Macro implications of the US Elections - Trump tariffs cause a recession

Democrat victory only marginally alters the US’ economic trajectory, Republican victory blows it off course. A full-scale implementation of the Trump-tariffs will increase inflation and put the US in a recession. The impact on the economy is as permanent as the tariffs, output and price levels do not recover. A partial victory, where Congress is divided, improves economic outcomes relative to full victories.

The US presidential elections are rapidly approaching. The two parties’ plans for the economy, such as tax, trade and immigration policy, differ greatly. We simulate the impact of the proposed policies on the US economy over the next presidential term. We focus on high-level economic outcomes such as growth, inflation, (un)employment and the Fed policy rate based on planned changes in corporate and personal taxes, tariffs, government expenditures and immigration policy.* We construct projections of the US economy conditional on a particular election outcome, without weighing the probabilities of such outcomes. Indeed, the aim of this piece is to objectively analyse the implication of the proposed economic plans, not to provide a direct projection for the US economy up to 2028.

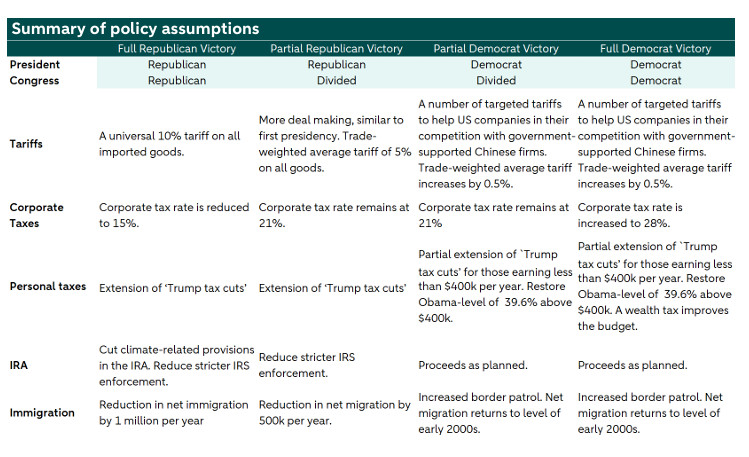

Our assumptions on Trump’s policy plans are based on his campaign website, various speeches and interviews. We do not explicitly include the Project 2025 policy plans, because of their disputed nature and because they are sometimes at odds with Trump’s own communication. President Joe Biden just announced that he withdraws himself from the presidential election. The current frontrunner to replace him, endorsed by Biden himself, is vice-president Kamala Harris. We do not think that the ultimate candidate will follow a dramatically different economic policy from the one originally planned by President Biden. We therefore base our assumptions for the Democrat candidate’s economic plans on the fiscal 2025 budget proposal. Should significant changes occur, we will update this analysis. An overview of our explicit assumptions on the policy plans are provided at the end of this document.

We consider four different election outcomes, which differ in who wins the presidential election, and in which party gains control of the Senate and the House. The House is currently Republican, while the Senate has a Democrat majority. This is unlikely to be the outcome of the upcoming election. To take the Senate majority , the Republicans only need one of five seats where polling suggests a tight race. As for the House, the Democrats would need to take four additional seats to obtain a majority. Current polling suggests this is not an impossible outcome. Based on these considerations, there is a Full Republican Victory, where Trump wins the presidency, and Republicans control both the House and Senate. In a Partial Republican Victory, Democrats obtain the House majority. In such a scenario Trump will face more difficulty following through on any plans that he cannot pursue using executive orders, in particular tax policy. He will not succeed in his intended tariff policy, but has to settle for a weaker and non-universal tariff. In a Full Democrat Victory, Democrats win the presidency and control Congress, allowing them to implement the full fiscal proposal. In case the Senate flips Republican, it will again be predominantly the tax policies that will be difficult to implement. We compare these scenarios with a reference scenario where current policies remain in place.

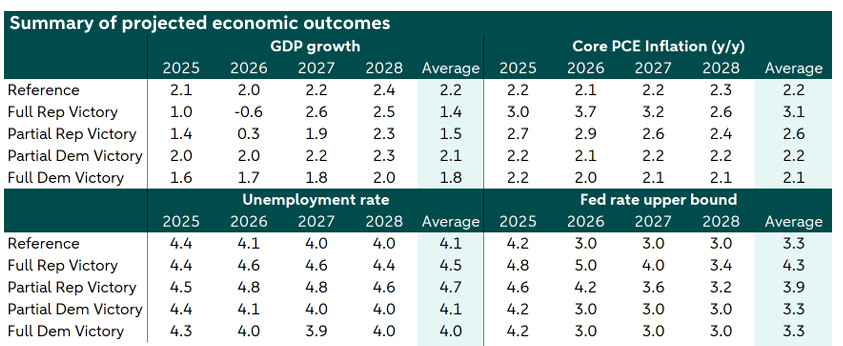

The findings can broadly be summarized as follows. A Full Republican Victory, and particularly the implementation of the universal tariff, will push the US into a recession. Inflation will rise substantially and stay elevated for most of the term. The stricter immigration policy leads to weaker labor supply when demand falls from the recession, such that the recession’s impact on unemployment is relatively small. As a result, the Fed has no reason to refrain from rate increases and fights inflation. The trade balance improves initially, but deteriorates in the long run. In case of a Democrat victory, the economy largely continues its current trajectory. Inflation will come down to target as expected and the Fed will start lowering rates. The corporate tax increase somewhat dampens growth, but has the benefit that the government debt-to-GDP ratio does not increase over the presidency. By the end of the term, growth, inflation, unemployment and the Fed rate are at similar levels for the two parties, but output, price level and total employment are substantially worse in case of a Republican victory. A full overview of the projections under the five scenarios is presented at the end of this document.

A Republican victory

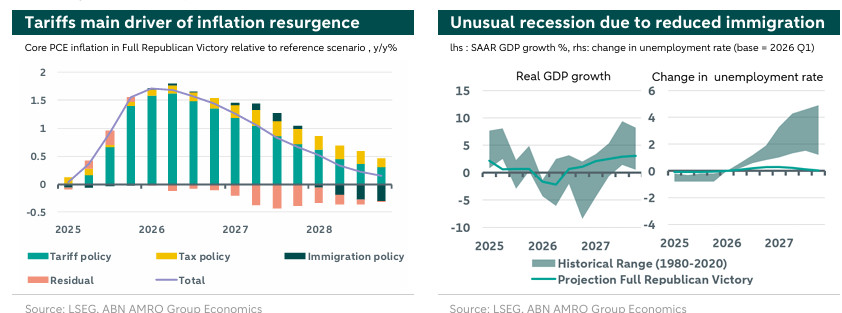

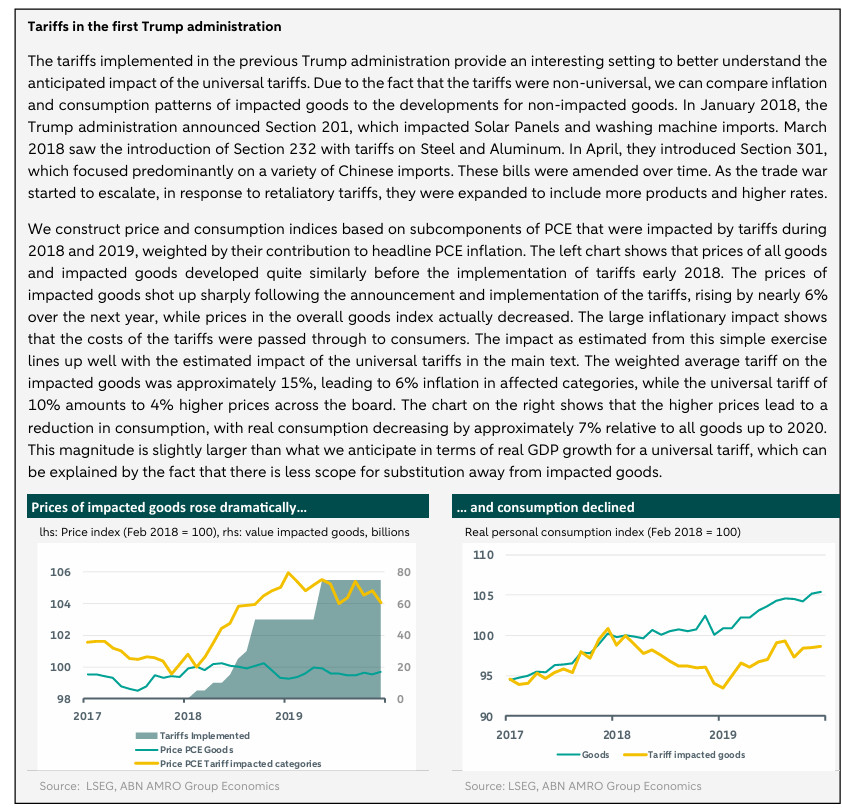

We start with the implications of the full Republican Victory scenario, which leads to three major policy changes. First, there will be a 10% universal tariff**. Second, the corporate tax rate will be reduced to 15%, and third, immigration will be reduced significantly. The impact of the universal tariff is large. First and foremost, there is an immediate impact on inflation. The higher cost of imported goods will gradually be passed through to final goods. Inflation increases by up to 1.7% relative to the reference scenario, almost fully attributable to the increase in tariffs (lhs chart below). There is additional inflationary pressure from the fiscal stimulus of the tax cuts, but a limited impact of the weaker labor supply induced by stricter immigration policy, as the economy is slowing at a similar pace. The dampening impact captured in the residual component encompasses, amongst others, the indirect effects of an exchange rate appreciation. The tariffs do not achieve their policy goal of improving the trade balance. They initially reduce import demand sufficiently to reduce the U.S. trade deficit, but as exchange rates react and retaliatory tariffs are implemented, the overall trade balance deteriorates relative to the reference scenario.

Growth suffers on the back of more restrictive Fed policy and weaker demand, leading to a mild recession by the first half of 2026. Facing a recession while inflation is above target, the Fed would usually be in a difficult situation. However, due to a reduction in immigration, and even active deportation, the labor force grows at a strongly diminished pace, and the unemployment rate never really takes off. The fed reinitiates a hiking cycle to bring inflation back down, as it is much further from target then employment.

By 2028, GDP growth and inflation are largely back in line with the reference no-change scenario. However, that convergence in pace comes without a recovery from the initial shock. The level of real GDP stands at 3% below the level in the reference scenario, and price levels are 4% higher. The unemployment rate is similar, but there are approximately 3.25 million fewer jobs. In addition, the Government debt will rise considerably as a result of the deficit-financed corporate tax cuts, as tariff income is insufficient to cover the cost. Any benefit obtained from the reduction in climate-related provisions in the IRA, is lost because of the unwinding of stricter IRS enforcement. The reduction in clean-energy investments will likely have consequences beyond the President’s term.

Would the outcome differ substantially in case the Democrats control the House? In order to circumvent Congress, Trump will need to declare a national-security emergency to impose his trade policies. This emergency is unlikely to hold up to court scrutiny for a universal tariff, but may stick for China and a few other countries, leading to a trade-weighted average tariff of 5%. Trump would also face more opposition in the costly process of actively deporting immigrants, and net immigration would be reduced to a lesser extent. He would be unable to find sufficient support in congress for the decrease in the corporate tax rate. The overall outcome is a milder variant of the Full Republican Victory scenario described above. Inflation would increase less dramatically, growth would slow, but a recession would be averted. At the same time, the unemployment rate would rise to a higher level as the labor force grows more quickly. Regardless, the Fed will still pursue a higher for longer policy. As for the government’s budget, the administration reduces the stricter IRS enforcement, but fails to cut climate-related provisions. The government’s debt-to-GDP ratio still increases, but less strongly than in the Full Victory scenario, due to the failure to cut corporate taxes.

A Democrat victory

In case of a Full Democrat Victory, the economy largely continues on its current trajectory. The increase of the corporate tax rate to 28%, and package of increases in personal taxes for higher income households help to balance the budget and limit the increase of Government debt. These measures are enough to flatline the debt-to-GDP ratio, which still increases under the reference scenario. However, the increase in corporate tax rate comes at the cost of a slowdown in growth of about half a percentage point per year, as seen in the lhs chart below. This slow-down helps in getting core PCE inflation down slightly quicker but it has no material impact on the Fed policy, which, similar to the reference scenario, eases over the course of 2025 and is stays at the neutral rate after.

In the event of a Partial Democrat Victory, the government fails to increase the corporate tax rate and to implement a wealth tax. They manage to increase the personal tax rate in the top bracket since the ‘Trump tax cut’ simply expires, while extending the tax cut for lower income households. The result is that we end up in a scenario that is very close to the reference scenario of no change, with only a minor impact from some small tariff increases. There is still an improvement in the government budget, and the debt-to-GDP ratio only shows a small increase over the presidency. This scenario results in slightly lower average growth compared to the reference scenario, but the highest overall growth out of the four election scenarios. Indeed, we also expect that this scenario would create the most jobs, even exceeding the job creation in the reference scenario.

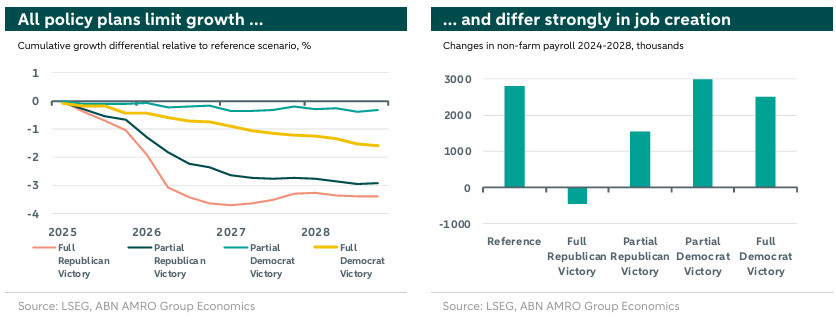

We conclude that the economic outcomes under a Republican presidency are objectively worse. The deterioration in the inflation and growth trajectories can be almost fully attributed to the tariffs, while decreased corporate tax rates and a reduction in IRS enforcement push up government debt. Immigration plays a significant role in that its reduction gives the Fed little alternative to focus on to fight inflation, keeping rates higher for longer. It is not inconceivable that the degree of proposed tariffs could be election rhetoric, and will ultimately be implemented in a much weaker form, similar to the first Trump presidency. A Republican Victory scenario without the tariffs is decidedly more benign from a growth perspective, but still not fiscally prudent. In case the Democrats win the presidency, the economy, perhaps unsurprisingly, largely continues its current trajectory.

* - The analysis presented in this document is based on a large Bayesian VAR specifically designed to assess these policy changes. Our official projections are based on a careful weighing of a various scenarios and do not coincide with any of the individual scenarios presented here. The reference scenario in this document is a no-change scenario, rather than the baseline scenario in our projections.- A large part of the policies is redistributional in nature, which provides another measure to evaluate policies. While we do incorporate taxes and credits in various parts of the income distributions as part of the policies in our model, we focus on the aggregate macro outcomes only.

** Trump has suggested to even put a 60% tariff on all goods imported from China. We think it unlikely that such a large tariff will be implemented abruptly, but rather in incremental steps. The 10% universal tariff can therefore be interpreted as a conservative initial implementation.