SustainaWeekly - ECB bond greening to intensify and spread

In this edition of the SustainaWeekly of the new year, we start by looking at key speech last week by ECB executive Board member Isabel Schnabel. The clear message is that the ECB will step up the greening of its bond portfolio both by intensifying its efforts with regards to its corporate bond holdings, as well as expanding its efforts to the other asset classes in its bond portfolio. Most notably, this will include public sector bonds. We set out the complications when it comes to a green public sector framework and the strategy the ECB is likely to employ. We then go on to look energy intensity trends across different sectors and subsequently healthcare real estate issuers in our ESG bond section.

Strategist: The ECB has signalled its intention to go further in greening its bond portfolio. It looks likely to actively reshuffle the stock of corporate bond holdings towards greener issuers. In addition, it plans to extend greening to other asset classes, most notably public sector bonds. The ECB looks set to increase the weight of SSAs (where the green proportion is higher) and increasing the share of sovereign green bonds.

Economist: Natural gas consumption decreased by 24% during 1990-2021, while the use of non-fossil energy carriers increased sharply. Growth in renewable energy stands out, with a 233% increase over the last 30 years. But despite this sharp growth, the total amount of energy in PJ is still limited. In almost all energy-intensive sectors, intensity has declined significantly since 1995, except in mineral extraction.

ESG Bonds: So far there are only three issuers have a clear focus on healthcare real estate and have accordingly issued social or sustainability bonds. The sector offers various structural tailwinds and the recent distress at tenant Orpea is manageable. But we do see lack of consistency in bond pricing.

ESG in figures: In a regular section of our weekly, we present a chart book on some of the key indicators for ESG financing and the energy transition.

ECB bond greening to intensify and spread

The ECB has signalled its intention to go further in greening its bond portfolio

Given that reinvestments will likely end, the ECB looks likely to actively reshuffle the stock of corporate bond holdings towards greener issuers

In addition, it plans to extend greening to other asset classes, most notably public sector bonds

However, there are complications when it comes to public sector holdings

The capital key, the absence of a monitoring framework regarding the Paris objectives alignment, and the relatively small size of the sovereign green market, are key obstacles

ECB board member Schnabel suggested (i) skewing the holdings to SSAs and (ii) increasing the share of sovereign green bonds, which would be a more long-term strategy given the limited supply of sovereign green bonds at the moment

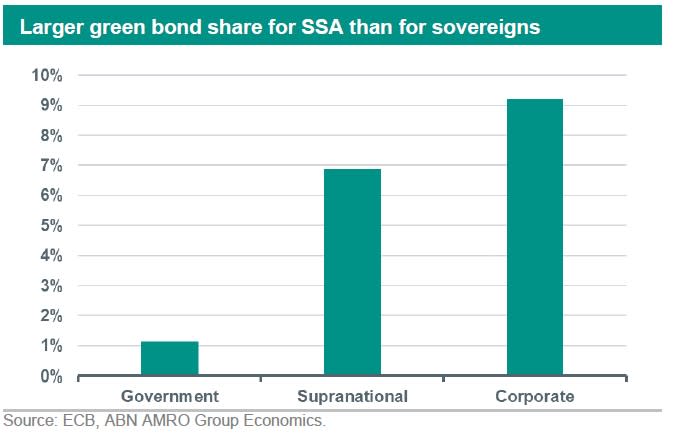

The European SSAs indeed offer a larger green bond market than sovereigns and additionally would not conflict with the Eurosystem capital key

Such a strategy could be supportive for the greenium from SSA and sovereigns, in which the latter has been declining for the past year

Last week, ECB executive Board member Isabel Schnabel held a speech about monetary policy and the green transition (see ). During the speech, Ms. Schnabel has highlighted that rising interest rates and high inflation jeopardize the green transition and that therefore the ECB would need to make additional efforts to align its actions with the objectives with the Paris Agreement.

ECB willing to sell bonds to green its portfolio

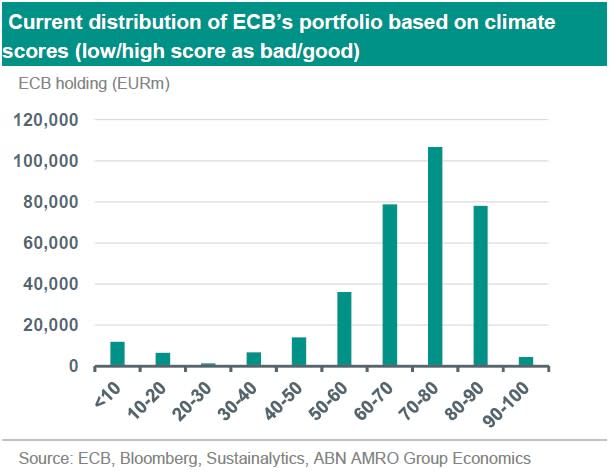

One of the most eye-catching messages was that the central bank will move from a flow-based approach to a stock-based approach to greening its stock of corporate bond holdings under the APP and PEPP. This makes sense as the reduction of reinvestments from March onwards, and the likely end of reinvestments in H2, will imply that the central bank no longer can decarbonise its corporate bond portfolio unless high-emitting companies themselves speed up their decarbonisation. In fact, it means that it will start actively ‘reshuffling the portfolio towards greener issuers’, which implies that it will need to actively sell bonds of companies with weaker green credentials and substitute these with bonds of greener companies.

Ms. Schnabel however made explicit that the intention is not to divest completely from high emitting companies (at least not initially), but rather foster incentives for them to reduce emissions further. We judge that this announcement will certainly have some spread impact, which will be negative for the issuers which are lagging behind in the transition. As we noted in our previous piece, currently a lot of issuers carry a very low “ECB score” due to the lack of proper ESG-related disclosures. Therefore, we judge that the first implication of such announcement is to incentivise companies to step up their efforts in terms of transparency on non-financial data disclosures.

“Greening” its holdings of other asset classes

In her speech, Isabel Schnabel strongly signalled the ECB’s desire to support the transition of the economy and to align its monetary policy decisions with the objectives of the Paris Agreement. To do so, the ECB is looking to also extend its portfolio greening to its covered bond, ABS and sovereigns portfolios.

With regards to greening its covered bond and ABS portfolios, Ms. Schnabel has highlighted that this would still require the development of a framework in order for the ECB to properly assess the ESG credentials of those exposures, which will likely follow the same three pillars chosen on the corporate side (quality of disclosures, backward looking and forward looking emissions). Nevertheless, it is likely just a matter of time before the ECB starts to decarbonise its covered bond and ABS portfolios. This is likely to support spreads of green covered bonds (and covered bonds by issuers with a strong green profile) over regular covered bonds.

With regards to public sector bonds, there are various complications that the central bank needs to overcome before such a green framework could come into place. The first of these highlighted in Schnabel’s speech is linked to the capital key. Indeed, the ECB must comply with the Eurosystem capital key when executing purchases in some of the ECB’s purchase programs. However, for this type of green framework, we doubt a capital key approach would be the best approach as the allocation would be unrelated to eurozone countries’ needs and progress made toward the energy transition. This connects to the second obstacle, which is the absence of a framework to assess the alignment of individual countries regarding the Paris agreement objectives. This adds to the difficulty for the ECB to adjust and skew its bond portfolio holdings away from public sector issuers lagging on the energy transition front. The third obstacle relates to the size of the sovereign green bond market. Indeed, despite a growing amount of issuance during the past years, sovereign green bonds remain a niche market. Out of the 19 Eurozone countries, 13 countries have issued green bonds so far, with most of them issuing their first bonds no longer than 2-3 years ago. Green bonds represent therefore only around 1% of the total sovereign bond market.

Currently, it remains unclear exactly how the ‘tilt’ of ECB holdings toward ‘’greener’’ countries with a more advanced energy transition will be executed in practice. The ECB has proposed two complementary options to make its public sector bond portfolio greener. One would be to reshuffle its portfolio in order to increase the allocation towards sovereign green bonds. Ms. Schnabel has highlighted that the central bank believes this would be a strategy in line with the Paris Agreement. However, we would like to highlight that this is not necessarily the case. For example, the Dutch State Treasure Agency (DSTA) has included climate change adaptations measures (such as expenditures related to flood risk management, flood defences, etc) in their Green Bond Framework (see ), which - while still particularly important - do not actually contribute to the decarbonization of the economy in line with the Paris Agreement.

Furthermore, given the relatively small size of the sovereign green bond market, Ms. Schnabel explicitly mentioned this would only be a course of action “as governments expand their supply of green bonds over time”. This implies that the sovereign green bond market would need to expand further before the ECB could intervene efficiently in this market. However, the prospect of the ECB adopting such a framework in the future could push governments to enter and/or increase their green supply in the coming future, as well as support investor demand.

ECB new framework to boost the Greenium …

As depicted in the charts below, the greenium (spread differential between green and non-green bonds of the same issuer and similar tenor) for core countries has so far been relatively moderate and continues to shrink. We discussed the greenium development in a previous note (see ) and it seems that the attractiveness of sovereign green bonds also diminishes during periods of stress. Indeed, as volatility in the rates market increased last year combined with poor liquidity, this led green and non-green peers to trade at similar yields. This is because sovereign green bonds tend to be less liquid than their non-green peers. Particularly in 2022, the Bund greenium reached all time low levels and has stabilised at these levels.

Hence, if the ECB indeed decides to tilt its public sector portfolio towards green bonds, this would be an important trigger for the greenium to bounce back. Given the relatively small size of the green bond market, the ECB would be able to acquire a significant portion of those bonds, likely to hold until its maturity and thus drive a significant difference in yields between green and non-green bonds. We have previously shown on the corporate side (see ) that the ECB net purchases tend to increase the spread difference between eligible and non-eligible CSPP bonds. Thus, we expect a comparable reaction if the ECB were to increase its focus on green bonds. Hence, we judge that a new climate-friendly monetary policy would help restore the greenium in the sovereign bond market. In addition, this would also help to reduce the cost of debt for governments committed to combat climate change and thus incentivize further national governments to make use of this market, which would be aligned with the ECB’s goals in greening the economy.

… as well as an additional push to green SSAs

The other complementary option given by Isabel Schnabel to tackle the complications set out above is to increase the share of bonds issued by supranational institutions and agencies (SSAs). This would imply skewing ECB purchases to SSAs. The argument was that a larger fraction of SSA outstanding bonds is green, roughly 7% according to the ECB estimates, as shown in the graph earlier in this note. This is indeed a higher share as well as amount than for sovereigns, where the green bond market represents solely EUR 210bn versus EUR 390bn for the European SSAs market (in terms of amounts outstanding). Moreover, increasing the ECB purchases to SSAs would not conflict with the requirement of the capital key and could be allocated more efficiently to the ones in need. An increasing number of SSA issuers are also becoming regular benchmark issuers in the ESG bond space and studies tend to show a higher greenium on average than sovereigns (something we will also discuss in a future note), which could serve as a greater greenium for investors if the ECB were to intervene as well.