The rise of a new sovereign ESG framework

The ASCOR project provides various metrics that assess climate change risks and opportunities at a sovereign level. The tool aims to provide a comprehensive and freely available framework that investors and issuers can use as a common standard. This framework can be a compliment to other frameworks, such as ESG country scoring and the use of proceeds tool of the Climate Bond initiative.

Sovereigns are making their way to greener investments and expanding their ESG financing

ESG data started to develop and extend to various metrics but is not always timely or accurate, and may involve bias, particularly in the sovereign space

Using an internationally agreed framework could help both investors and issuers on this topic

The ASCOR project is a first step in that direction and aims to fill this gap by providing various metrics that assess climate change risks and opportunities at a sovereign level

This tool aims to provide a comprehensive and freely available framework that investors and issuers can use as a common standard instead of relying on multiple different climate databases

In a previous publication (see ) we shed some light on the gaps and drawbacks of current sovereign ESG scores. The most important drawbacks we found were the lack of transparency, data accessibility and availability on the environmental front, income bias, and a backward-looking approach. ESG frameworks have started to emerge already on a corporate level with the most widely used one being the Climate Action 100+ Benchmark (see ), but are still lagging on the sovereign space. The ASCOR project aims to adopt a similar approach on a sovereign level. The ASCOR, which stands for ’Assessing Sovereign Climate-Related Opportunities and Risks’, is a project led by asset owners, asset managers, and investor networks to fill this gap and develop a publicly available, independent tool to assess countries on climate change. Indeed, even if ESG country scoring frameworks discussed in our previous note served as a first step to help investors in their investment decisions, this type of framework remains incomplete, and used alone could also lead to missed opportunities or worse, incurring higher (climate) risks than initially assessed in sovereign bond investments. As such, we judge that a proper sovereign ESG framework should consider additional indicators such as the country’s future trajectory, engagement, and financing capabilities to attain its climate goals which is what the ASCOR project attempts to do. In this piece, we will discuss this new sovereign ESG framework, the issues it addresses and solutions offered, and how it could be used as a (complementary) tool for current and prospective ESG investors.

First step toward an internationally recognized sovereign climate-risk framework

ASCOR published on the 7th of February a consultation report (see ) to introduce the project and outline the upcoming framework to assess sovereign bond issuers on climate change with the aim of gathering initial feedback. The goal of this project is to set up an internationally agreed framework to assess the climate-related risks and investment opportunities on a sovereign debt level. Indeed, as highlighted in our previous publications, the lack of data transparency and availability as well as a consistent framework to rely on, made the task particularly difficult for investors, institutions, and sovereign issuers themselves to properly invest and act on the green side of sovereign debt instruments. The end goal of this project would be to set an internationally recognized sovereign standard instead of using multiple different sources to assess sovereign ESG performance.

As such, a global coalition of asset owners and managers supported by international investor networks worked together in 2021(*) to create the ASCOR project to remedy some of those issues. The aim is for a country to be assessed against a framework that will analyse emission pathways, climate policy action, and opportunities to finance the transition. Furthermore, this framework will also be made freely available in an open-source online tool, which will already help on the transparency and data accessibility front. Important to note that this new tool is not meant to serve as a sovereign ESG scoring framework but rather a complementary tool to support investors’ decision-making process towards greener investments. ASCOR will launch this free online tool by the end of the year as well as publish the assessment of 25 countries (including some European countries like France, Germany, and Italy).

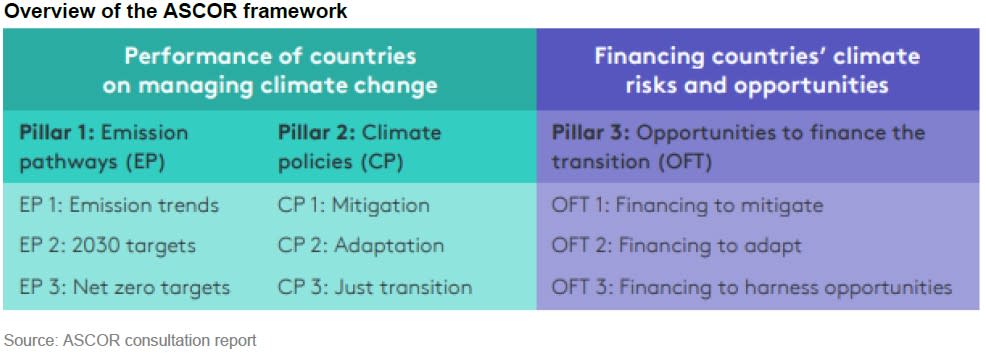

The framework is composed of three pillars, which we briefly discuss below and assess whether those indicators tackle our previously discussed drawbacks from current sovereign ESG frameworks.

Each pillar is divided into sub-themes, for each of which a set of indicators are defined. To keep it simple, ASCOR set out Yes/No questions for most indicators (see report for further details on the methodology).

Pillar 1: Emissions pathways (EP)

This pillar considers historical emissions trends and the alignment of forward-looking national emission reduction targets with international climate goals. In this pillar, historical emissions developments are analysed on five-year trends in absolute emissions and assess the annual rate of this trend against the emission reduction rate needed for the country to meet its 2030 target. The framework will assess whether the ambitions set by the country are sufficient to align with the 2030 emission reduction target from the Paris agreement as well as the global net zero target for 2050. In our view, this would serve as a critical metric for ESG investors as many countries issuing ESG bonds have not even adopted net-zero targets and/or decarbonization plans at the national level. A lot of the criticisms from the greenwashing detractors for instance were the lack of high ambitions on the climate front from most sovereign issuers. Thus, this pillar could help reconcile both issuers and investors by providing a clearer picture of a country’s climate ambitions and its capabilities and efforts put in place to meet them. However, as we will discuss in the third pillar below, we are still missing the analysis regarding the sovereign’s ESG bond’s use of proceeds and how this aligns with the country’s net-zero targets.

Two of our ESG measuring issues are addressed in this first pillar. One refers to the integration of a more forward-looking approach in assessing a country’s climate performance. Indeed, we observed that in many ESG rating methodologies, a more backward-looking approach was taken, which gave limited information about the country’s progress toward reaching its net-zero targets. In this pillar, the 20230 targets and net zero targets themes are both meant to provide a degree of alignment with the national 1.5°C target and whether the climate targets and policies put in place are sufficient to meet those. One of the metrics used will be the scenarios model from Climate Analytics, which will serve as a benchmark to evaluate whether a country’s Nationally Determined Contributions (NDC) are sufficiently ambitious to meet the 2030 targets. A second issue tackled in this pillar is income bias. We identified a significantly high correlation between a country’s credit rating and a country’s ESG score. In our view, this could lead to biased investment decisions skewed towards richer countries while saying little about the actual country’s environmental performance and effort made to reduce its carbon emissions.

Looking at the new EPI index report for 2022, we see that a focus skewed to a country’s environmental performance gives a different picture in terms of ranking than a country’s S&P rating or even its overall ESG score. Particularly when looking at some of the most developed and wealthy economies (such as the US, Germany, and Canada) which appear among the laggards in terms of environmental performance against less wealthy economies like Malta, Slovenia, or Cyprus. As such, we judge that a comprehensive and reliable ESG framework should give a fairer picture and account for countries’ differences in terms of climate mitigation requirements and longstanding progress on the environmental front.

However, one critical aspect this framework does not cover is the transboundary pollution spill over effect. Indeed, countries may perform well in environmental metrics by outsourcing their polluting activities and discounting trades in goods and services which is an issue that no sovereign data or frameworks have been able to cover yet. This issue has also been highlighted in the ASCOR consultation report. The project ambitions to develop such a consumption-based emission in their framework as soon as is practicable. Although, an indicator on the disclosure of consumption-based emissions is included in the second pillar under climate policies below.

Pillar 2: Climate policies (CP)

This pillar considers national policymaking efforts to mitigate emissions, adapt to climate change, and ensure a ‘just transition’. The main goal of this pillar is to provide greater transparency in the sovereign’s disclosure of emission data and related documents as well as demonstrate whether the country’s climate targets are credible and measurable. The last theme expands the analysis of the framework to account for physical climate risks as well as social issues relating to the low-carbon transition.

One innovative approach in this pillar is the consideration of physical risks which is usually a missing climate-related risk as most research and ESG data providers have been focusing on the transition risk. In the adaptation policy theme, ASCOR aims to measure the preparedness of countries to deal with the physical impacts of climate change like heat waves and hurricanes. The pillar also considers disaster risk reduction policies (such as multi-hazard early warning systems) which indicate how well a country can reduce the economic and social impact of acute climate hazards. Indeed, countries adopting early warning coverage can reduce significantly its disaster mortality rate. Those indicators are particularly important for ESG sovereign bond investors usually adopting a longer time horizon in their investments and thus, seeking to reduce climate-related risks exposures.

Despite a lot of research on transition risk, we are still lacking an international framework to assess and compare countries on this topic. Indeed, the economic and tax policies adopted on a government level play an important role in the green transition and should be considered when performing a country risk analysis regarding climate change. Countries adopting strong economic and financial incentives, such as the inflation reduction act (IRA) in the US, can be critical in a country’s advances toward reaching its net-zero targets. Although this aspect will not be part of this framework yet, this has been discussed as a potential area for ASCOR to develop in the future.

One interesting metric in this pillar is the inclusion of carbon pricing as more and more countries are putting carbon pricing at the centre of their mitigation strategies. The ASCOR will consider both national and supra-national carbon pricing systems such as the European Union’s Emission trading systems (ETS). Finally, another innovative feature we would like to pinpoint in this pillar is its just transition policy theme which addresses the social aspect of the climate transition. To do so, the ASCOR project aims to account for the social costs and distributional impacts of a country’s low-carbon transition while exploiting its welfare and employment opportunities.

Pillar 3: Opportunities to finance the transition (OFT)

This pillar considers the financing requirements needed for countries to achieve their climate goals. These indicators can be helpful for investors in recognizing countries with financial constraints and thus, that might slow down their climate-related achievements. In our view, this would best serve investors looking to invest in developing countries and emerging markets as those countries are the ones facing the greatest climate-related risks while facing limited access to financing. In this pillar, ASCOR will provide a clearer picture of a country’s funding requirements to meet its climate targets, whether its financing capabilities are sufficient to meet those, and account for financing transition opportunities that can be added to the country’s financing resources as well.

In addition, these indicators will highlight to investors potential investment opportunities and open further dialogue priorities between them and the issuers. However, one metric we are missing here is an indicator that analyses the use of proceeds from issued Green bonds by sovereigns to assess whether investments are aligned with the country’s set climate targets. So far, only the Climate Bond initiative has developed such a tool and thus this could be used as a complementary framework.

The ASCOR project will provide a helpful complement for sovereign ESG investors

The methodology and data that will be made available by this project will provide a simple, accessible, and complementary tool for current and prospective ESG investors. This framework is not meant to serve as an ESG country scoring but for individual investors to decide how to use this broader information data availability in their decision-making process and combine it with other frameworks such as ESG scoring providers. This project could indeed provide a first stepping stone to set a comprehensive standard to be used in the sovereign ESG field and provide further clarity on sovereign exposure to climate risks and climate policies that is useful for investment decisions.

In addition, this type of framework could serve as a base for the ECB in its aims to green its sovereign portfolio in the future (for more details on this topic see ). Finally, this new tool could be used by sovereign issuers in issuing sustainability-linked bonds (SLBs) by using it as a key performance tracker. Indeed, one way for governments looking to show display ambitions in their ESG transition plans could be through the issuance of SLBs as those bonds are tied to meeting key performance indicators..

(*) Members of the ASCOR Steering Committee are: the UN-convened Net-Zero Asset Owner Alliance, (AOA); Ceres; the Institutional Investors Group on Climate Change, (IIGCC); the Principles for Responsible Investment, (PRI) and SURA Asset Management.