Carbon Market Strategist - EUA prices rise, thanks to gas drama

EUA prices maintained their upward trend driven by the jump in gas prices, which boosted the profitability of coal power generation. European industrial demand shows early signs of a recovery, while emissions from the power sector continued to decrease for the fourth year in a row. Bullish sentiment dominates driven by the rising uncertainty in European gas markets and geopolitical ambiguity of the US trade policies. We revisit our outlook for Q1 upwards to average 75 €/tCO2.

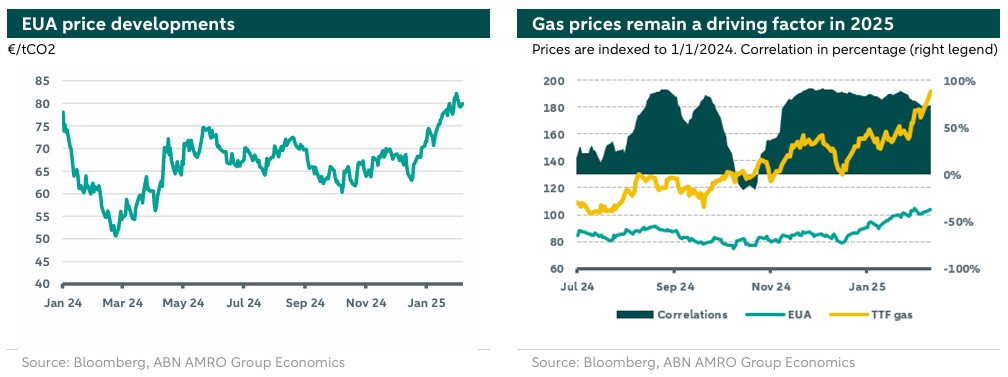

EUA prices have averaged 76.8.9 €/tCO2 since the start of 2025. EUA prices have been rising driven mainly by the surge in European gas prices. The rally in the gas market was triggered by the end of the transit agreement between Ukraine and Russia, along with adverse weather conditions in Northern Europe. Demand for industrial purposes shows early signs of recovery but a momentum is yet to come, while emissions from the power sector continued to decrease for the fourth year in a row. Bullish sentiment is dictating the market as uncertainty dominates the gas market and geopolitical ambiguity surround the coming US tariffs. EUAs were trading at around 83 €/tCO2, at the time of writing.

EUA market developments

EUA prices were subdued in the first half of December before the rally in gas prices triggered an ongoing upward trend. The correlation between carbon and gas prices remain very strong, as can be seen in the right hand chart below. The correlation stems from the role that gas plays in power markets, where gas is the main marginal fuel determining power prices, and its price further determines whether coal power plants are dispatched or not.

More precisely, gas markets have been witnessing high uncertainty after the end of the transit agreement between Russia and Ukraine on 31 of December. Gas prices started to move higher as hopes for an extension to the agreement faded away. Additionally, cold weather and slow wind induced higher demand for heating and power purposes, which in turn increased the withdrawal rate from the strategic storage. Accordingly, storage levels are now well below their seasonal averages (51% versus 58%), which sparked worries about the timely refill of storage before next winter. An increase in gas prices boosted the profitability of coal power generation and induced a higher demand for EUAs. You can read more on the developments in the European gas markets

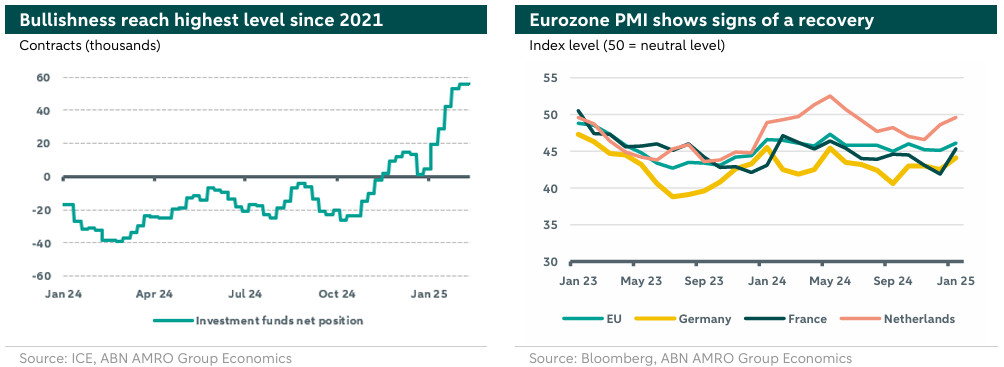

European industrial demand showed early signs of a recovery. The Eurozone composite PMI for January edged up, now just above neutral in expansionary territory at 50.2 (49.6 in December). However, the eurozone economy is still being held up by expanding activity in the services sector. Crucially for carbon prices, manufacturing remains very weak 46.1 (45.1 in December), though the pace of contraction eased in main economies, most notably in the industrial heavyweight Germany, as can be seen in the chart below (right). Current output and new (export) orders contributed to this slight improvement in the manufacturing PMI. At the same time, the expected tariffs under the new US administration are expected to have adverse impacts on trade flows and growth . This is expected to slow down the recovery in industrial demand in the second half of 2025.

Emissions from the power sector maintained their downward trend in 2025, with January power emissions hitting their lowest level ever. At 17.3 MtCO2, emissions were 14% lower than the same month of last year. The constant decrease in emissions from this sector is due to the continuous rise of renewables share in the power mix with more investments taking place in solar and wind power every year.

Market sentiment on the outlook for EUA prices is becoming increasingly bullish, as illustrated in the chart above (left) where net positions by investment funds reached their highest level since 2021. This sentiment is mainly driven by the rising uncertainty in the European gas market as explained above along with the geopolitical ambiguity surrounding US trade policies.

From the supply side, there are some reforms expected to affect the market in the coming months. These relate to the final number of allowances for REPowerEU packages and the timing of the additional free allowances for sustainable aviation fuels. Additionally, there are calls for linking the UK and EU carbon markets, citing fears of adverse impacts of the foreseen border carbon adjustment on UK exporters. Such a linkage would also increase liquidity and deliver an efficient decarbonization process, but it would also mean higher carbon costs for the UK in the short term.

Outlook

As the uncertainty in gas prices remains, carbon prices will stay elevated especially during the remaining months of the heating season (February and March). However, we think that the current levels are largely driven by speculation by market participants in the gas market rather than fundamentals in carbon market. Furthermore, geopolitical uncertainty regarding the extent and level of the new US tariffs raises ambiguity on the economic and industrial recovery in the EU. Accordingly, gas and carbon prices will be very responsive to geopolitical and weather developments in the coming months. These could play out on the upside or the downside fronts. For example, a peace deal ending the war in Ukraine would deliver a relieve to the gas market and induce an abrupt decrease in prices. Accordingly, we revisit our outlook for EUA benchmark contract for Q1 of 2025 upwards where we expect the price to average 75 €/tCO2 (was 65 €/tCO2).

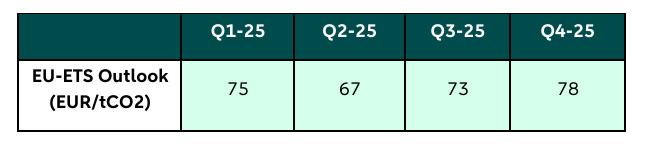

The table below summarizes our EUA price outlook for 2025. You can find the logic of our 2025 outlook in our .