Gas Market Monitor - The interplay of geopolitical risks, weather, and market dynamics

European TTF prices witness a surge fuelled by the end of the transit agreement through Ukraine, adverse weather conditions, and escalation of geopolitical risks. Storage withdrawal rate has been high with low LNG imports and the halt of Russian flow through Ukraine inducing uncertainty and strong volatility. The bullish sentiment is still dominating the market following concerns of a timely summer refill. Geopolitics remain the main driver for volatility especially with intended measures by the new US administration affecting trade flows and growth. In addition, prices will be highly responsive to any developments concerning the Ukrainian war. The market remains responsive to factors affecting demand in Europe or key LNG competitors in Asia such as adverse weather conditions, along with supply disruptions from key suppliers such Norway or the US. We expect prices to remain elevated in Q1 of 2025. Subsequently, we foresee prices to cool off a bit during the summer period, but remain above seasonal averages, before heading to 40 EUR/MWh by the end of year.

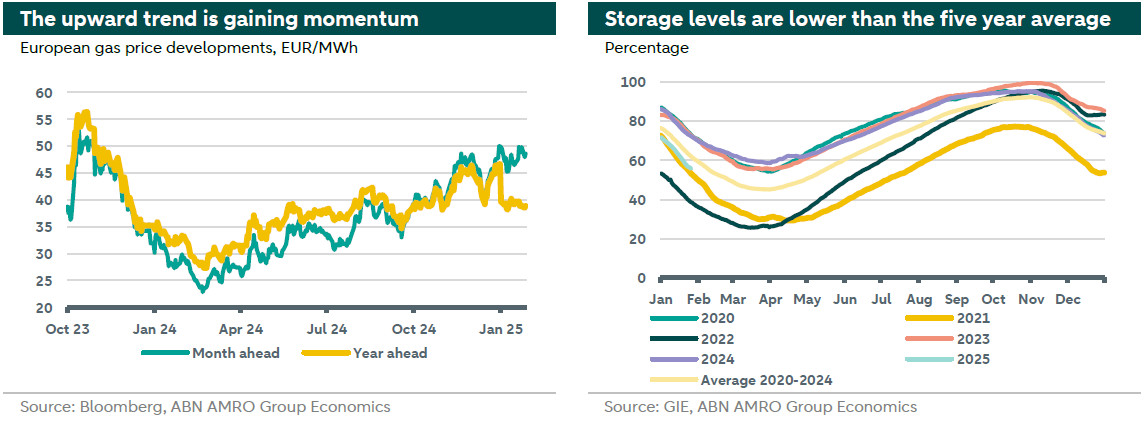

The upward trend in European gas prices continues with the month-ahead benchmark surpassing 50 €/MWh for the first time in 14 months. Since the start of 2025, the TTF averaged 48.2 €/MWh for the benchmark month-ahead contract (39.5 €/MWh for the year-ahead contract). The increase in prices was fueled by a combination of factors: a cold spell hitting Europe, which coincided with lower renewable generation, the end of Ukrainian gas transit agreement with Russia, the new US sanctions on Russian oil and gas, and geopolitical tensions, especially the escalations in the Ukrainian war. As a result, the rate of storage withdrawals has been high, which raised the risks of the timely refill before following winter, driving prices further up. European industrial demand continues to be weak, while LNG markets remain tight and volatility is here to stay. European TTF month-ahead contract is trading around 52 €/MWh at the time of writing.

European gas market developments

Several developments drove the recent surge in TTF prices. First, the end of the transit agreement between Russia and Ukraine and the failure to find a solution to keep pipeline Russian gas flowing to Europe. Even though these flows represent a fraction of the total European imports (5% by end of 2024), the absence of these flow meant higher withdrawal rates from strategic storage and more reliance on already tight LNG markets. In addition, the new US sanctions targeting Russian oil and gas have also contributed to the rally in prices. The withdrawal rate was also catalysed by cold spells seen in January combined with slower wind blow, which increased gas demand for heating and electricity production. Current storage levels (55%) are way below their five-year average (62%) and that of the same time last year (72%, see right hand chart on the previous page).

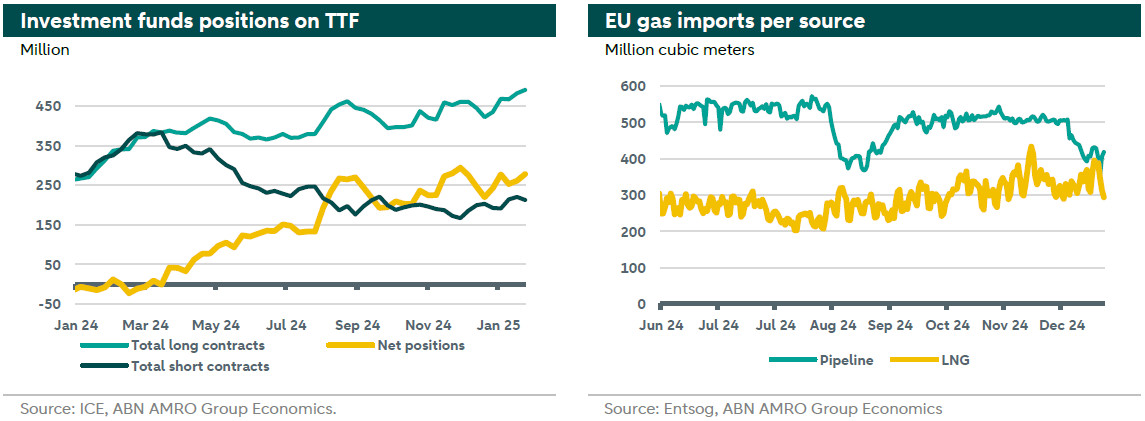

Accordingly, the coming summer refilling season poses challenges as more LNG is now required to compensate the fast depleted storage and the halted Russian gas flow via Ukraine. High storage withdrawal and potential elevated summer prices increase the uncertainty about a timely refill of storage that meets regulatory requirements (90% by November 1st). Adding to the upward pressure on prices is the German subsidy proposal that aim to refill the storage in a timely manner even with the presence of high prices, which underscores the continued fragility of supply. This has pushed summer prices further up, inverting the summer-winter spread (summer prices becoming higher than those of next winter). These developments explain the domination of bullish sentiments across market participants as illustrated by the net long position of investments funds in the chart below (left).

The halt of Russian gas flow through Ukraine has been widely compensated by storage withdrawals rather than more LNG. This could be due to recent increases in its price, which make refilling in the summer more attractive to storage administrators, knowing that the current storage was largely bought at high prices during the energy crisis. Furthermore, LNG imports to Europe have been low due to lower supply and unforeseen delays. For example, several LNG shipments from the US were delayed following the halt of production by storms hitting exporting terminals. LNG will be a major source of supply for Europe in the coming months, which means that prices should remain high to attract more LNG cargos. Higher exposure to LNG markets means more vulnerability to market disruptions and higher volatility.

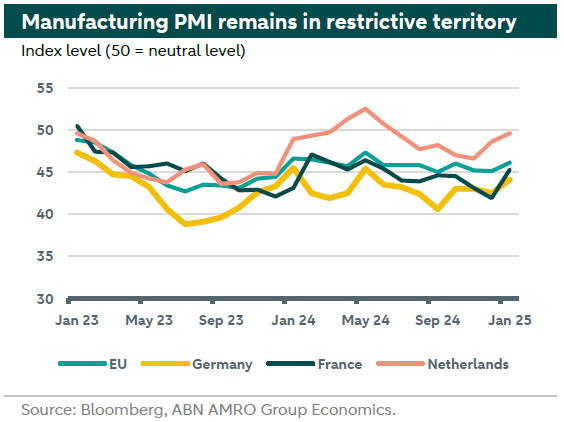

From the demand side, the recovery in European industrial demand still lacks a momentum. The Eurozone composite PMI for January edged up, now just above neutral in expansionary territory at 50.2 (49.6 in December). The eurozone economy is still being held up by expanding activity in the services sector. While manufacturing remains very weak 46.1 (45.1 in December), the pace of contraction eased in main economies, most notably in the industrial heavyweight Germany, as can be seen in the chart on the next page. Current output and new (export) orders contributed to this slight improvement in the manufacturing PMI. At the same time, the expected tariffs under the new US administration will have an adverse impact on growth, leading to a divergence in monetary policy rates across the Atlantic in 2025 (see our global outlook for 2025 ). This is expected to slow down the recovery in industrial demand in the second half of 2025.

In addition, demand for heating purposes is expected to remain high throughout the rest of winter, as weather forecasters predict this winter to be colder than the 10 year average. Hence, weather conditions in the remaining winter months are key in determining the storage levels by the end of the season. According to BloombergNEF, with extreme cold, Europe ends the heating season with its inventories 15% full, while with mild weather conditions, inventories end up 30% full.

The geopolitical premium on TTF prices remains following the latest escalation in the Ukrainian war, the risk of wider conflict, a potential lower US support to Ukraine under the new administration, and the potential US tariffs against wide range of countries threatening trade flows and growth rates. At the same time, there are some prospects for peace talks to take place soon following peace developments in the Middle East. If the Ukrainian war comes to an end, that will most likely include a (partial) lift/mitigation of sanctions on Russia, which will translate into less tightness and some relief to the European gas market. More precisely, the door will be open for a new transit agreement of Russian gas flowing through Ukraine, and, with some optimism, could also mean a Russian gas reflow through some halted pipeline such as Nord Stream. In such a scenario, we foresee TTF prices to decrease by at least 25% with lower volatility and less relevance of a storage timely refill.

Outlook

In the upcoming months, the tightness in the market remains. Geopolitics continue to be the main driver for volatility especially with intended measures by the new US administration affecting trade flows and growth. In addition, prices will be highly responsive to developments related to the Ukrainian war in the coming months. Furthermore, the market remains responsive to factors affecting demand in Europe or key LNG competitors in Asia, such as adverse weather conditions, along with any supply disruptions from key suppliers such Norway or the US.

As long as the current geopolitical atmosphere persists and the Ukrainian war continues, we expect prices to stay at elevated levels during the rest of the heating season, though we argue that current month-ahead levels being inflated by speculation. Accordingly, our outlook for TTF year-ahead price is to average around 40 €/MWh in Q1 of 2025 (47€/MWh for the month-ahead contract). Subsequently, we foresee prices to cool off a bit during the summer period, but to remain above seasonal averages, before heading back to 40 EUR/MWh by the end of year. Our outlook for EU TTF year-ahead benchmark is summarized in the table below.