Public Prosecution Service (DPPS) informed ABN AMRO that it had started an investigation into whether the bank had fulfilled its obligations under the Dutch Act on the prevention of money laundering and financing of terrorism (Wwft). ABN AMRO is cooperating fully with the authorities. ABN AMRO has accepted a settlement offerfrom the DPPS to pay a fine of EUR 300 million and EUR 180 million as disgorgement in connection with the identified shortcomings in its Client Life Cycle processes.

In 2014, ABN AMRO started implementing several remediation programmes in multiple business lines. Since 2019, ABN AMRO has been running an extensive bank-wide programme to remediate shortcomings in its processes designed to prevent, detect and respond to financial crime (Client Life Cycle processes). We expect to complete this programme by theend of 2022 and will continue to strengthen our Client Life Cycle processes going forward.

Future-proof detection, countering and prevention of financial crime

On 1 January 2019, ABN AMRO centralised its Anti-money laundering (AML) / Combating Terrorism Financing (CTF) activities in the Netherlands in the Detecting Financial Crime (DFC)department. DFC aims to detect, counter and prevent financial crime, including money laundering, terrorism financing, tax evasion and the circumvention of economic sanctions.

The DFC department (to which ABN AMRO has currently dedicated over 10% of its staff) aims to strengthen ABN AMRO's processes to get a full picture of:

The client we are doing business with (activity known as KYC – Know-Your-Client). For this, group-wide programs are established to realise that client data is up-to-date, standardized and of sufficient quality to be used to efficiently and effectively execute transaction monitoring and client filtering process.

How each client uses our products and services. For this, client profiles and transaction patterns are benchmarked against the pattern of standardized profiles to show standard usage of the bank’s products and services.

How to recognize when clients (attempt to) misuse the bank’s products and services for criminal purposes (activity known as ongoing due diligence). For this, ABN AMRO experts increasingly also engage with other organizations such as the police, FIU, FIOD, universities, non-governmental organizations, and other financial institutions to pool and increase the shared knowledge on financial crime. The end goal is to design and adopt smarter detection solutions and to raise the field for safeguarding the integrity of the financial system.

Detecting financial crime approach

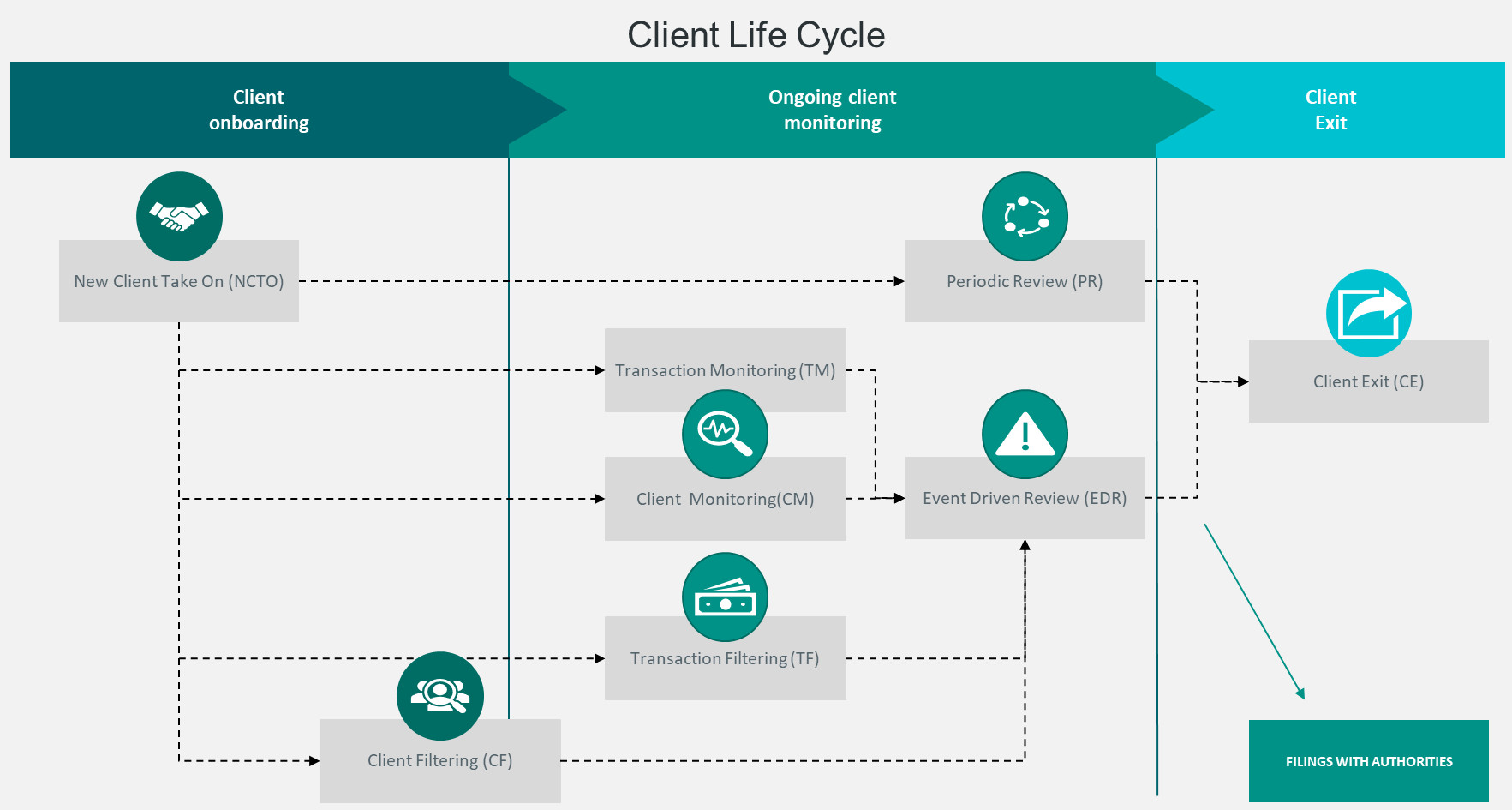

ABN AMRO is aware that serving over 5 million individuals and businesses exposes the bank to the risk that our products and services will be abused to facilitate financial crime. We manage these risks through fact-based management information and a continuous assessment of potential vulnerabilities and unknowns, supported by data. In accordance withregulatory requirements, we monitor the risks of money laundering, terrorism financing, bribery and corruption to maintain a strong control system and to mitigate these risks. We call this comprehensive set of procedures and controls the 'Client Life Cycle':

Process of the client life cycle in our AML/CFT programme.

Our people – the actual gatekeepers

Our employees are key in enabling us to fulfil our role as a gatekeeper, protecting the integrity of the financial system. Every day we monitor transactions and clients to prevent the abuse of our bank. Our people share a drive to contribute to a better society. We recognise the value our employees bring to the bank, and we work hard to attract and retain the best people. We also know that in addition to our people’s knowledge, their intuition is essential to our fulfilling our gatekeeper role.

Guidance for the gatekeepers

To support our staff in fulfilling this important responsibility, we have established the DFC Academy. The DFC Academy offers employees intensive training given by a combination of in-house experts and national and international experts. The broad and versatile programme focuses on how to protect the integrity of the financial system and how to ensure that ABN AMRO complies with its regulatory obligations. We continuously encourage our employees to develop themselves.

One way of working

In our harmonised Know Your Client (KYC) and Client Due Diligence (CDD) processes, clients (whether they are served by one or more business lines, branches or subsidiaries) are assigned a risk classification in line with their risk profile and are handled in accordance with risk-based priority. We continue to improve and redesign our CDD and KYC processes to ensure increasingly streamlined and faster processes and upgraded automation.

State-of-the-art systems and tools

We recognise that tools are essential for our employees to safeguard the integrity of the financial system, and we continuously acquire and develop the best possible tools for detecting financial crime.

Innovations

Criminals are becoming increasingly sophisticated and organised. As a result, financial crime patterns are constantly changing. While expectations remain high, our work as a gatekeeper of the financial system is becoming increasingly challenging. ABN AMRO has taken various steps to stay on top of this important task. We invest in our innovation unit, collaborate with external experts and companies, and continuously seek new partnerships in order to design and adopt smarter solutions. We also participate in a number of public and private partnerships, for example the Terrorism Financing Taskforce, the Serious Crime Taskforce and partnerships in the areas of human trafficking and corruption. To further combat money laundering, we will continue our work in public and private partnerships, such as Transaction Monitoring NL (), policy alignment, data taxonomy, taskforces and work groups (Dutch Banking Association (NVB), FEC Committee), to enhance a coordinated approach to anti-money laundering and terrorism financing. Networks and partnerships are needed to combat criminal networks.

Breakdown of Client Life Cycle process

Client life cycle

The client life cycle is the end‐to‐end management of a client during their entire relationship with ABN AMRO: client acceptance, periodic and event-driven reviews, monitoring for unusual or suspicious activity, reporting of suspicious activity and ultimately the exit of the client in the event of unacceptable compliance and integrity risks.

New client take-on

The client acceptance process for onboarding of a client with whom the bank is considering entering into a business relationship.

Client filtering

The process of filtering clients and relevant related parties as well as ABN AMRO partners.

Ongoing client monitoring

CDD means taking into account all those factors that the bank needs to determine when assessing whether a client is or is still acceptable to the bank. Due diligence procedures include KYC measures and risk assessment at acceptance, and reassessment throughout the client life cycle. CDD includes the following processes: New Client Take-On, Event-Driven Review, Periodic Review, Client Filtering, Transaction Filtering, Transaction Monitoring, Internal SAR filing and Exit.

Periodic review (PR)

Periodic reviews (PR) require the client owner to assess whether the current AML/CFT risk rating is still applicable and to determine whether the risk the client poses remains acceptable to ABN AMRO.

Event driven review (EDR)

An ‘event’ is any change in the circumstances relating to a client or client segment of ABN AMRO that potentially changes the client’s AML/CFT risk rating or represents increased AML/CFT risks for ABN AMRO. An Event-Driven Review (EDR) is a review of the client with a focus on the event that triggered the EDR.

Transaction monitoring

Monitoring of changes in the pattern of transactions to and from an account, or changes in circumstances, that are not consistent with the client’s normal and expected transactions and might prompt further analysis.

Transaction filtering

ABN AMRO does not facilitate transactions involving parties or goods subject to economic sanctions. Cross-border transactions must be filtered against the sanction lists before they can be executed. Transactions may need to be frozen or rejected in accordance with applicable sanctions restrictions.

Client exit

As part of Client Due Diligence, the risk assessment may result in an unacceptable AML/CFT risk. For a prospective client this will lead to rejection, for an existing client to an exit.