Global Monthly - Cracks emerge amid tectonic shifts

The fracturing of the transatlantic alliance is going to mean higher defence spending in Europe over time, though the immediate macro-economic implications of this are likely to be modest. The most imminent threat still comes from higher US trade tariffs, with a host of measures due as soon as next week. Last month, Trump blinked at the last moment on the biggest tariff rises, will souring confidence in the US make him do so again? Spotlights: 1) European defence spending: We summarise the available options for an increase and the macro implications; 2) German election: We look at the likely policy agenda of the new GroKo.

Jaap Teerhuis

Senior Fixed Income Strategist

Co-author: Sonia Renoult

Global View: Brewing shocks are starting to have an impact. Is Trump going to blink?

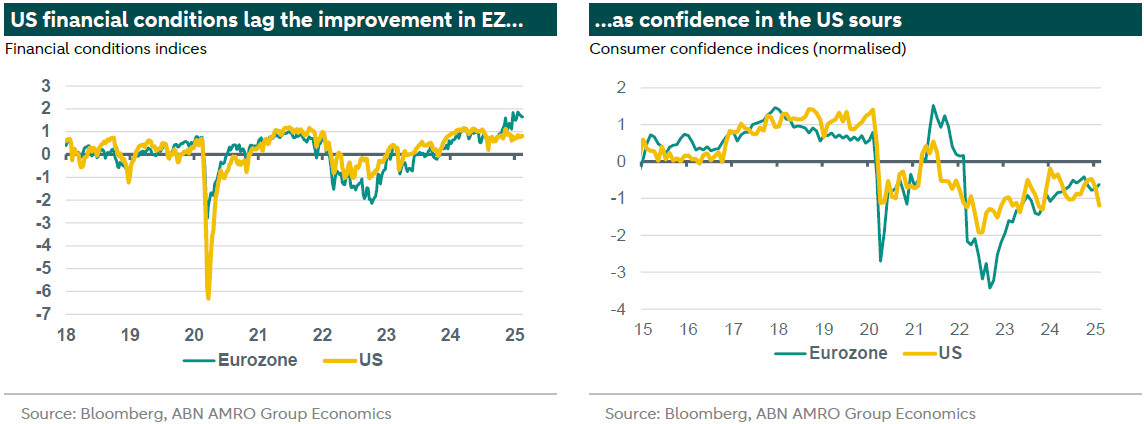

It has been a month of geopolitical earthquakes, and economic tremors. The most shocking development – the fracturing of the post-WW2 western alliance – does not yet pose immediate implications for the macro outlook. European defence spending is surely set to increase over the coming years, but the timing, magnitude, and composition of that increase remains highly uncertain. A significant moving part in all of this will be coalition negotiations following Merz’s expected victory in the German elections. We look at some of the broad implications of both of these themes in our two Spotlights this month, and we will have much more to say over the coming months as the details begin to crystalise. For now, the most imminent threat to the global economy remains US trade tariffs, with massive new Mexico and Canada tariffs perhaps coming as soon as next week. In recent days, we have published an overview of the main threats and what they specifically mean for the eurozone. In the meantime, while the hard macro data suggests the US economy continues to coast along for now, yesterday’s market reaction to a downside surprise in consumer confidence – which followed a spate of weaker survey data – suggests cracks in the market’s belief in US economic resilience. It wasn’t long ago that the talk was of Europe being left behind by a gold rush of investment to the US amid the new administration’s deregulation drive, and yet since then, European equity markets have outperformed those in the US – visible in the divergence in financial conditions indices – while consumer and business sentiment in the US has also softened, contrasting with the stability in Europe. The latest consumer confidence report cited renewed worries over inflation in the US, amid recent upside surprises and ongoing tariff threats. If the usual political checks and balances in the US don’t stop Trump, might souring economic and market sentiment? Watch this space.

Spotlight: European defence spending

Sonia Renoult, Senior Rates Strategist, Jaap Teerhuis, Senior Rates Strategist, Bill Diviney, Senior Economist Eurozone

Recent comments by Trump have suggested a diminished US commitment to NATO, prompting European nations to consider significant increases to defence spending

Various financing options were discussed at the Paris defence summit, including the exclusion of defence expenditures from EU fiscal rules, utilizing existing EU funds and facilities, and creating a new EU defence fund financed through joint debt issuance (similar to the NGEU programme post-COVID)

All else equal, higher defence spending could put upward pressure on growth and inflation, but the case for a prolonged ECB rate cut cycle remains very much intact

This Spotlight summarises our note EU defence spending could shake EGB market

European nations are under mounting pressure to increase their defence spending due to the shifting geopolitical landscape, highlighted by the United States' reduced emphasis on NATO commitments under President Trump. This situation poses significant implications for the European Government Bond (EGB) market as countries strive to meet higher defence spending targets.

Among the eurozone's largest countries, only Germany and France are projected to meet NATO's 2% GDP defence spending target by 2024, with the Netherlands nearly reaching it. However, countries such as Italy, Spain, and Belgium still fall short and may be required to substantially increase their defence investments. In a scenario where the NATO target increases to 3%, the EU's largest six economies would need to augment their spending by an estimated EUR 156 billion.

At the recent Paris summits, various financing options were discussed to manage these expenditures:

Excluding defence Expenditures from the EU fiscal rules: One direct approach is financing at the national level by excluding military spending from the EU's stringent budget deficit limits. This would allow member states to finance defence spending through higher deficits without breaching fiscal rules. However, this could lead to increased bond issuance and higher borrowing costs, heightening fiscal concerns among investors and exerting upward pressure on bond yields, especially for heavily indebted countries like Italy, Spain, and Belgium.

Utilising existing EU programmes: Some European politicians proposed using existing EU programmes to finance the increase in defence spending. Redirecting parts of cohesion or structural funds, such as the NGEU programme, towards defence-related investments could provide a temporary solution. However, this would require unanimous approval from EU member states and potential legal reforms. While this could alleviate immediate financial pressure on fiscally vulnerable states, larger economies like Germany and France would likely bear a bigger portion of the financial burden, potentially resulting in an underperformance of their bonds.

Creating a new EU programme/facility financed by joint debt issuance: Another option is establishing an EU defence fund programme through joint debt issuance, similar to the post-COVID NGEU instrument. While this could offer long-term funding stability and bolster domestic defence industries, achieving EU consensus for such a programme would be challenging and time-consuming. This approach might primarily benefit peripheral economies that currently fall short of NATO targets, potentially leading to the outperformance of their bonds.

Macro-economic impact and implications for the ECB

It is too early to draw concrete conclusions given how fluid the situation is, but all else equal, higher defence spending on the scale described above would put upward pressure on growth, inflation, and – depending on the timing – could lead to the ECB pausing rate cuts sooner than our current base case. We note however some caveats. First, any increase in spending is unlikely to fully offset the slowdown from the US tariff threat, which if anything is tilting towards a more negative scenario than our base case. Second, to the extent that other EU funds are redirected towards defence spending, this would not lift growth beyond our base case, as it would mean less spending in other domains. And third, it would take time for the EU defence industry to ramp up and to respond to higher spending, meaning that initially a significant portion of higher spending is likely to ‘leak’, i.e. be spent on higher imports (mostly from the US). This will dampen the growth and inflation impact.

Spotlight: CDU’s Friedrich Merz poised to be the next German chancellor

Bill Diviney, Senior Economist, Jan-Paul van de Kerke, Senior Economist, Philip Bokeloh, Senior Economist

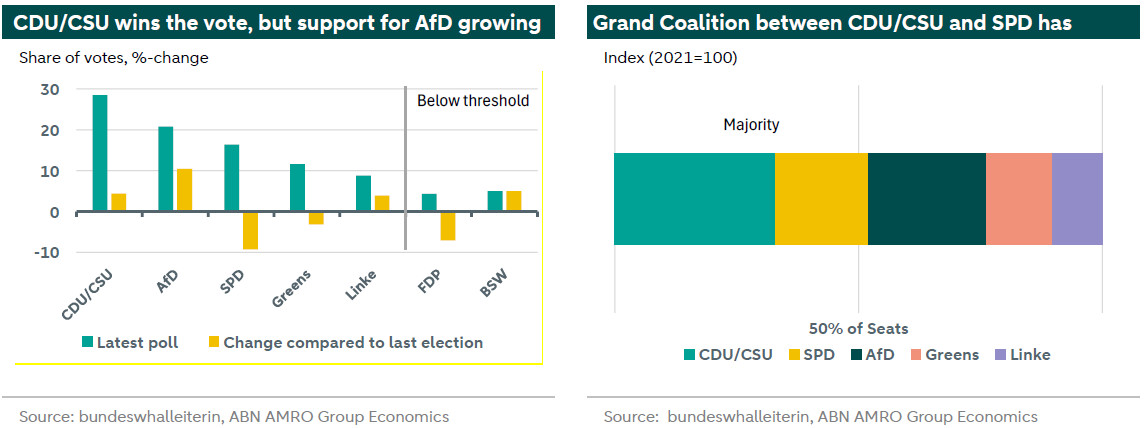

AfD and Die Linke are the biggest winners of the German elections, whereas FDP and BSW failed to reach the 5%-threshold, thus boosting the number of seats of the remaining parties.

Though the middle parties lost ground, Union and SPD are likely to form ‘Grand Coalition’ government once again.

Merz wants to reach agreement by Easter. Negotiations between Union and SPD will be tough though given the differences of their elections programs.

Even when supported by Greens, the ‘Grand Coalition’ can’t attain the two third parliament majority required to change the debt brake.

More fiscal space is needed to ramp up defence spending, which is urgently required given the changes in US governments’ security priorities.

This Spotlight is a follow up of our note Germany – ‘Groko’ likely amid further political political fragmentation

Sunday 23 February, Germans voted in a crucial election impacting not only their economy and domestic policies but also European policy-making amid geopolitical tensions involving Ukraine, NATO, and potential US tariffs. The highest voter turnout in decades underscored the importance of this election. In line with the polls, the CDU/CSU with leader Friedrich Merz has won the election. This puts the CDU/CSU in the driver’s seat for the coalition talks. Current chancellor Olaf Scholz’s Social Democratic party won just 16.4% of the votes, down around 10% from last election.

The liberal democratic FDP and far-left BSW failed to reach the electoral threshold, thereby boosting the seats of the remaining parties. This makes a two-party majority and the revival of the Groko (Grand Coalition) between the CDU/CSU and the SPD the most likely next coalition. Even more so as the Greens disappointed at just 12% of the votes which does not make them a possible alternative for the SPD.

The election underscored further political fragmentation – While a centrist ‘GroKo’ still seems the most likely outcome, it has to be noted that support for Germany’s traditional big parties has declined as the political landscape has further fragmentated. The far-right Alternative for Germany has recorded its best result yet, now 20.8% of the votes, roughly doubling their backing since 2021. In East-Germany, the AfD was often the biggest party. While Merz has vowed to keep the AfD behind the ‘Brandmauer’ i.e. excluding them from coalition talks, the AfD is set to become a dominant opposition party in parliament.

A new government by Easter? – Merz urged that formation talks should be quick to address the many challenges Germany faces as the “world out there will not wait for us”. As it stands now, a new Grand Coalition between the CDU/CSU and the SPD seems the most likely outcome. However formation talks are expected to be difficult. Most importantly as the SPD has clearly lost in the election. While the AfD has been quick to announce their willingness to support a CDU/CSU minority government, Merz has ruled out governing together with the AfD.

Merz inherits a challenged economic growth model – The next coalition will have to face Germany’s stagnating economy caused by a mixture of structural as well as cyclical headwinds which together challenge Germany’s export-led growth model. We do expect some cyclical improvement as consumer demand picks up, rate cuts feed through and frontloading effects – US firms increasing import orders in anticipation of tariffs – provide an impulse to exports. However, structural factors, such as high energy prices, a changed competitive landscape for German exporters and suboptimal infrastructure continue to weigh on the outlook. Together this underpins our expectations for a sluggish but positive growth rate of 0.4% in 2025 up from -0.2% in 2024. Still, Germany is expected to continue underperforming the broader eurozone.

The incoming coalition will struggle to find fiscal room to fund all of its ambitions – Supporting the economy, while reversing the course of infrastructure underinvestment, and ramping up defence spending, is all going to add up. The incoming government faces a difficult landscape how to free up fiscal wiggle room to fund these ambitions. Firstly because the current trajectory of public finances is one of already significant budget deficits. Merz, however, has voiced his intention to cut spending, especially on social programmes and welfare to free up space. The second challenge comes from changing the debt-brake, which looks difficult given the make-up of parliament. Currently the German constitution prohibits a structural deficit larger than 0.35% of GDP. Changing the constitutionally enshrined debt brake requires a two-thirds majority in parliament and the Bundesrat, and with the election results yesterday, the Left and AfD appear to have a blocking minority for any changes to the debt brake.

While a lot is uncertain at this stage, there could be three avenues forward. First, the debt brake has an emergency escape clause, for instance used during the pandemic. It is unclear whether the changing attitude of the US regarding European security and NATO would qualify as such an emergency. Second, the Left has indicated openness to change the debt brake (or allowing the creation of off-balance sheet funds) for instance for infrastructure spending, but is unwilling to do so for defence spending. It remains to be seen whether the incoming coalition can strike a compromise with them. A third option is to reform the debt brake before the new parliament takes office.

To form a coalition, the Union and the SPD will have to tackle various tough issues. Both parties entered the elections with very different programs, for instance regarding migration. The Union wants a much stricter policy that, according to the SPD, partly contravenes European rules. Nevertheless, given the strong growth of the AfD, it is likely that the Union and the SPD will tighten policies in this area. Support for Ukraine will also be more explicit than before. During the elections, Merz stated that the goal is for Ukraine to win the war, a formulation that Chancellor Scholz consistently avoided.

There are also differences in the tax proposals of both parties. The Union wants to abolish the solidarity tax, which was introduced after the fall of the Berlin Wall to finance German reunification, while the SPD wants to maintain it. Additionally, the Union wants to lower income tax rates and only apply the top rate at a higher income level. In contrast, the SPD wants to lower income taxes for the bottom 95% income groups and fund this by increasing taxes for the top 5% income groups. Furthermore, the Union wants to reduce corporate taxes, but the SPD fears that companies will use this advantage primarily to buy back shares. Therefore, they propose giving tax incentives to companies that invest. Finally, the Union advocates for lowering the VAT-rate for the hospitality sector, while the SPD advocates for reducing VAT on food.

Another point of debate is the rising pension costs and how to address them. The Union hopes to finance these costs by stimulating GDP growth. The SPD is more realistic, assuming that social contributions and taxes will need to increase. However, taxes and social contributions relative to gross income are already relatively high in Germany. There is little support in either party for the alternative proposed by think tanks—raising the retirement age.

Then there are welfare and the minimum wage. The Union wants to cut costs by abolishing the new welfare scheme introduced by the Scholz government, which is not popular among the public. The SPD is not in favour of this, although there seems to be some room within the party when it comes to sanctions for those who refuse to accept work. The SPD wants to raise the minimum wage from 12.82 to 15 euros per hour, but the Union wants the decision on the minimum wage level to be left to an independent committee designated for this purpose, which will give its verdict in June. Considering inflation, it is likely that the committee will decide to increase the amount.

Finally, both parties agree that energy costs need to be reduced, especially for businesses. Under the Scholz government, the electricity tax was temporarily reduced to the EU minimum of 0.05 cents per kilowatt-hour. Both parties want to make this reduction permanent. They also both endorse the goal of being climate neutral by 2045 and using more renewable energy. However, a difference is that the Union is open to nuclear energy. Furthermore, the Union and the SPD have different views on how the higher energy system costs should be borne. The Union wants to use CO2 levies for this purpose. In contrast, the SPD is considering a higher fee for the transmission network of 6.65 cents per kilowatt-hour and investments from a newly formed investment fund of EUR 100 billion.