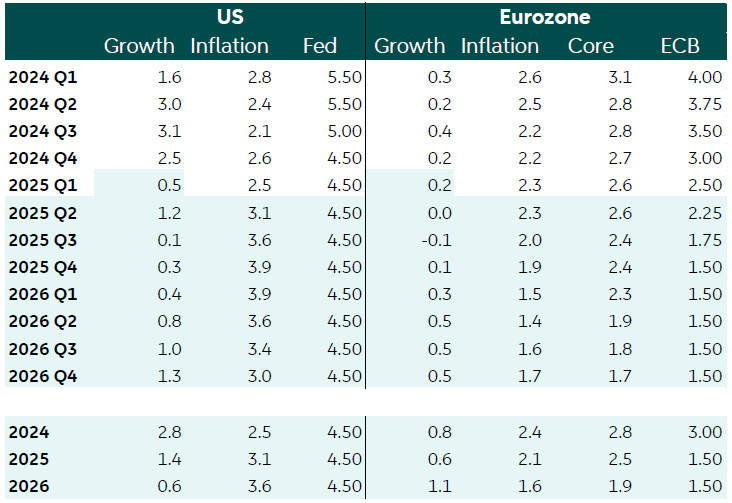

Tariffs risk recession - a forecast update

President Trump announced sweeping ‘reciprocal’ tariffs based on the size of the bilateral trade deficit. We expect both the US and the eurozone to slow sharply and only just skirt a recession, while the US will also have to deal with higher inflation. Monetary policy divergence is likely to re-emerge as a theme, with the ECB cutting rates further but the Fed remaining on hold. Fiscal stimulus should help drive a eurozone recovery in 2026, but growth improvement in the US next year will be more tepid.

An unprecedent shock is about to hit the global economy

The White House’s reciprocal tariff plan had been billed as a game changer, and the ‘Liberation Day’ announcement yesterday certainly lived up to that. In this note we set out our initial take alongside forecast changes that seek to capture the impact of the announcement. The unprecedented nature of the tariff shock makes it difficult to quantify the full effects, and so the forecast changes we make today could well be the first in a series of changes that will come as the situation evolves. In our new base case, the eurozone will see an earlier and bigger downward growth shock, and alongside the US is likely to skirt recession for the remainder of 2025. A recession is not our base case but the risk has risen significantly. For next year, we expect much higher fiscal spending in Europe (both defence generally and in Germany infrastructure) to lead to a rebound in growth.

Three key takeaways from yesterday…

Leading up to the announcement we had already expected very significant and across the board tariff rises, but there were three things that stood out: 1) The sheer scale and the breadth of the rises in tariffs was unexpected, with a 10% universal minimum tariff and individual countries often facing far higher tariffs. This raises the risk of a global growth shock that ends up being more than the sum of its parts. 2) Asia is much harder hit than Europe with tariffs in some key countries in excess of 40% – which acts to some extent as a cushioning factor for countries less hard hit. This is because their competitive position vis-à-vis trade with the US is enhanced, even if their position relative to domestic US producers is hit hard. 3) There are some very important exemptions to the tariffs – most notable for Europe is the (partial) exemption of pharmaceuticals, which made up a quarter of all EU imports to the US in 2024. Tariffs on these exempted products have however been threatened, and it is still unclear if the lower 10% baseline tariff may apply. Still, this could be a short term cushioning factor for Europe (and others that depend on pharma exports to the US), especially in the near-term as there is likely to be frontloading of exports ahead of feared tariffs.

…and three key uncertainties

Aside from the above factors there are further layers of uncertainty, and how this uncertainty resolves will be key for the outlook. First is the potential for retaliation and escalation. So far retaliation threats to yesterday’s announcement have been vague, with the EU for instance stating only that it would ‘respond’, though indications are that France and Germany are calling for aggressive moves to target US big tech/services. We assume one round of retaliation in our new forecasts but no renewed US escalation on the back of that. The latter could be a significant risk. The second uncertainty revolves around diversion and dumping. China is making overtures to other global trade players such as the EU to work more closely together. It remains to be seen how quickly companies losing access to the US market will be able to find new markets elsewhere, and a counter to this would be that fear of dumping will induce the opposite – that other countries erect their own trade barriers to protect industry from further pain. The third big uncertainty is the fiscal response. Already in Europe, we expect higher defence and German infrastructure spending to act as an important offset next year, but this would be too late to cushion growth in the very near term. Companies might make the case to governments that they are facing an unforeseen exogenous shock that necessitates government support until new markets for their goods are found, similar to the ‘bridging’ support seen during the pandemic and energy crises. We think this would only come into play if the alternative is major bankruptcies, but that if push comes to shove governments would probably step in.

The US is skirting a recession

Following earlier steps in our March Global Monthly, we are further downgrading our growth estimates for the US. Based on our earlier analyses, the complete package of tariffs enacted since the start of this administration (a roughly 20pp increase in the trade-weighted average tariff) puts a drag on US GDP of around 3pp over two years, with inflation rising 1.5-2pp. Our new base case for the US economy is largely consistent with this, weighing some of the possible scenarios in which this new shock may play out.

For the first two quarters of 2025, front-loading will distort the readings, with a surge in imports pushing down GDP in Q1 and a reversal pushing it back up in Q2. The second half of the year will more clearly reflect the negative impact of the sweeping tariffs on activity, both directly, and indirectly through high economic uncertainty and decreasing consumer and investor confidence. This results in a severe decline in consumption and investment growth, and both imports and exports weakening. We expect total 2025Q4 y/y growth to drop to a mere 0.5%. In 2026 we will see a slow recovery from a low baseline, but the structural changes set in course by these tariffs continue to be a drag on the US economy. The impact on the unemployment rate is limited due to a concurrent decrease in labour force growth, although pockets of unemployment in certain sectors or regions are likely. Meanwhile, higher inflation projections reflect the higher cost of imported goods and higher demands on domestic production. Headline PCE Inflation is likely to touch 4% at the end of this year or early next year. Compared to this new base case, growth risks are probably still tilted to the downside, with inflation risks more balanced on the back of uncertainty in exchange rate adjustments and pass-through to final prices. A reversal of tariff policy will do more to undo the inflation shock than the growth shock.

This leaves the US in a scenario of low growth and elevated inflation, putting the Fed in a difficult position. Survey evidence suggests a risk of inflation de-anchoring while our base case does not yet see a recession materializing, limiting the likelihood of a rapid easing cycle to support the economy. Ultimate retaliation policy may provide a clearer signal on the question of whether the inflation shock will be transitory or more substantial, leading to upside risks to the path, while at the same time, the risk of an even stronger downturn puts downside risk to the Fed path. We continue to think that the Fed's likely response in the face of this uncertainty is to keep rates where they are for an extended period. (Rogier Quaedvlieg)

China faces larger export shocks, Beijing will step up support and looks for allies

China will now be faced with an average import tariff rate of (at least) 54%. Although this is not far from our assumption of 45%, this comes quicker than the gradual build-up we had assumed. Moreover, typical trade diversion routes (through countries like Vietnam and Mexico) will dry up given that these countries are facing high tariffs as well. All of this means an even larger shock to China's exports to the US, but likely also a bigger shock to total exports (due to the impact of the new tariffs on global growth/trade including trade partners in Asia). Mitigants would come from negotiations (although initially, retaliation/further escalation is also a possibility), more fiscal and monetary support (which we assume) and trade reorientation - with a remarkable rapprochement seen between China, Japan and South-Korea. Taking these factors into account, China's resilience shown in Q1, and the fact that we are already a bit below consensus due to our tariff assumptions, we leave our China growth forecasts unchanged for now. We will review them later in April, after publication of the Q1-25 GDP figures, and publish revised forecasts in our April Global Monthly (see for more our China update, , published earlier today). (Arjen van Dijkhuizen)

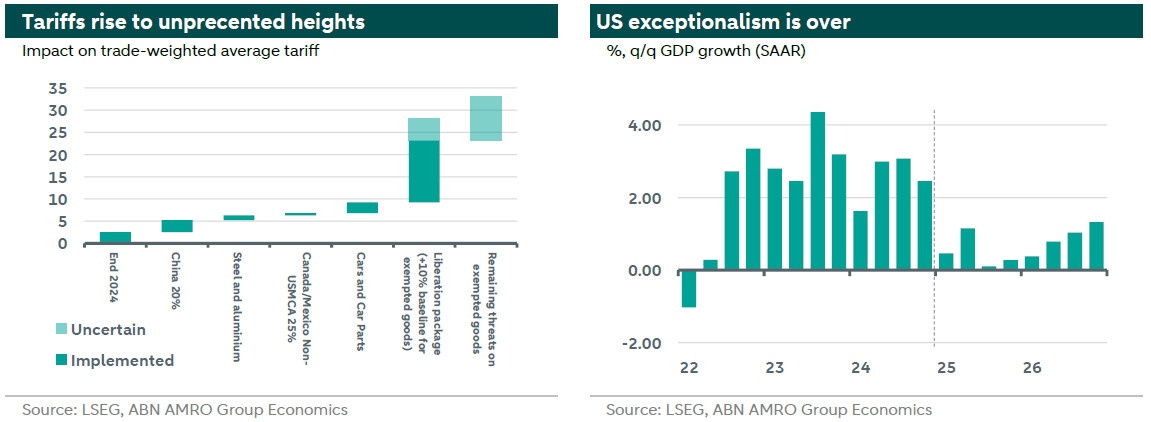

Eurozone: Big near-term growth hit; defence and German bazooka to drive 2026 rebound

The EU has been hit with a 20% tariff – with a 25% tariff on cars/car parts (around 9% of exports to the US), and an exemption for pharmaceuticals (around 25% of exports to the US). We expect this to drive a sharp fall in exports to the US over the coming months, and we are significantly downgrading our 2025 growth forecast on the back of this. In the near term, we expect quarterly growth to hover around zero, with a high chance of a negative quarter, though frontloading effects may muddy the impact. The tariff increase facing the EU is relatively lower compared to other regions, except for the UK, which could serve as a mitigating factor. For 2026, we are modestly upgrading our forecast to reflect a) an earlier fading of tariff impact given the earlier start of tariffs than we previously had in our base case, and b) much more fiscal spending – especially from Germany. For 2025, we have halved our growth forecast to 0.6% from 1.2% previously, while for 2026 we raised our forecast by 0.3pp to 1.1%.

The trough in quarterly growth is expected in Q3, with a recovery expected to start towards the end of Q4 and picking up steam in 2026. The recovery is driven partly by a) fading tariff impact, and b) some combination of mitigating factors. These include: 1) the potential for a partial US climbdown from tariffs (driven by negotiations or perhaps domestic pressures), 2) finding new markets for goods/possible diversion of trade, 3) balance sheet support from governments if things get really bad.

Beyond this and looking to 2026, we expect higher eurozone defence spending and Germany’s fiscal bazooka to pick up the baton and drive a more meaningful recovery. In the eurozone we expect defence spending to rise from the current 1.9% of GDP to c2.5% by the end of 2026, and in Germany, we expect a combination of higher defence spending and infrastructure spending to start meaningfully supporting growth.

With regards to inflation, we are slightly upgrading our forecast reflecting that the EU is likely to retaliate against US tariffs in a more meaningful way than we previously expected (though this is still highly uncertain); effects of higher fiscal spending are likely to come later, in 2027. However, we continue to see the potential upward pressure from tariffs as quite limited. As described in our Global Outlook, the US share of eurozone goods imports stands at just 13%; around 20-30% of goods consumption is imported; and goods makes up 26% of the HICP basket. Based on this, a 20% rise in the price of US goods imports would add only 0.2pp to HICP inflation.

The impact of the EU potentially deploying its services/Big Tech targeted ‘anti-coercion instrument’ (ACI) also looks unclear. While there is the potential for instance to put levies on streaming services, many of the measures targeting services would not be inflationary – for instance, higher digital services taxes on company revenues, or the suspension of intellectual property rights. There are also downside risks from weaker eurozone activity and possible dumping of goods onto the European market by Asian exporters. All told, our big picture view remains that inflation is more likely to undershoot the ECB’s 2% target, largely on the expected hit to energy prices due to the global growth shock. Taken together, and including retaliation effects, we have raised our 2025 inflation forecast by 0.1pp in both 2025 and 2026, to 2.1% and 1.6% respectively. (Bill Diviney, Jan-Paul van de Kerke).

The Netherlands: Hungover from ‘Liberation Day’

While there is a lot of uncertainty about the impact of the tariffs, there are several channels through which they impact the Dutch economy. Firstly, there is a direct effect on Dutch exports to the US. Our calculations show that the tariffs, including exceptions for products like pharmaceuticals, will cause exports to the US to decrease by 1.6%. About 6% of total Dutch goods exports go to the US, accounting for approximately 4.8% of Dutch GDP. This direct effect will impact the Dutch economy in the short term. Then, there is the indirect effect, which probably dominates; a weakening of the global economy particularly affects the export-dependent Dutch economy.

There are a few mitigating factors. As mentioned in the above, the relative competitiveness position of the EU versus countries with a higher tariff and in the short-term some frontloading of goods that temporarily enjoy an exemption, such as pharmaceuticals. This can somewhat soften the impact on Dutch growth.

Additionally, Trump’s announcement isn’t the only recently announced game-changer for Dutch growth forecasts. Fiscal largess in the country’s main trading partner Germany has spillovers to the Netherlands, which comes on top of the EU ambition to increase defence spending. In terms of the growth profile, timing plays a significant role here. Import tariffs mainly impact the economy in H2 2025, while the growth impulse from fiscal spending will ramp up over the course of 2026.

Due to the above factors, we have revised our growth forecasts for the Dutch economy. Our forecast for 2025 has been adjusted downwards to 1.4% (from 1.8%) because the tariffs are being implemented earlier and more extensively than we originally included in our projections. The forecast for 2026 has been adjusted upward to 1.3% (from 1.0%) primarily reflecting fiscal support and mitigating factors kicking in. (Jan-Paul van de Kerke, Aggie van Huisseling)

How will the ECB react to the trade war?

For the eurozone, higher tariffs in themselves would most likely call for lower rather than higher interest rates, but we also need to take into account the impact of fiscal stimulus, which points in the other direction. While in the US, tariffs will lower growth but raise inflation, we expect that for the eurozone both growth and inflation will be clearly lower. In contrast, the Governing Council is currently quite uncertain about the impact on inflation and therefore looks set to tread carefully allowing the evidence to drive decision making. As ECB Vice President Luis de Guindos noted earlier today there could be upward and downward effects on inflation and ‘the environment of exceptional uncertainty requires us to stick even more closely to our data-dependent and meeting-by-meeting approach’. We think ultimately, as the data comes in, it will make the ECB’s near term path very clear.

As shown in the charts below, for the coming quarters, our updated forecasts for growth and inflation will in both cases come in below the ECB’s staff macro projections, published last month. These downside surprises should trigger further reductions in the ECB’s key policy rates, beyond what markets are currently pricing in. Our baseline sees a further 100bp of rate cuts by the autumn of this year, taking the deposit rate to 1.5%. However, as we move towards the end of the year, economic growth starts to improve. In addition, there will be the prospect of a growth recovery in 2026 (and the years beyond) driven by fiscal stimulus. Given that fiscal policy will do a bit more of the heavy lifting, we think that terminal rate may end up higher than we previously forecast (at 1.5% compared to 1% before). (Nick Kounis)

Upgrade EUR/USD

We upgraded our EUR/USD forecast sharply to 1.08 from 0.98 for the end of 2025, and to 1.15 from 1.05 for the end of 2026. We are now considerably less negative on EUR/USD than before, but we still expect a modest decline from current levels. For a start, we expect substantial weakness in the eurozone economy in 2025 and the ECB to ease more than financial markets currently price in. This points to a lower EUR/USD. Furthermore, if risk off turns into panic the US dollar will be bought as global safe haven currency for liquidity reasons. There are a number of reasons why we are less negative on EUR/USD than before. Our out of consensus view of no Fed rate cuts in our forecast horizon with an economy that is weakening leads to a weaker dollar. US policy uncertainty will continue to weigh on the dollar. In addition, a stronger eurozone recovery puts upward pressure on the EUR/USD in 2026. Finally, the technical picture for EUR/USD looks positive and net-speculative positions in the futures market are not extreme net-long euro. The market was relatively neutral dollar at end of March (Georgette Boele).

Tariffs and Fiscal Policy: Key Catalysts for the future of European Rates

Market dynamics are shifting with renewed focus on U.S. tariffs, leading to a decline in European rates, which was in line with our expectations. Over the past weeks, attention was heavily skewed towards fiscal spending, while the potential ramifications of U.S. tariffs on the European economy were largely overlooked.

We see German government bonds rallying further in the coming months, with yields dropping, as the impact of tariffs on eurozone growth materializes and the ECB cuts its policy rates by more than markets expect. The prevailing flight to quality momentum to government bonds could strengthen, particularly in an environment of sustained volatility.

Looking ahead towards the end of the year – however - we anticipate a pivot back to fiscal spending narratives. As discussions around the 2026 budget advance and Germany unveils more definitive plans regarding defence and fiscal initiatives, we predict a renewed emphasis on increasing fiscal spending across Europe, ultimately leading to higher term premia. Additionally, we project a significant uptick in capital market issuance from Germany, estimated between EUR 65-80 billion in 2026. This influx is likely to exert upward pressure on long-term rates. Consequently, we are adjusting our 10-year Bund yield forecast slightly above the 2% level by the end of 2025.

On the US side, we expect quite a different development, particularly in terms of the yield curve shape. We anticipate the US Treasury curve to invert due to a significant repricing of Fed rate cuts, which will drive US rates higher across the curve. However, we expect the US economy to slow down in the second half of the year, exerting downward pressure on long-term rates. In contrast, short-term rates will remain elevated as we foresee the Fed funds rate staying at 4.5% until the end of 2026. Considering inflation expectations alongside lower economic growth projections, we expect the 10-year US Treasury yield to hover around the 4% level by the end of 2025.

We will publish a more detailed note next week on our new rates projections (incuding swap and country spreads). (Sonia Renoult)