What Trump’s latest tariff threats may mean for Europe

As the US approaches key deadlines, the news flow is likely to switch over the coming weeks back to tariffs. We explore what the latest threats mean for the eurozone and Dutch economies. While the situation is fluid, we judge that the risk of stagnation – or even recession – has moved higher.

Has it really only been one month?

Last week we taking stock of US tariff developments. Hard though it may be to believe, we are only a bit over one month into Trump’s presidency. While we thought 2025 would be the Year of the Tariff, even we have been surprised by the scale and speed of announcements. In this note, we look more specifically at the threats affecting the eurozone. Our base case was for a significant rise in US tariffs this year that would lead to a sharp fall in eurozone exports to the US, putting the brakes on the nascent recovery. While US-EU negotiations last week (see below) are a positive development, the threats that have been made, if anything, point to a more negative scenario than our base case. Another recent moving part in the outlook – higher defence spending – pose some upside risks to growth, but any impulse on this front looks in our view likely to be overwhelmed by the drag on exports from US tariffs.

Tariffs on cars & pharma have the most likelihood to be damaging

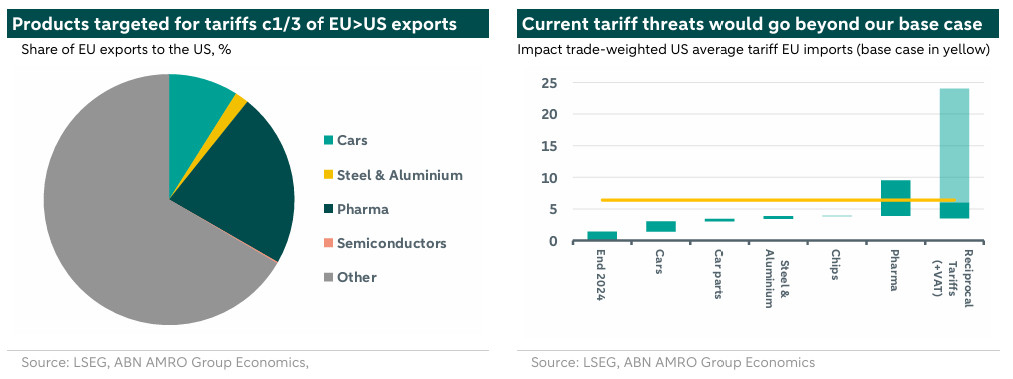

Of the trade measures proposed so far (see here for a full summary), the most consequential for the eurozone are 1) reciprocal tariffs, 2) a 25% tariff on cars, aluminium & steel, chips and pharmaceuticals. Most of these measures could be implemented on 2 April; steel & aluminium even sooner, on 12 March.

Reciprocal tariffs involve the US matching the tariffs of its trade partners, per product item, wherever that tariff is higher. By itself this would not be particularly damaging to the EU, because tariff rates are actually not all that higher than the US. We estimate the weighted average tariff rate on EU goods would rise by c2.5pp if the US were to match the EU’s tariffs on US goods. The wild card is that the US administration has started calling VAT a trade barrier, which it is not, because VAT is charged at the same rate on all goods, domestic and imported. Still, a tariff that would seek to compensate for differences in sales taxes between the US and EU would have a far greater impact on the US tariff rate, raising it by some 18pp. While difficult to justify, the US administration may well use this as a pretext for a massive rise in tariff rates that it in any case wants to implement. We refrain from speculating on that at this point, suffice to say that the scale of this threat makes a more negative scenario more likely. An arguably more concrete threat comes from the proposal for a 25% tariff on all car, steel & aluminium, pharmaceutical and semiconductor imports. Together, these products make up around 1/3 of the EU’s exports to the US, and if these tariff rises were to be implemented, they would raise the weighted average tariff on EU imports by some 8.1pp, from 1.4% to 9.5%. By far the biggest impact would come from the tariff on pharmaceutical exports, with a 25% tariff adding 5.6pp, followed by cars & car parts (c2pp), aluminium & steel (0.5pp) and semiconductors (0.04pp). These differences reflect the differing share of exports to the US.

As discussed in our note last week, it is unlikely that all of these measures would be implemented in a compounding way, i.e. any reciprocal tariff (especially involving VAT) would have significant overlap with the product-specific tariffs. This is visible in the chart below.

What does this mean for our base case?

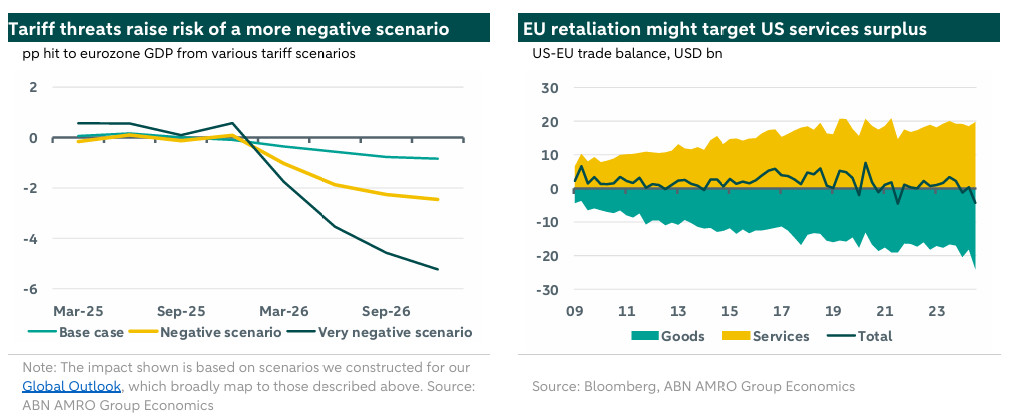

Our base case assumes a 5pp rise in US tariffs on EU (and other ex-China) imports. While reciprocal tariffs without taking account of VAT would still be within the bounds of that base case, the other measures discussed above would clearly put us well beyond our base case, and closer to the more negative scenario we sketched out in our Global Outlook. 25% tariff on pharma, cars et al would drive a sharp fall in eurozone exports and cause a stagnation in the economy, in contrast to our base case for a slowdown to well below trend growth. In the very negative scenario where the administration sees VAT as a trade barrier that needs to be offset, such a sharp rise in the average tariff rate would likely tip the eurozone economy into a recession, with non-linear second round effects coming from a rise in unemployment and a fall in consumer confidence (see chart on next page).

How might the EU respond?

Aside from the uncertainty over what the US’s ultimate policy goal is – is it revenue-raising, or is it a genuine desire to boost US exports? – there is also the uncertainty of how the EU plays its hand, both in negotiations and in any possible retaliation. EU trade commissioner Maros Sefcovic was in Washington last week for talks with president Trump’s trade team, where officials were quoted claiming there was ‘positive momentum’ in the talks, which mostly focused on car tariffs. The EU is reportedly open to lowering its own tariffs as part of a deal, and talking up the potential to buy more US LNG as the continent continues to transition away from Russian gas.

Should the US go ahead with steep tariff rises, we continue to think any EU retaliation will be targeted and aimed at politically sensitive goods, meaning its impact on inflation should remain limited. If this does not succeed, the EU could deploy its ‘bazooka’, the anti-coercion instrument (ACI). While the US has a trade deficit in goods with the EU, it enjoys a significant surplus in services, largely thanks to the dominance of US Big Tech.

The ACI would seek to hit the US services surplus through some potentially extreme measures, including: suspension of intellectual property rights, for example allowing free use of software, and applying duties to streaming services and other digital platforms. Trump’s nominee for Chair of the White House Council of Economic Advisors, Stephen Miran, has proposed putting US defence on the table if the EU threatens to respond aggressively to US tariffs. But with the US already significantly watering down its defence commitment to Europe, this arguably weakens the US’s hand.

The economic consequences for the Netherlands

Compared to the broader eurozone, the newly announced 25% targeted tariffs on steel, aluminum, and since last week also cars, pharmaceuticals, and semiconductors, would raise the effective tariff rate for the Netherlands by 4.2pp. This is lower than the estimated 8.1pp for the eurozone aggregate. Pharmaceuticals alone account for roughly 3pp of the increase in the trade weighted tariff rate for the Netherlands, as they comprise a significant portion (13.5%) of Dutch exports to the US. Given the critical role of semiconductor manufacturing equipment, like those produced by ASML*, to the US industry, we anticipate this sector will remain exempt from potential tariffs. Should it be included, the effective tariff rate could rise by an additional roughly 2pp. In the previous tariff case, exceptions were made for the steel sector, such as Tata Steel being from the tariffs due to its production of steel products not manufactured in the US. It is possible that similar exemptions could be granted again, which would mitigate part of the rise in the tradeweighted tariff rate.

(*As we wrote in a previous note, Dutch company ASML is increasingly becoming caught up in US-China rivalry. recently, reports indicate Trump officials spoke to Japanese and Dutch counterparts on restricting engineers from companies Tokyo Electron and ASML to maintain their semiconductor gear in China. This could prove to be a source of leverage in the US-EU negotiations. )

Considering only these product-specific tariff rises, the rise in the trade-weighted tariff rate approaches our base case scenario of a 5pp increase. Similar to the eurozone, factoring in potential reciprocal tariffs of approximately 2.5pp would push us beyond our base case scenario. As previously explained, the VAT wildcard could significantly raise the tariff rate, meaning we would move to a more negative scenario for Dutch growth. While some overlap between the reciprocal and product-specific tariffs is expected, these plans could substantially increase the tariff rate from the initial effective rate, estimated at around 1.4%

, the Netherlands is a trade-oriented country with a high degree of participation in global supply chains, exporting high value-added goods to the US, and serving as a gateway to the European mainland. Consequently, it stands to be significantly affected by tariff rises. Approximately 6% of Dutch goods exports are destined for the US, with around 20% being re-exports and 80% Dutch-made goods. Exports of domestic produce have a larger value-added, with the GDP contribution of domestic produce exports to the US averaging 0.8% of GDP (average 2015-20) according to .

is both direct and indirect. Directly, higher trade costs with the US will reduce demand for Dutch goods, thereby decreasing the volume of goods traded. This was also evident in the previous tariff period when exports of sanctioned steel products to the US dropped significantly: steel exports were than in 2018. Indirectly, the tariffs will lead to lower world trade volumes and slower eurozone growth. Given the US economy’s global influence, these tariffs will have a global knock-on effect, thereby also indirectly hurting the Dutch economy.