US - The reports of a contraction are somewhat exaggerated

Import frontloading depresses 2025Q1 GDP nowcasts, while private domestic demand remains solid. This increases the probability of a technical recession, especially if further tariffs arrive later in Q2. Recession probabilities marginally elevated with current policy, with upside risks if tariffs are increased.

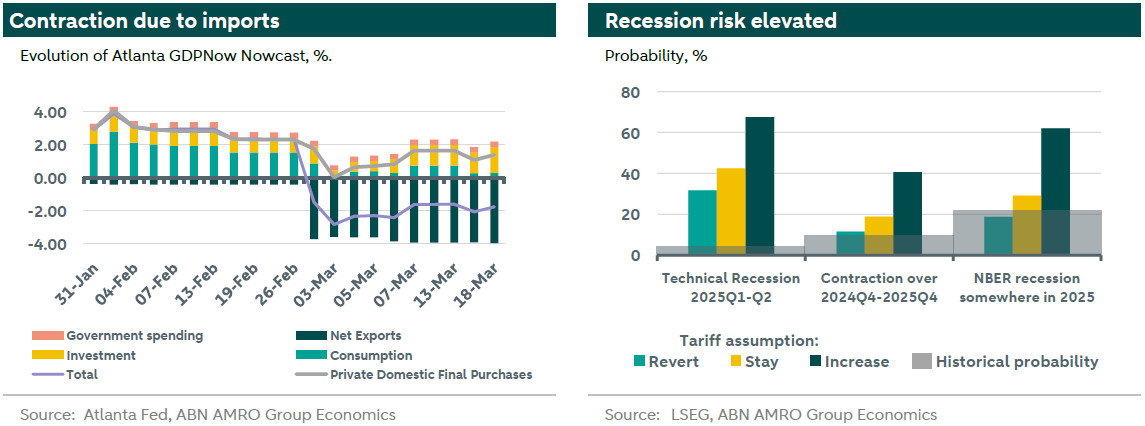

The sentiment on the US economy has abruptly changed as it’s becoming increasingly clear that the Trump administration is serious about tariffs. There is little disagreement amongst economists that the tariffs will present a negative growth shock. Even proponents of tariffs acknowledge there may be some pain in the short run, with Trump explicitly saying a recession cannot be ruled out. Tariffs are hitting an economy that was already a bit weaker than headline figures suggested. Our global outlook highlighted increasing signs of weakness, with consumption increasingly concentrated on essentials such as food, housing and healthcare, supported by borrowing, buttressed by increasing credit card delinquencies. Tariffs, effectively a regressive tax, will likely add to these cracks. Add to that a significant decrease in consumer sentiment, increasing inflation and unemployment expectations, and the result is likely weaker consumption. Another driver of GDP growth, population growth, is also likely to decline as immigration is curtailed. The policy uncertainty stemming from the Trump administration, will certainly also not help with investment. This is all reflected in the Atlanta Fed’s GDPNow tracker. The headline-grabbing negative nowcast for 2025Q1 GDP growth however comes from net exports, for a large part attributable to frontloading in anticipation of tariffs. It is clear that another year of exceptional growth is unlikely, but will the US fall into a recession?

There’s no cast-iron definition of a recession, but you know one when you see one. We evaluate the likelihood of three different definitions: i) a technical recession of two consecutive quarters of negative growth, ii) a contraction over 2025, i.e. that real GDP at 2025Q4 is lower than 2024Q4, iii) an NBER-defined recession will start somewhere in 2025 (although it may be backdated). Since 1960, the probability of these events occurring is about 4, 9 and 22% respectively. We evaluate their likelihood under three scenarios around tariffs. At the time of writing, Trump added 20% tariffs to China, 25% tariffs on Mexico and Canada (10% on energy imports), partly delayed until April, and 25% tariffs on steel and aluminium. In the ‘Stay’ scenario tariffs remain at this level, which puts the trade-weighted average tariff slightly above 9%, and close to 12% after the partial delay of Canada/Mexico tariffs passes. In the ‘Revert’ scenario, these tariffs revert to 2024Q4 levels (around 2.5%). In the ‘Increase scenario’, all the threats are enacted, including a VAT-based reciprocal tariff, leading to a trade-weighted average tariff of almost 24%.

Despite having the lowest historic probability, the technical recession probability is currently the highest, predominantly on the back of import frontloading ahead of tariffs in these two quarters. Frontloading is on track to deliver a negative GDP reading in Q1, and further tariffs in Q2 may extend that impulse. The probability of a contraction over the year is marginally elevated, and only substantially elevated if tariffs increase further. The probability of an NBER recession, which provides a broader view of the economy than just growth, is slightly higher, but also not substantially higher than the historical probabilities suggest in the revert or stay scenarios. Of course, the presence of a recession says nothing about the depth, but the overall picture of the three definitions above paints a consistent picture. The US economy can withstand the tariffs that are currently implemented, with growth merely moving to below trend, but not into a recession. Increasing tariffs to the levels that Trump has suggested to be their ultimate goal may very well be enough to push it past the breaking point. It is also important to realize that the tariff impact will last well beyond 2025, and this trade distortion may set the economy on a permanently lower trajectory, or at least until tariffs are unwound. Overall, recession probabilities very much depend on tariff policy. Given the strong economy it inherited, the Trump administration effectively has a near-term recession in its own hands. April 2nd, the ‘Liberation day’ when the tariff plan will be unveiled, will provide a clear signal on which direction the US economy is headed.