ESG Economist - Are US tariffs a catalyst for EU energy transition?

The world we are living in is changing at a fast pace where a decades-long pro-globalisation stance is being challenged by the vulnerability of supply chains during the COVID pandemic and the energy crisis after that. Furthermore, faced with domestic challenges and the rise of nationalism, the prioritization of domestic agendas has come to the fore in many countries. The most recent development in this regard is the (proposed) new tariffs imposed on imports from several trading partners by the new US administration, along with a rolling back of climate policies. This opens the door to multiple scenarios of retaliation and the rise of trade wars between the US and its trading partners (see our most recent macro notes on the subject (1) and (2)). These trade conflicts could affect trade flows, growth rates, and transition pathways all over the world. In this note, we revisit the concepts of free trade and the role of its international governing body, the WTO. We also outline the main channels by which a US invoked trade war affects the transition process in the EU highlighting the main impacts on cost structures and supply chains. We end with a conclusion. This note is the first part of a series analysing the impacts of trade war on the energy transition.

A US-triggered trade war would decrease trade flows and weigh on global growth, with the EU potentially experiencing lower inflation

This could lead to divergent monetary policies, where the ECB might cut interest rates much further, reducing financing costs for the EU's energy transition

Furthermore, US tariffs and the roll-back of the US energy transition could reduce demand and therefore prices of transition technologies from China

Accordingly, the EU may capitalize on reduced technology and financing costs, while facing challenges from increased competition with Chinese products

On the other hand, a trade war could lead to lower fossil fuel prices which would increase the opportunity cost of climate investments, prolong the use of fossil fuels, and induce a slowdown in the transition process

Overall, as long as there are no additional tariffs between the EU and China, a US-only trade war may have positive spillovers for Europe’s energy transition

Free trade and the WTO

Trade barriers could take many forms such as tariffs, quotas, embargoes, sanctions or regulations. Tariffs are the most common trade barrier, which represents additional surcharges on imports at the border before entering domestic markets. In principle, tariffs shields domestic producers from international competition. Lower competition would allow domestic producers to increase prices and profits. But, at the same time, such protectionism could also induce lower efficiency in resource use. At the same time, higher domestic prices would put an upward pressure on inflation and reduce the purchasing power of consumers. This last effect is mitigated by an increase in employment and wages. All in all, in general, tariffs would be advantageous for producers on the expense of consumers. These impacts are reversed under free trade where trade barriers are minimal.

From a pure economic perspective, removing trade barriers would allow every country to specialize in the production of goods and services it has a comparative advantage in, while relying on imports for other products. This would achieve high efficiency in resource use. Accordingly, in principle, free trade would benefit trading partners alike, where the importing country enjoy higher quality products with lower prices, while the exporting country gains higher profits from its accession to new markets. However, free trade would also entail higher level of globalization where supply chains for different products become more complex and spread over several countries associated to a specific cost structure. Accordingly, vulnerability to supply chain disruptions increase.

Countries have recognized the advantages of free trade by engaging in various trade agreements, both regional and international, with the World Trade Organization (WTO) playing a key role in reducing trade barriers. Established through negotiations under the General Agreement for Tariffs and Trade (GATT), the WTO aims to lower tariffs and promote non-discriminatory trade practices through principles like Most-Favoured Nation and National Treatment. While countries can unilaterally lower tariffs, increasing them requires justification, and exceptions to non-discrimination are allowed under specific conditions, such as unfair trade practices. The WTO also offers a dispute settlement mechanism to address trade disagreements among member states.

International trade and the energy transition

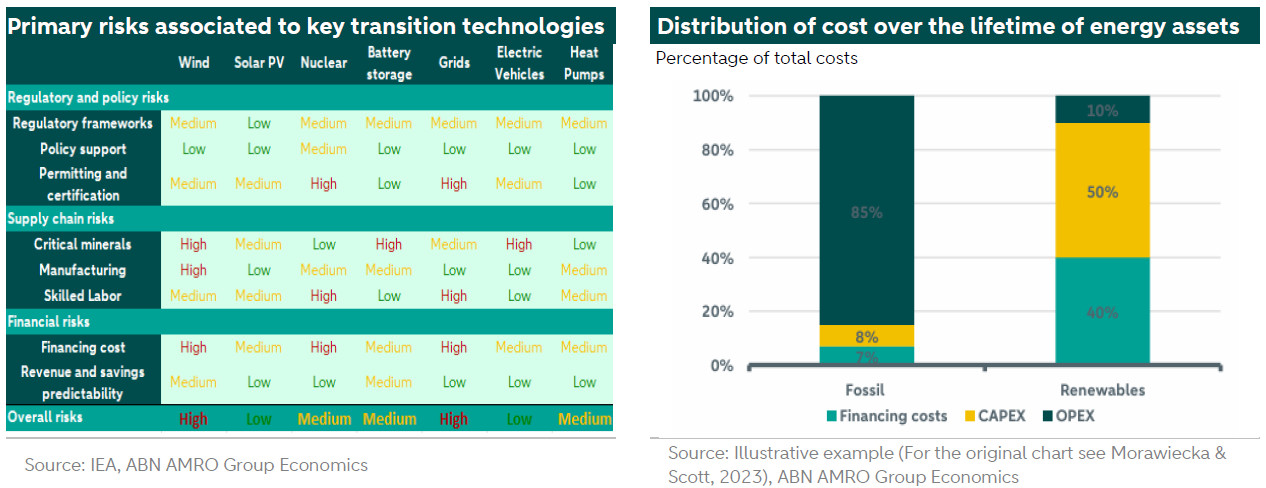

In order to assess the relationship between international trade and the energy transition, we need to identify the different channels by which trade policies affect the transition process. A successful energy transition depends on the timely rollout of transition technologies in order to achieve capacity and emission targets across sectors. Investing in transition technologies is affected by different factors, such as regulation, infrastructure readiness, financing and technology costs, as well as the resilience of supply chains. Accordingly, trade policies would affect the transition through their impact on investment costs (both CAPEX and OPEX), infrastructure development, and global supply chains of critical metals and transition technologies.

The table above (left) illustrates primary risks associated to key transition technologies. It shows that wind, battery storage and EVs are particularly vulnerable to supply chain disruptions of critical minerals, while higher cost of financing would affect wind, nuclear and grids investments the most. Wind stands out as the most vulnerable to disruptions in international trade.

Trade wars and the energy transition

A trade war is provoked when one country decides to unilaterally increase tariffs, or trade barriers, on the imports coming from one or more trading partner, while the latters, in retaliation, raise trade barriers on their imports from the former. Countries could motivate the use of tariffs on different grounds, some of which are allowed under the WTO, such as protecting own industry from unfair competition. While others could be substantiated by national agenda such as addressing trade imbalances and protecting domestic industries, which are in violation to WTO agreements.

A trade war would trigger impacts through multiple channels. In general, and depending on the business cycle, a trade war would translate into higher inflation for the country imposing the tariffs. Additionally, there will be lower trade flows between involved countries and lower growth rates. Furthermore, raising tariffs on imports would induce changes in exchange rates affecting both sides of trade, which in turn induce implications on cost, pricing and profitability. More precisely, tariffs would reduce the flow of imports and decrease the demand for the exporting country currency, inducing a depreciation of the exporting country currency relative to that of the importing country. All in all, trade wars would result in a shift in trade patterns, mostly reducing trade flows and growth rates.

The US has a unique position in international trade as the largest global economy with a dominant position for the US dollar as a main currency for international trade settlements. The new US administration started its term with an increase in tariffs on main trading partners such as Canada, Mexico and China, while tariffs on European goods could be next on the list. As these countries have signalled that they would retaliate to different degrees, a US-triggered trade war is starting to take place.

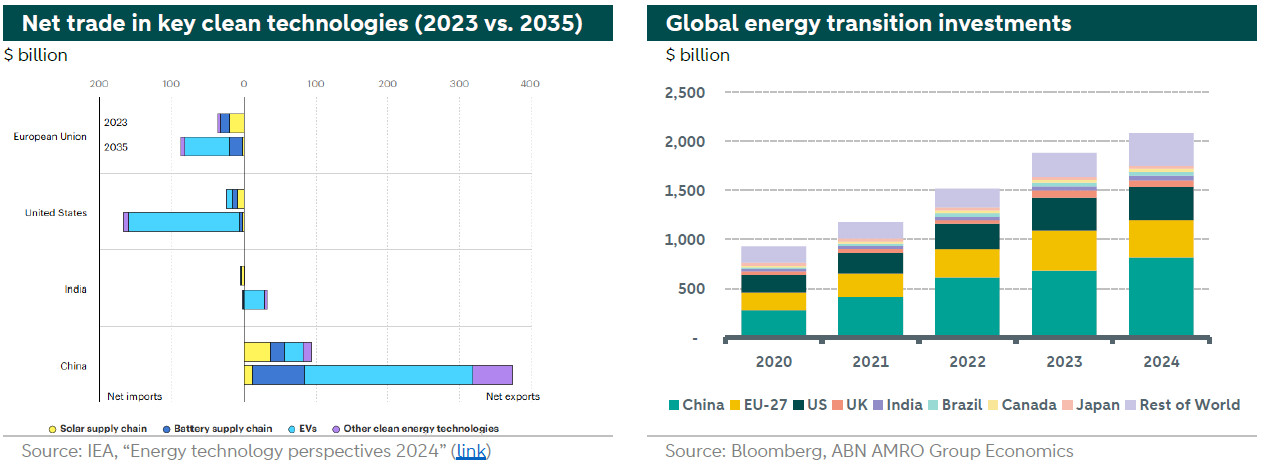

These developments are taking place at a time where international trade in clean technologies have been rising, with China leading as a net exporter for clean energy technologies, as can be seen in the graph above (left), along with arise in global energy investments (right). This raises the question of how would the European energy transition be affected by a US invoked trade war against its main trading partners? In the following sections, we highlight potential impacts on the European transition of such a war assuming trade policies between the EU and other trading partners beside the US remain as they are.

Exchange rates

China is a leading manufacturer for many transition technologies, such as EVs, batteries, solar panels and wind turbines. In addition, it has substantial reserves of critical minerals needed for these technologies, such as rare earth elements. Some of these minerals are sourced globally and processed in China. In principle, higher US tariffs on imports and a stronger US dollar would induce positive spillovers for the European transition when American tariffs affect the Chinese Yuan relatively more than the Euro, this would mean relatively cheaper transition imports from China to the EU. That is, if the US dollar strengthens against the Chinese Yuan but not as much against the Euro, it could make Chinese imports relatively cheaper for the EU compared to the US. In our base case for 2026 we expect a weakening of Chinese Yuan versus the Euro by 4,5% in comparison with 2025 (you can read more about our FX outlook here).

Technology costs

With regards to manufacturing capacity of clean technologies, there is already a global glut in the manufacturing of solar PV, electrolysers, and wind turbines, with the biggest stalled capacity in China. American tariffs (as well as the roll back of US climate policies) would reduce demand for these technologies further adding more challenges to manufacturers. The lost American demand would drive prices of these technologies to new lows, helping, in principle, to boost the European transition further. At the same time however, this would present an additional challenge for countries aiming to support and protect their domestic manufacturing capacity in these sectors. For example, the protection of the EV industry has been a strategic goal for the EU, and tariffs were already used to slow imports of Chinese EVs. Similar steps could be taken to protect Europe’s solar PV industry substantiated by anti-dumping and anti-subsidy grounds. Despite the protective tariffs, European manufacturers have struggled to compete with Chinese companies; many have had to halt operations, and some have even declared bankruptcy. Meanwhile, these tariffs are also increasing costs for developers of renewable energy projects, making their equipment more expensive.

Simply stated, reducing competition by shutting out foreign competition through tariffs in the EU would increase the cost of the transition for end users. At the same time, if the EU keeps their tariffs on Chinese imports unchanged, a US invoked trade war with China would decrease equipment prices for European developers and push the transition forward which would enhance European energy security and achieve climate outcomes.

We note that despite the higher potential EU tariffs, differences in costs could be large and Chinese goods remain competitive in European markets rendering such tariffs ineffective in protecting local industry while increasing the cost of transition for Europe. One approach that Europe needs to consider instead of protectionism through tariffs would be to attract the expertise of the world leading companies to their markets.

Finally, lower trade flows following the rise in trade barriers would entail subdued demand for international shipping, inducing even lower shipping and technology costs, especially beneficial for wind projects.

Financing costs

As mentioned above, investment in key transition technologies is quite sensitive to financing costs. In order to assess the impact of the US invoked trade war on these costs, we need to consider changes in monetary policy in response to potential changes in tariffs, growth rates, and inflation.

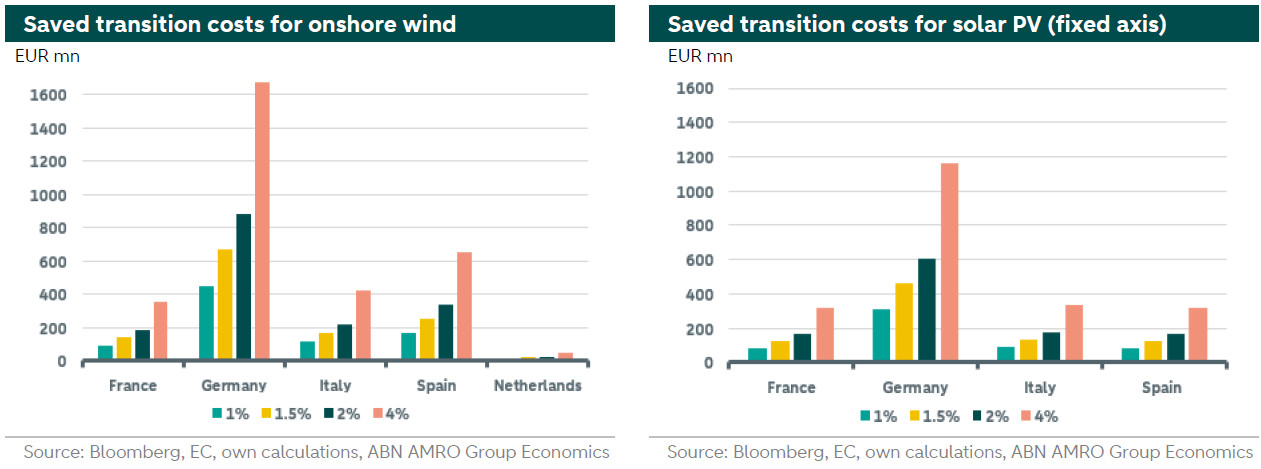

An indicator that is widely used to compared the development cost of different power technologies is the Levelized cost of Electricity (LCOE). In principle, a lower interest rate translates into lower LCOE. However, the impact differ across technologies and between countries depending on the several factors such as renewable resources and capacity factors. In an earlier study (here), we quantified the impact of lower green interest rate on the LCOE for key renewable technologies across several European countries. The charts above reflect the potential savings in transition costs associated to reaching 2030 capacity targets for onshore wind and solar PV under several scenarios of interest rates cuts.

While we judge that US tariffs would increase inflation in the US, the eurozone would likely experience lower inflation as the negative impact on domestic and global demand would offset any direct effect from EU retaliation. We set out our expectations for US tariffs in detail in our global outlook for 2025 (see more here) and in our recent global monthly (here). We expect trade to settle at a post-tariff new normal, where Chinese trade flows shift from the US to other countries including the EU. All in all, the EU would witness higher competition, lower growth rates and inflation. Accordingly, the US tariffs will likely trigger a divergence in interest rates across the Atlantic where the Fed is expected to face higher inflation and keep interest rates at restrictive levels, while the ECB would cut interest rates sharply. Lower interest rates would mean lower financing costs for energy transition investments which delivers a boost to the European transition.

Fossil fuels, critical metals and supply chains

The impact of the trade war on the prices of fossil fuels has an effect on the transition process and transition investments as well. As mentioned earlier, a US-invoked trade war would induce lower trade flows and growth rates, especially in China, demand for different fossil fuels would be lower putting a downward pressure on fossil fuel prices(3). In addition, the new US administration is backing down on its climate ambitions while supporting the development of new oil and gas projects. This would entail a future increase in fossil fuel supply and further lower prices. Lower fossil fuel prices would increase the opportunity cost of climate investments, prolong the use of fossil fuels, and induce a slowdown in the transition process.

Furthermore, tariffs and other trade barriers have been used on critical metals and minerals needed for the transition under different contexts by different countries, all of which have an effect on the transition one way or another. For example, the US tariffs on steel and aluminium have been rising in recent years. Those metals are used in transition technologies such as wind turbines, battery storage and EVs. Additionally, export controls on critical metals, such graphite and nickel, deemed essential for the manufacturing of clean technologies, have been used by China and other countries in order to retain their relative advantage in these technologies. All in all, higher US tariffs on Chinese steel, aluminium, or other critical metals would increase prices of clean technologies in the US while inducing a price decrease for these technologies outside the US which would have a positive impact on the transition in the EU.

We note that the highlighted expected effects mentioned above depends on other aspects that need to be considered as well. For example, a rise in trade barriers will induce a reshuffle in supply chains for energy and clean technologies which will induce changes in the industrial mix for different countries depending on differentials in the comparative advantage of these countries. In addition, the final effect of the trade war across countries will depend on the business cycle, emerging bottlenecks, the development of supporting infrastructure, and any changes in climate ambitions, targets, commitments, or regulation.

Conclusion

The link between international trade and the energy transition is anchored in facilitating the flow of clean technologies between countries. Different forms of trade barriers would reshuffle trade flows and supply chains of key transition technologies. Furthermore, it would induce effects on exchange rates and growth rates along with prices, inflation, and monetary policy. All of which will affect cost structures and investments in clean technologies. In a scenario of a trade war invoked by the US on Chinese goods, the transition within the EU will most likely benefit from lower technology and financing costs, while European manufacturing for clean technologies will face higher competition from Chinese products. The final effect of the US invoked trade war across countries will depend on the business cycle, emerging bottlenecks, the development of supporting infrastructure, and any changes in climate ambitions, targets, commitments, or regulation. The balance between protectionism and open trade will be crucial in shaping Europe's energy future.