Carbon Market Strategist - Market bullishness is back

EUA prices have been trending upward following the rally in gas prices which boosted the profitability of coal power generation. Allowances demand for industrial purposes remains low on the back of weak recovery . The bullish sentiment is back to dominate the market for the first time in 16 months driven by the rising uncertainty in European gas markets . The EUA market may still witness a temporary surge in demand around the year end following the yearly break in primary markets. Our outlook for December and January is slightly bullish, where we expect the EUA price to range between 68 and 73 €/tCO2. In 2025, we expect prices to cool down at the beginning of the year before regaining momentum in the second half of 2025.

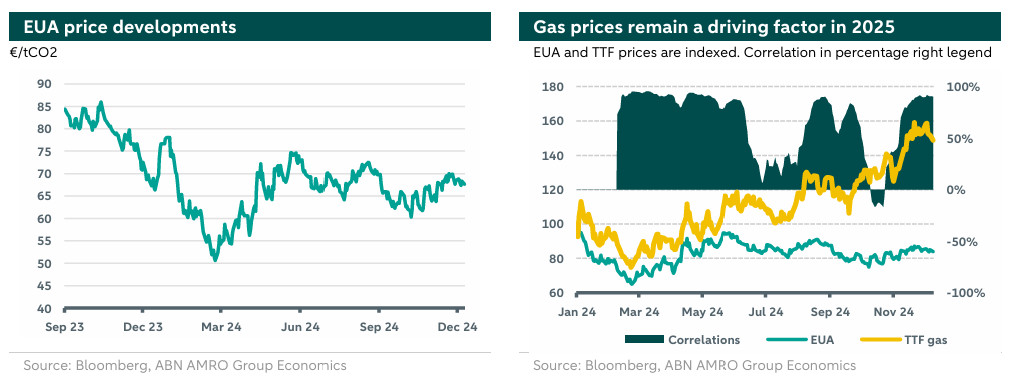

EUA prices averaged 65.9 €/tCO2 since the beginning of October. The market has been witnessing an upward trend driven by several developments in the gas market and adverse weather conditions in Northern Europe. Demand for industrial purposes remains weak following the reluctance in economic recovery. The bullish sentiment is back to the market for the first time in sixteen months driven by the uncertainty that dominates the gas market. EUAs are trading around 67.3 €/tCO2 at the time of writing.

EUA market developments

After a short lived period of decoupling from gas prices in October, the correlation between the gas and EUA markets reached its highest levels since the start of November (above 90%), as can be seen in the right hand chart below. The correlation stems from the role that gas plays in power markets, where gas is the main marginal fuel determining power prices, and its price further determines whether coal power plants are dispatched or not. Gas prices witnessed a rally that was driven by fears of supply disruptions from main suppliers following the renewed escalations in the Ukrainian war, the unpredicted halt of Russian supplies to Austria, and the uncertainty of the continuation of the transit agreement through Ukraine. An increase in gas prices boosted the profitability of coal power generation and induced a higher demand for EUAs. You can read more on the development and our outlook for European gas markets in our note here.

Weather conditions have also played a role in the rally in the gas and carbon market. More specifically, the slower wind in November induced lower renewable output and higher dependency on gas and coal power generation. This in turn translated in higher demand for EUAs. Additionally, temperatures in Europe have been towards the low end boosting the gas demand for heating purposes and supporting EUA prices.From the supply side, the primary EUA market is scheduled to be in a yearly break for a month starting from Mid-December. During this period, no auctions will take place. We note that the market has been experiencing a surplus this year driven mainly by the front-loading of allowances to fund the REPowerEU packages and the additional allowances put in the market following the extension of EU-ETS to the shipping sector.

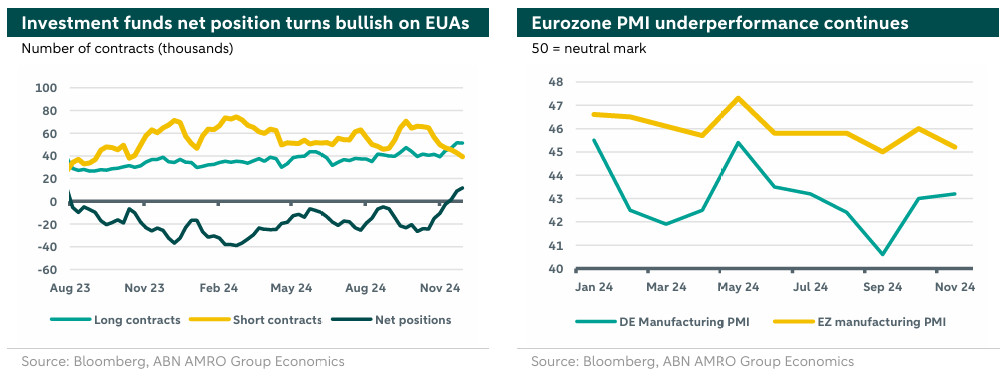

Demand for industrial purposes remains weak as the recovery in European industrial recovery still lacks a momentum. The eurozone composite PMI for November slipped into contractionary territory at 48.1 (50 in October), indicating a decrease in business activity in the eurozone halfway through Q4. Manufacturing PMI for Eurozone decreased slightly towards 45.2 (was 46 in October), while that of Germany witnessed a slight increase towards 43.2 (was 43), reflecting the challenges facing the biggest European economy, as illustrated in the right hand chart below. That being said, also the French PMI is at low levels (43).

In a prominent development, market sentiments on the outlook for EUA prices turned bullish as illustrated in the left hand chart below where net positions by investment funds became positive for the first time in 16 months. This shift in market sentiments is widely driven by the rising uncertainty in the European gas market for the coming months.

Outlook

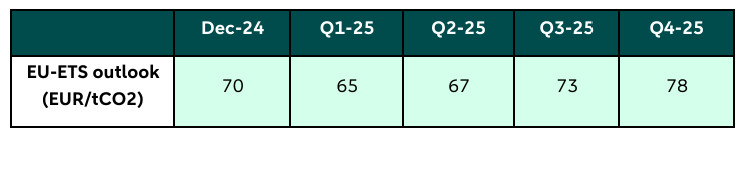

As the uncertainty in gas prices increases, carbon prices will remain responsive to geopolitical developments and weather conditions affecting the gas market. Accordingly, our outlook for EUA benchmark contract is slightly bullish in in December and early January where we expect the price to range between 68 and 73 €/tCO2. In 2025, we expect prices to cool down in February and March as the uncertainty in the gas market clears out. In addition, we expect the recovery in EUAs demand from the manufacturing sector to gain momentum in the first half of 2025 before slowing down in the second half of 2025. This momentum loss follows the expected tariffs under the new US administration which will induce net adverse impact on growth and a divergence in monetary policy rates across the Atlantic in 2025 (). That is, EUA demand for industrial purposes is expected to be modest in second half of 2025. Accordingly, demand for EUAs in 2025 will be mainly driven by the power and shipping sectors especially around the surrender date (30th of September) in the third quarter of 2025. On that note, EUA demand from the power sector is expected to be lower than the yearly average following the continuous decrease in emissions from this sector as the share of renewables in the power mix keep increasing with more investments. However, EUA prices will remain responsive to developments in gas markets and weather conditions given the insufficient storage capacity for electricity (storage capacity helps in smoothing out the intermittency in renewable output). We note that the shipping sector will surrender allowances for the first time for its 2024 emissions, which will also have an upward pressure on prices.

All in all, in 2025, we expect prices to cool down at the beginning of the year before regaining momentum in the second half of 2025. The table below summarizes our EUA price outlook for 2025.