One week later - Reversal Day

Reciprocal tariff pause limits downside risks, but growth shock still significant

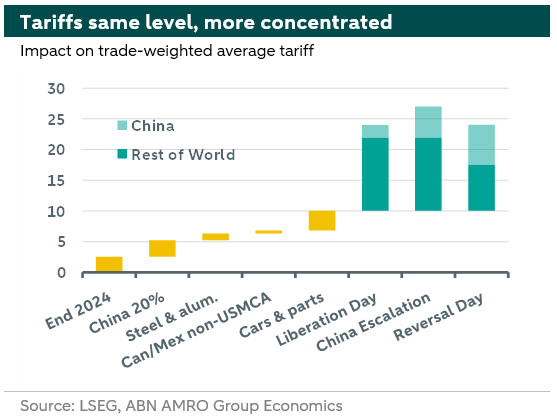

Yesterday Trump announced a 90-day pause on to every country but China, who was hit by an additional tariff hike to 125% (though the incremental escalation is smaller, adding 21% compared with 50% in the previous round). At the same time, the universal tariff of 10% stays in place, as do the separate 25% tariffs on steel & aluminum and cars & car parts. This is therefore not a full reversal of the Trump administration’s trade policy. The chart below highlights that, assuming end-of-2024 trade volumes, the change of course merely brings us back to the pre-China-escalation level in terms of trade weighted average tariff, but the trade restriction is far more concentrated towards China. We see two main takeaways; on the positive side, tail risk to the global economy is reduced. A Trump put exists: the scenario that things keep escalating and that Trump is insensitive to market pressures seems off the table. Still, taking a step back, the tariff package that remains in place is massive, there are still threats in the air, such as tariffs on pharmaceuticals (1/4 of EU exports to the US), and the full reciprocal package may still come into play 90 days from now. Meanwhile, there seems to be a high bar that other tariffs would be unwound, with Kevin Hassett (Chair of Trump’s National Economic Council) stating that countries would have to strike an ‘extraordinary’ deal for tariffs to go below 10%.

The Trump put was exercised before the Fed had to seriously think about stepping in

We’ve that, with various checks and balances actively being dismantled, financial markets may be the only backstop to stop Trump policy. While stock markets did not seem to rattle him and given his remarks that ‘THIS IS A GREAT TIME TO BUY!!!,’ he did not seem to mind the ‘dump-and-pump.’ The rapid rise of more than 60bps in the span of days in the 10y US Treasury yield, which alongside the weaker dollar fuelled a broader US confidence crisis narrative, may have been the ultimate catalyst triggering the Trump put. (This unusual combination of rising rates and a weakening currency was ultimately what famously brought down the Liz Truss government in the UK in 2022.)

For the US, the damage is done

The tariff’s impact on the US is two-fold. There are near-mechanical effects on inflation and growth, directly stemming from price increases due to the added tax. A (partial) reversal of the tariffs immediately lessens this direct blow. Even if the total trade-weighted tariff is back at the level implied by the original Liberation Day plan, the more concentrated nature of high tariffs on China and lower on everyone else, limits the impact as there’s more scope for rerouting and substitution. This will also endogenously lower the trade-weighted average tariff quite quickly as demand for Chinese goods declines. Still, the confidence and sentiment effects in the US, both domestic and external, from the administration's economic attacks and policy uncertainty remain. Even if tariffs are fully reversed, it seems unlikely that business will continue as it did in 2024, with the world likely moving away from their dependence on the US and the dollar. The near-term also remains murky, due to large policy uncertainty and volatility. The extent to which companies believe that higher tariffs will indeed start in July, will determine whether companies will continue to build inventories, and whether net imports will remain a drag on growth throughout Q2, or whether we will see the previously anticipated reversal. Overall, yesterday’s developments only strengthened our keeping rates at their current level until well into 2026. There will still be a substantial inflationary impact, and recession risks have abated somewhat. (Rogier Quaedvlieg)

What does the reprieve mean for the eurozone and the ECB?

For the eurozone, the pause is clearly a positive, though it is not a game changer. European exports will still see a significant hit from the 10% baseline tariff as well as the 25% tariff on cars, steel & aluminum. If Trump follows through with a similar magnitude tariff on pharma, then the trade weighted tariff on the exports to the US would rise to c15% from the c2-3% that prevailed until a month ago. Meanwhile, the euro is no longer the offsetting cushion that we thought it would be, as the euro has actually strengthened, partly due to general dollar weakness. All told, while the lower tariff rate would mean somewhat higher near-term quarterly growth, the big picture of a large growth shock this year remains broadly in tact. Given this, and given that inflation is likely to undershoot the 2% target later this year, we also think the ECB would continue to cut rates at the next four consecutive meetings, starting next week and taking the deposit rate down to 1.5% by September.

Would the EU team up with the US against China?

The US seems to be finding a new-found use for allies and is trying to shift the narrative to one of ganging up on China. Treasury Secretary Bessent’s comments leading up to the 90 day pause announcement clearly hinted at that, when he warned Europeans that it would be ‘cutting your own throat’ to work with China and that the US and its allies could ‘approach China as a group’. We think the EU would certainly pause for thought before following the US down a path of targeting China, given how unreliable the US itself has been as an ally of late. However, the reality is that Europe is far more dependent on its export relationship with the US than it is with China: the EU exported around $500bn to the US in 2024, more than double the c$200bn it exported to China. If the US were to try to coerce the EU into targeting China (for instance by threatening secondary tariffs), the EU would be put in a difficult position, and balancing US demands with its trade relationship with China would be challenging to say the least. (Bill Diviney)

China: Singled out again

In our 2025 Outlook, The Year of the Tariff, we already assumed China to be ‘singled out’ as main US bugbear, receiving a much higher tariff than for the rest of the world. While the current escalation of the US-China trade war leads to even much higher bilateral tariffs, the recent increases thereof are less meaningful than they appear. Chinese exports to the US would also fall sharply with 54% tariffs, an increase by another 75pp does not add much in that respect. That said, the external shock that China will face over the coming quarters is large. We expect direct exports to the US to collapse. Mitigating factors are the fact that some products for which there are product-specific tariffs face lower tariffs, and the remaining possibility of trade rerouting. Trade reorientation (from the US to other final destinations) also remains an option to cushion the blow (this also happened during the 2018-19 tariff war). In that sense, the postponement of reciprocal tariffs is in a way beneficial to China, because this means that the global demand shock will be softer.

However, China may face increasing tensions too with other trade partners, who are weary for a flooding of exports from China. Brussels is already preparing for this risk, with additional tariffs (beyond EVs) seen as a potential tool. At the other hand, for Brussels some kind of trade reorientation may also be welcome. As China would need to carefully manage trade relations with other trade partners including the EU, perhaps this is a good moment for Brussels to make clear agreements with Beijing. This is perhaps not even the endgame though. Comments from US officials seem to hint at the possibility to ask countries negotiating for lower tariffs to levy tariffs on China as well. If that’s the direction of travel, the export shock to China may become much bigger.

A clear litmus test for Beijing’s commitment to support domestic demand.

Meanwhile, domestically China has clearly changed tack following Liberation Day. Not only by mirroring additional US tariffs, but also in terms of macro and FX policy. In the first round of tariffs the yuan was still held relatively steady, but now more tolerance versus CNY deprecation is accepted – in line with our USDCNY forecasts (7.80 per end-2025). The easing of the foreign exchange valve also creates more room for monetary easing, we expect more policy rate and RRR cuts to follow soon. More broadly, Chinese policy makers are coming together to step up/frontload fiscal stimulus (in line with our expectations). Given the dramatic turn in exports from growth engine to key drag, this creates the ultimate litmus test for the government’s commitment to stabilising the property sector and bolster domestic demand. It is likely that they will try to directly support consumption demand, and if this does not work they may resort to more old-school support measures (e.g. infrastructure investment).

What does this mean for our China growth forecasts?

We already had below-trend growth in Q2 and Q3 given our bearish tariff view and this explains while we still are a bit below consensus (regarding GDP growth in 2025). Still, consensus is gradually moving our way. The quarterly growth profile will likely change following the latest developments (more downward pressure initially). We will review our China growth forecasts more closely after the publication of the Q1-25 GDP figures on April 16th and will publish revised forecasts in our April Global Monthly. (Arjen van Dijkhuizen)