US Watch – One month of Trump Tariff Threats

One month into Trump’s presidency, trade policy uncertainty has only increased, with wider, more ambiguous trade proposals, chaotic negotiations, backtracking and delaying. Based on the current set of proposals, Canada and Mexico are the most exposed. The proposed 25% tariff would also have a significant negative impact on the US. Reciprocal tariffs are likely less damaging to the US compared to the previously proposed universal tariff, but a lack of clear definition or upper bound on the tariffs leaves great uncertainty around the potential impact.

Barely a day has passed during Trump’s first month in office without a tariff headline in the major news outlets. Less than two weeks after his inauguration we were close to substantial tariffs on the US’ closest trading partners, Mexico and Canada, only for them to be postponed by a month at the very last minute. Over the course of Trump’s first month, we’ve seen a large number of different tariff proposals, which can be grouped into two categories: economic and political. The basic premise of the universal tariff touted during the election campaign was economic; reduce the trade deficit, bring back jobs and fund tax cuts. Since then, we’ve seen tariffs being used as economic threats to obtain political goals; reducing immigration, forcing nations to accept their deported citizens, and even a tariff threat to Denmark over the US’ potential claim on Greenland. The threats have increasingly become interwoven with geopolitics, such as the suggestion that any retaliatory tariffs from the European Union might be met with a withdrawal of the US’ defence commitment to Europe, to the extent that Europe can still rely on the US as it stands.

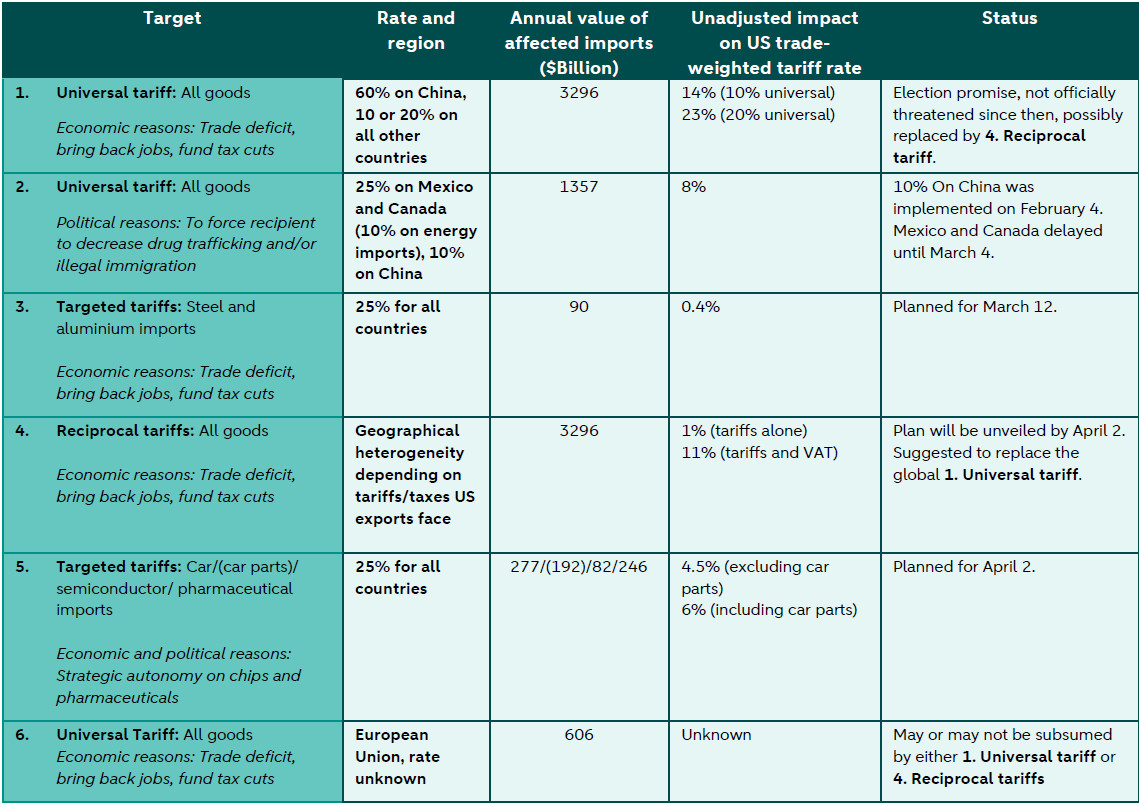

This piece evaluates the most credible tariff threats in Trump’s first month in office. These are distilled from the administration’s ‘flooding the zone,’ trying to identify plausible threats from the general, mostly uncoordinated, barrage of rhetoric stemming from the various policymakers. The table at the end of the document summarizes these proposals (labelled 1-6 in the text below), their scope, estimated impact on the overall tariff rate of the US based on current levels of trade, and their current status.

The universal tariff (1) proposed during the election is all but off the table. The only new tariffs (2) that have actually been implemented are a universal 10% on China, and . The Canada and Mexico part of that package has been delayed, and we assess the likelihood of it being implemented at full strength as relatively low. Steel and aluminium tariffs (3) were also proposed and enacted in the first Trump administration, and at least a partial implementation seems likely, with some exceptions for certain qualities that the US does not produce itself, but the overall level of tariffs applied will likely rise. The latest is a 25% tariff on cars, chips, and pharmaceuticals (5). Whether car parts are included in the plan is unclear at the time of writing, so we consider both scenarios.

Reciprocal tariffs (4) are the new name of the game, effectively replacing the threat of universal tariffs (1). The details are unknown and currently developing, but the baseline expectation is that the US would put tariffs on its trading partners to at least equate the tariffs to the average tax levied on US exports to that country. However, Trump has brought other supposed trade barriers into the mix, such as VAT, and food safety standards that prevent US exports. These are clearly not formal trade barriers, as VAT impacts both imported and domestic goods. These wider trade barriers are particularly hard, and arbitrary, to quantify, but are most likely an attempt to recast the implementation of high tariffs into a national emergency or unfair trade practice package. We consider two scenarios; i) a simple country-by-country equation of average tariffs and ii) tariffs raised to the sum of the tariff the US faces and the country’s VAT rate in excess of the average US sales tax. The latter leads to substantially higher tariffs but is not necessarily an upper bound; the prospect of the US also countering non-tariff barriers leaves space for even higher tariffs.

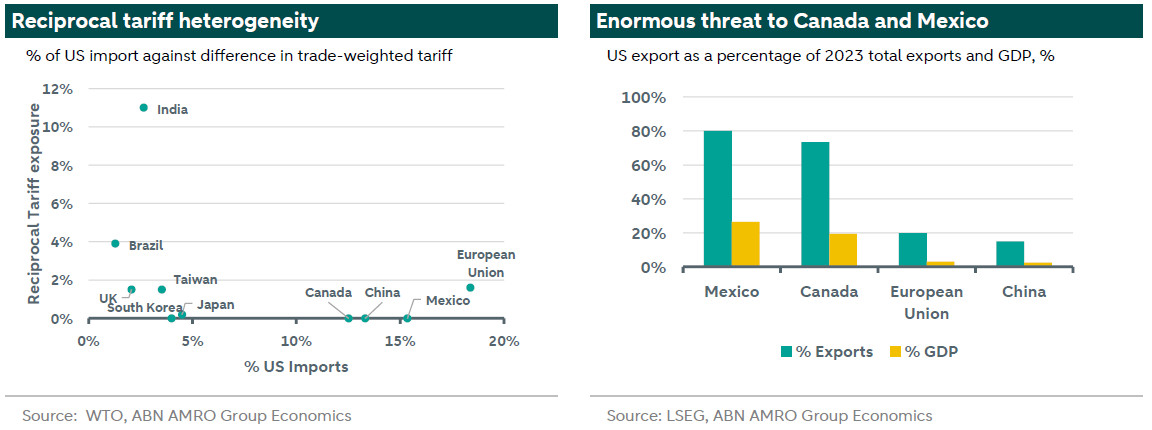

The chart below shows the exposure of the US’ major trading partners to (non-VAT) reciprocal tariff rises. Exposure is generally larger in emerging markets, which tend to apply high tariffs to all imports to protect developing industries. Out of the major non-EM trading partners, the European Union is the most exposed to reciprocal tariffs, mainly because of the US’ free trade agreements with Mexico and Canada (USMCA) and the fact that China already faces high tariffs on US exports, especially after the recent increase (2). At the same time, Europe’s tariff differential is small, but VAT and non-trade barriers may quickly raise the reciprocal tariff exposure, and Trump has threatened wider tariffs on Europe, without being specific (6).

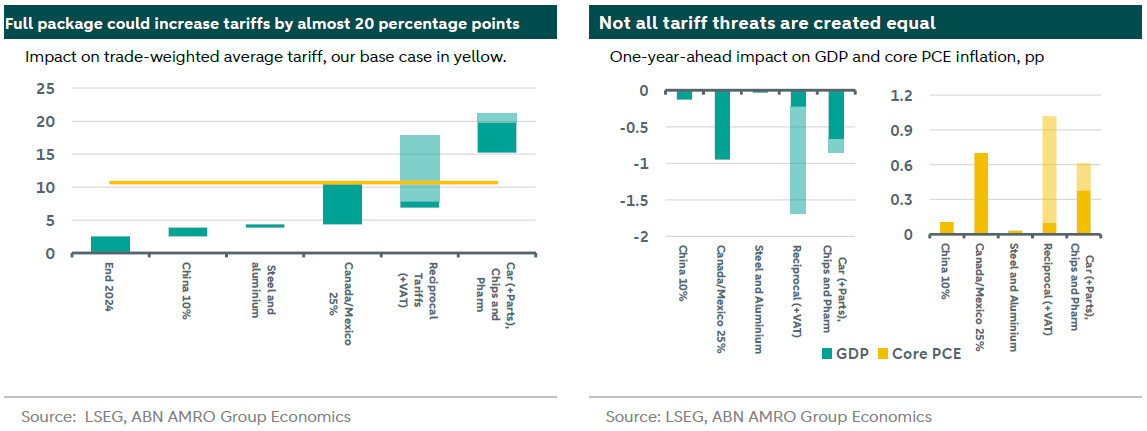

There is of course some overlap between the various tariffs. The chart below provides an estimated impact on the overall US trade-weighted tariff, with the bars on the right being shifted down by the amount of overlap with other tariffs preceding it. The primary origin of overlap is that Mexico and Canada likely won’t be subject to additional targeted (3 and 5), nor (VAT-based) reciprocal tariffs (4) in case the 25% tariff is applied to all their imports (2). This leads to substantial overlap between (2), (4) and (5). In such a scenario the additional impact of the overall reciprocal tariff (with VAT) would be reduced by about 4%. Mexico and Canada similarly account for a large part of car imports, making up more than half of the value of car and car part imports, with the European Union about 15% of car imports but less in car parts. Out of the major trading partners, 12% of semiconductors comes from China, and about 7% from Mexico, while Malaysia and Taiwan are the primary exporters. Roughly half of pharmaceuticals come from the European Union, an additional 12% from Switzerland, and 5% from both India and the UK. This leads to about 3.5pp in overlap between the potential Reciprocal Tariff (4)and the car/chips/pharmaceuticals tariff (5). As a result, while the individual tariffs sum up to over 25%, a full implementation of all the tariffs would increase the trade weighted tariff by less than 20%. Substantial compared to the 2.5% at the start of the year, and significantly higher than our current base case of just above 10%. Indeed, the risk of tariffs exceeding our baseline assumptions has steadily increased over the course of the past month, gradually increasing the probability of more adverse outcomes for the US economy. At the same time, trade policy uncertainty is at an all-time high, and there are many scenarios in which the ultimate implementation of these proposals would result in tariffs around our base case level.

We estimate the one-year-ahead impact of the various tariff proposals on growth and inflation. Similar to our , the impact on both prices and GDP is estimated to be quite permanent. Inflation rises but wanes once the price increases drop out of the y/y rate. GDP gets a negative shock and sees no strong recovery after. The estimated impact is for individual tariff measures, and it is important to realize that the joint impact of two proposals does not simply sum up, because of i) overlap between the tariffs, and ii) non-linear interaction effects.

Starting with the simple ones; the already implemented China tariffs and proposed steel and aluminium tariffs have a relative mild impact, through a combination of limited value of imports and/or moderate rate. The exposure of the US economy is simply too small to show a large impact on headline figures.

The other three measures are decidedly more impactful. Due to USMCA, value chains are heavily dependent on the free trade between Canada, Mexico and the US, and the two countries make up almost 30% of total US imports. Due to the non-universal nature, trade flows would gradually adjust due to rerouting and diversion, but not all activity would move to the US. We estimate a negative impact of the Canada/Mexico tariffs (2) of about 1% on US growth, while core inflation is estimated to increase by about 0.6% due to the tariffs.

The reciprocal tariff (4) by itself is relatively benign. The implied tariffs are low as the largest tariff differentials are with small trading partners. A VAT inclusion, or wider scope through non-tariff trade barriers, would push the impact up substantially, particularly through trade with the major trading partners: Mexico, Canada and Europe. The latter would be hit with the highest tariffs. The heterogeneous nature means we would see some trade reroute, but all the major trading partners are hit with additional tariffs, limiting scope for substitutability and amplifying the impact. The GDP and inflation impact (-1.7 and 1.0% respectively) scales more than proportionally with the trade-weighted tariff impact compared to the Canada/Mexico 25% tariff.

The cars, chips and pharmaceutical tariff (5) is similarly impactful through the sheer volume of trade, affecting almost a quarter of total imports at a substantial rate. The universal nature makes it impossible to substitute geographically, amplifying the relative impact. We estimate a 0.8% hit to growth and 0.6% increase in core inflation.

Overall, the potential impact of the various tariff threats is large, both on the US, and especially its neighbors and key trade partners. In isolation, the various proposals increase inflation and dampen growth, but are not enough to steer the US into a recession. The overall joint scope of the tariffs may be enough to push the US in that direction, depending on timing and ultimate implementation. The Fed would be put in a precarious situation, with quickly slowing or potentially negative growth, and elevated inflation. Canada and Mexico are most exposed, and tariffs on them would also have the largest relative impact on the US. That particular tariff’s deadline is approaching rapidly, and developments in the coming weeks will be crucial for the continent’s economic outlook.