Carbon Market Strategist - Prices drop following unprecedented tariffs

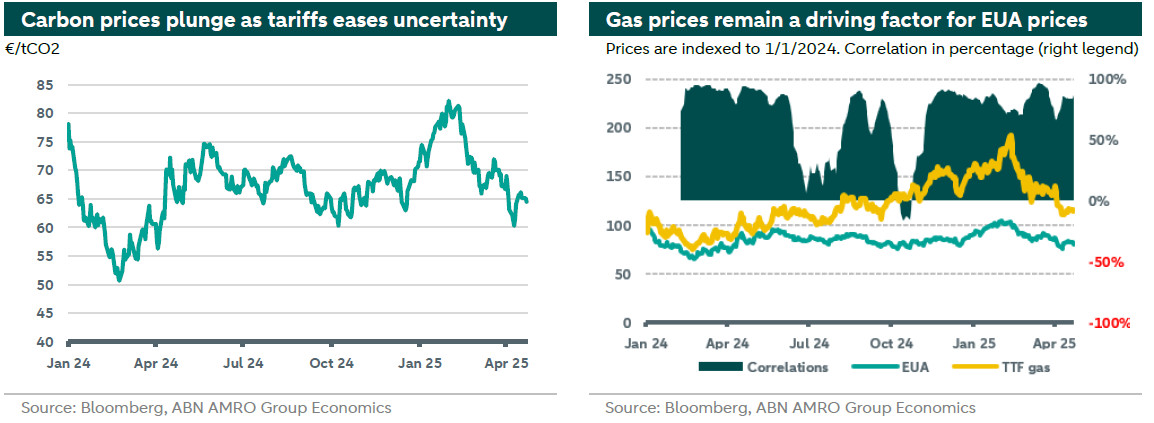

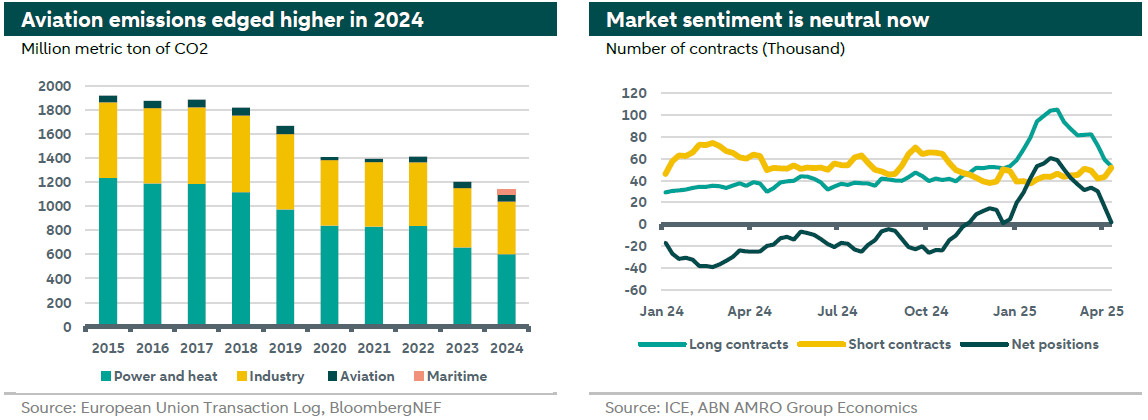

Carbon prices plunged to levels last seen twelve months ago after a temporary surge in late March. The decrease in prices was driven by a decline in gas prices following the announcement of the sweeping global US tariffs on 2nd of April, which was beyond expectations both in terms of their scope and levels. The tariffs have led to deterioration of the global economic outlook. Lower expected Asian demand, a main competitor for LNG, relieved the tightness in the market and drove European gas prices downwards. Carbon prices closely followed the movement of gas, as the correlation between the two markets remains at high levels. Accordingly, market positioning has moved back to more neutral levels, as traders unwound long positions. Meanwhile, new emission data shows a reduction of 2.3% in 2024 compared to 2023, where emissions witnessed a decrease in the power and industrial sectors, while that of aviation observed an increase. Furthermore, the carbon market remains responsive to weather conditions and geopolitical developments. EUA prices were trading around 66 EUR/tCO2 at the time of writing.

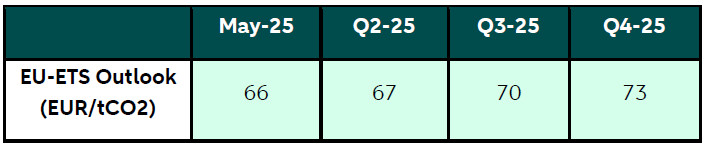

Carbon prices are expected to hover around 66 EUR/tCO2 in May, while reacting to weather conditions, and geopolitical risk

Gas prices continue to drive EUA prices, with a strong correlation between the two markets

US tariffs reduced growth expectations for Asia, easing competition for LNG cargos to Europe and lowering European gas prices

Geopolitical tensions and uncertainty around US tariffs saw a wind down of speculative long positions and the market is now neutral

2024 emission data for EU27 countries showed a 2.3% decrease, with power and industrial emissions down, but aviation emissions up

Carbon market developments

The correlation between carbon and gas prices remained strong for the sixth month in a row. After rallying early this year, gas prices have fallen significantly due to a number of factors: warmer weather as we exit the heating season, possibility of a flexible storage plan by the EC, advancements in peace talks between Ukraine and Russia, and the sweeping global tariffs imposed by the new US administration. More precisely, the US government announced reciprocal tariffs that exceeded all expectations, with minimal 10% blanket tariff on all countries and higher rates for specific nations. These tariffs deepened concerns on global growth outlook. Although Trump subsequently announced a 90-day postponement of these tariffs (except for China), uncertainty still dominates the markets. You can read more about the potential macro impacts of the tariffs in our most recent notes and .

At their announced levels, the US tariffs have induced lower growth expectations for Asia, reducing the competition for LNG cargos coming to Europe and decreasing European gas prices. Carbon prices followed closely the developments in the gas market as the correlation between the two markets remains high, as illustrated in the chart above (right).

The tariffs on European exports are expected to adversely affect European growth over the coming months. However, the 90 days pause is expected to induce a front-loading positive effect on growth in the second quarter of 2025. Additionally, the impacts of the tariffs will be mitigated by the EU fiscal stimulus targeting infrastructure and defence spending. Though such impact will take time to come through but once it does it helps drive a recovery during the course of 2026. Accordingly, the recovery in industrial output and emissions could witness a slowdown in the second half of 2025 before picking up in 2026. Meanwhile, in 2026 the Border Carbon Adjustment Mechanism (CBAM) is expected to get into force. CBAM would, in theory, level the playing field between domestic and foreign producers in the EU market. The implementation of CBAM would also mean that many industrials will lose their free allowances which could decrease profitability and induce pressure on producers with relatively high emission profiles.

With regard to maritime emissions, the wide scope and high levels of the tariffs are expected to hit trade flows and global shipping adversely. In consequence, we expect the tariffs to hit emissions for voyages involving European ports, inducing lower demand for EUA from that sector, especially in the second half of 2025.

Meanwhile, the newly published 2024 compliance emission data for EU27 countries showed a decrease of 2.3% compared to 2023, as illustrated in the chart below (left). Both power and industrial emissions witnessed a decrease in their emissions, while aviation emissions saw an increase. You can read more about recent emission trends across countries in our recent note .

Geopolitical tensions and high uncertainty associated to the final scope and level of the US tariffs, and their corresponding impacts, induced a shift in market sentiment in the EU carbon markets with traders winding down long positions, as can be seen in the chart above on the right. However, the market is now neutral in terms of net positions, suggesting that there is still scope for more bearish sentiment to take hold.

In that regard, as geopolitical risks mount, we could see some interventions within the EU carbon market, like those taken in the aftermath of the energy crisis, where a front-loading of allowances was used to finance REPower EU packages. That said, there are also some calls for the postponement of EU-ETS2 for one more year towards 2028. Some member countries also calls for the postponement of CBAM. Such change in timelines and climate regulations would translate into less incentives for reduce emissions and prolonged higher emission levels and lower carbon prices but all this is highly uncertain.

Outlook

As the current supply uncertainty remains in the gas market, the correlation with carbon prices will remain in play, and prices will be responsive to any rise in geopolitical risks, especially those related to the current trade war, or the levy of new sanctions that affect energy markets, cost structures, output, or emissions. At the same time, weather conditions will remain a source of volatility in the carbon market during the coming months through their impact on power generation. Accordingly, as things stands today, we expect carbon prices to hover around 66 EUR/tCO2 in May. We still expect a rebound around the surrender date (30th of September), but we think the impact will be mitigated by the expected slowdown in global economy which will negatively affect demand from the industrial and power generation sectors. Thus, our outlook for Q3 and Q4 is revised slightly downward towards 70 EUR/tCO2 (was 73) and 73 EUR/tCO2 (was 78). The table below summarizes our EUA price outlook for 2025.