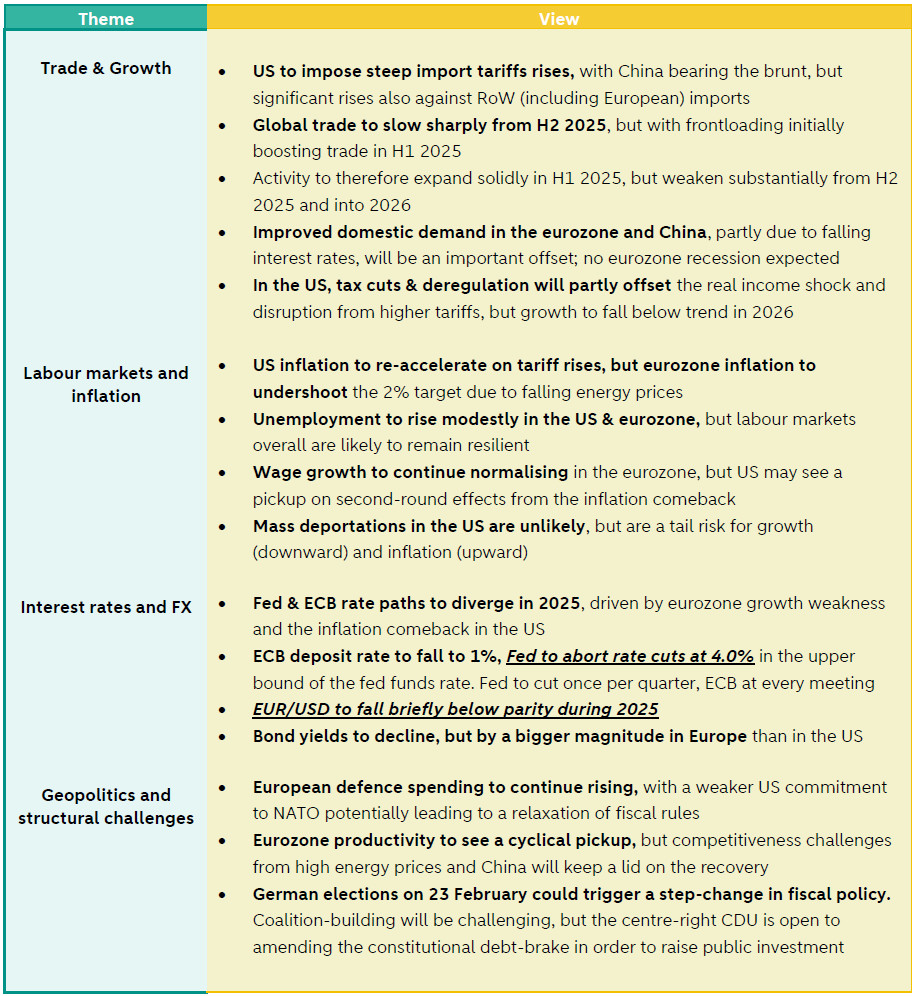

Global Monthly - Buckle up – this is just the beginning

The early days of the Trump administration have been predictably chaotic. Businesses and investors had better get used to the new environment of radical policy uncertainty. An earlier end to Fed rate cuts is likely to drive the euro below parity later this year. This will take the edge off of the tariff blow to European exports, but it won’t fully offset it. Still, Europe isn’t powerless: the EU has long prepared for negotiations with Trump, while the German election could free up much-needed investment to deal with structural competitiveness challenges. We preview the German elections in the first of a series of articles in this month’s Spotlight*. Regional updates: The consumer is finally waking up in the Eurozone, helped by ECB rate cuts, while in the Netherlands, stronger domestic demand is likely to partly offset looming headwinds for trade. In the US, the goldilocks economy is back for now, but Trump policies will likely put an end to Fed cuts. China is seeing tailwinds from Beijing’s policy pivot and trade frontloading, ahead of likely US tariffs.

Global View: Europe isn’t powerless to the challenges of Trump, but it won’t be easy

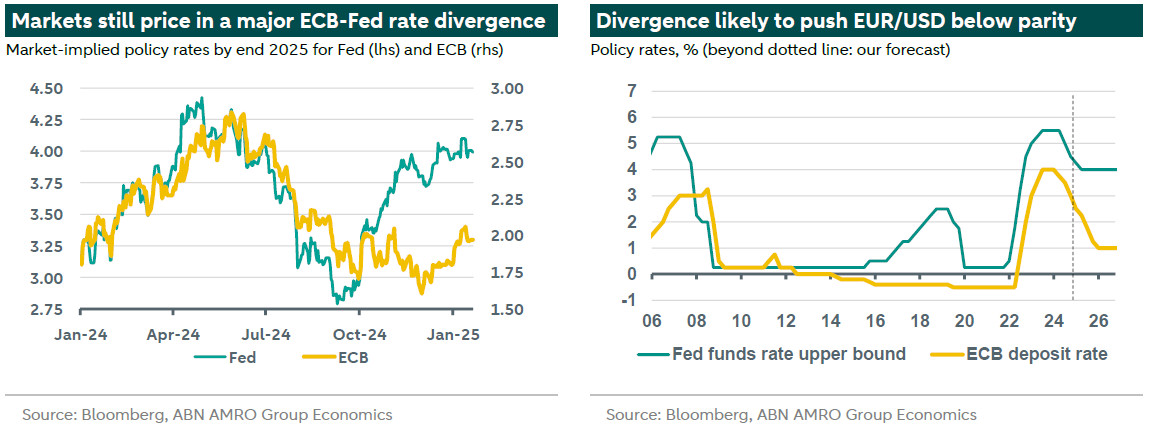

Only three days into Trump’s second term as president, and if anything has been predictable, it is the chaos. For a while, it appeared China, Mexico and Canada had been spared immediate tariff rises after some positive phone calls. If we take Trump’s & 2 comments literally, the US’s neighbours could be hit with 25% tariffs on 1 February, and China could be hit by an additional 10% tariff. China has even been threatened with 100% tariffs if it does not agree to a partial sale of TikTok. The saga is an illustration of the new, volatile policy environment we find ourselves in, where anything could happen on a given day. It won’t be long before Europe enters Trump’s tariff cross-hairs – as his comments overnight suggest – but the administration supposedly is not yet ‘ready’ for universal tariffs. Our base case continues to foresee a significant rise in tariffs on European imports in the second half of 2025, putting the brakes on a fragile eurozone recovery. For now, the global economy is not doing too badly. US growth momentum remains solid, notwithstanding some cracks below the surface; the eurozone consumer is finally waking up – partly helped by ECB rate cuts; and China is seeing a lift from more stimulus, as well as a front-loading of trade ahead of probable US tariffs. As for central banks, we now expect the Fed to halt rate cuts even sooner – after June – while for the ECB, the growth threat from tariffs continues to point to the deposit rate falling to 1% by early 2026. The earlier end to Fed cuts implies an even bigger divergence in rates, and therefore an even weaker euro: we now expect EUR/USD to fall briefly below parity to $0.98 by the end of the year. Might the weaker euro keep the eurozone economy on an even keel? It will certainly cushion the blow of tariffs, but it will not fully negate it. As described in our , while we expect a 5pp trade-weighted rise in tariffs, much bigger tariffs are likely on products where US companies stand to gain market share, and it is through these sectors that the drag on eurozone growth is likely to materialise.

Europe faces enormous challenges from the new Trump administration – to put it mildly, particularly given that tariffs may be used for broader political goals under Trump 2.0. But it is not powerless to deal with them. Aside from the the European Commission can use in response to US tariffs, in the country that faces the biggest challenge from tariffs – Germany – the election on 23 February presents a golden opportunity to respond to the new geopolitical and economic environment. In the first of a series of publications covering the elections, this month’s Spotlight describes the key themes and policies of the various parties, and discusses the likelihood of Germany’s debt brake being eased to help free up much needed funds for investment. Germany is one of the few eurozone countries that has the fiscal space to tackle structural challenges in a more ambitious manner, and while forming a coalition won’t be easy, the two main parties most likely to be part of the next government at least appear open to change. This will be crucial, because the challenge of Trump to Europe’s prosperity will likely require radical solutions.

---

In the below table, we summarise our key judgement calls and assumptions for macro and financial market developments in 2025. We’ve made some updates (in italics) where views have changed since the publication of our Global Outlook in November.