Macro Watch - What is the macro impact of all this uncertainty?

Uncertainty negatively impacts the macroeconomy, even without any actual policy changes. Households consume less and firms invest less, putting a further drag on future growth. The US is expected to face the biggest impact on economic activity, with the partial relocation of investment to the eurozone dampening the negative effects for the single-currency area.

The world faces historical levels of uncertainty. Traditional alliances, both political and economic, are upended. Some policymakers cause these rapid changes and ensuing uncertainty, while others have to react, which further increases uncertainty as the playbook is yet to be written. The mere risk of severe policy changes reflected by this uncertainty is enough to have an impact on the economy, even in the absence of any actual policy changes. We’ve discussed this before in the period leading up to the US elections. Uncertainty can lead to delayed or cancelled investment decisions by firms. They will also tend to be more cautious in hiring practices and employment expansion. Higher financial market volatility raises risk premia, with higher cost of capital again affecting the real economy through less investment. Households tend to increase their precautionary savings, decreasing consumption.

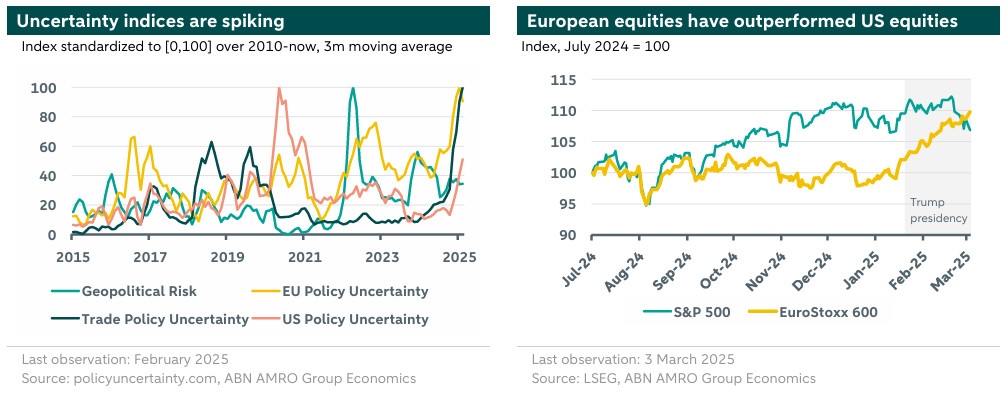

The academic literature has produced a variety of uncertainty indices on the basis of text analysis. In this piece we consider four of these indices, which best reflect the current environment[1]. The chart below normalizes these indices such that 0 is its lowest, and 100 is its highest value since 2010. The values represent no absolute amount of risk and are not comparable across the indices, merely within.

Unsurprisingly, trade policy uncertainty shows the most remarkable increase since Trump was elected, reaching levels more than one-and-a-half times the maximum uncertainty during his first presidency, which reflects the various tariffs that have been threatened and recently implemented. US and EU policy uncertainty is seeing a drastic rise in uncertainty since the start of Trump’s presidency, with EU policy uncertainty effectively doubling, while US policy uncertainty even quadrupled. US policy uncertainty is still rapidly increasing. EU uncertainty is near all-time highs, on the back of elections, defense and budget issues, already elevated after Russia’s invasion of Ukraine. Geopolitical risk peaked after that invasion, and has not substantially increased, though it is marginally higher compared to the middle of last year.

With most uncertainty originating in the US, the S&P 500 index has been mostly flat since the start of the Trump presidency, with another strong pullback recently as tariffs become more concrete. At the same time, the Euro STOXX 600 has grown steadily on the back of this same changing sentiment. The relative predictability on this side of the Atlantic makes investment more attractive. Equity markets reflect expectations about future economic activity, but we’ll have to wait months before macro data reflects this uncertainty, let alone the actual policy changes. We therefore attempt to quantify the potential macro impact of this unprecedented rise in uncertainty [2].

The macro impact of uncertainty

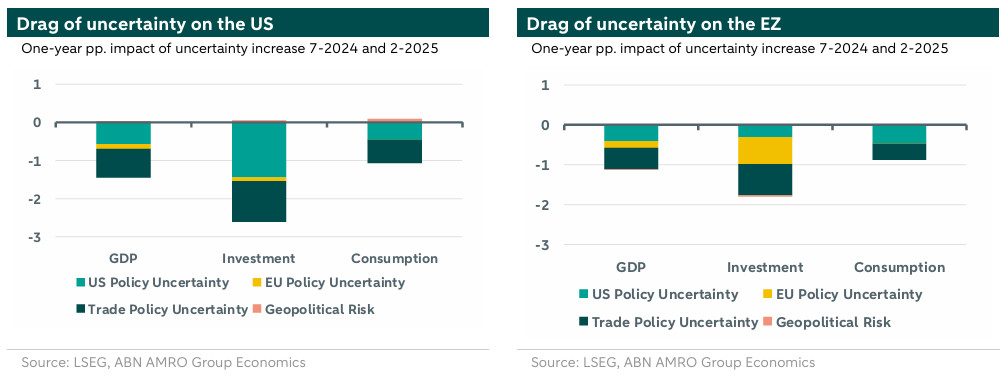

The charts below show the joint impact of the increase in uncertainty of the four indices between July 2024 and February 2025 on GDP, investment and consumption. These estimates provide the marginal impact of the change in uncertainty, without any potential offsetting factors from other developments in the economy. Moreover, given that we take the uncertainty change over a long period, some of this impact may already be reflected in Q4 figures. For instance, Q4 investment in the US already decreased by 1% (SAAR), while consumption still grew very strongly.

The relative impact on the three macroeconomic outcome variables for the US and EZ is similar: the decline in investment is the largest, with a more moderate impact on GDP and consumption. However, the investment decline has a more lasting impact on GDP and is expected to deliver a further drag beyond the one-year window. The drag on the US economy is effectively solely driven by uncertainty originating in the US: US policy uncertainty and trade policy uncertainty. Geopolitical risk has a positive effect on the US economy, but the magnitude is small (statistically insignificant) and further muted by the limited changes in risk since the second half of last year. The increase in EU policy uncertainty contributes very little.

The eurozone similarly experiences a drag from EU policy uncertainty and trade policy uncertainty, but there are far stronger spillover effects from US policy uncertainty, predominantly on GDP and consumption. The relative impact of US policy uncertainty on eurozone investment is limited due to a partially offsetting effect where a reduction in US investment is reallocated to the eurozone. EU policy uncertainty has no discernible impact on eurozone consumption, potentially reflecting governments that shield households more from abrupt policy changes, or consumers being used to crisis politics.

Overall, the US is likely to face a stronger impact of the uncertainty its government is bringing to the world. Indeed, we’ve already seen various survey-based measures, such as consumer confidence and the PMI/ISM services indices decreasing substantially over the course of the past months. This drag on investment, consumption and growth is already partially reflected in our forecasts, particularly for the US, Germany and France, which have been affected by elections and political instability. Still, resolution of uncertainty may (partially) reverse this trajectory and instead fuel investment and consumption. However, reduction of uncertainty is a trust and credibility game, something the US government is rapidly losing, and will take years to build back. Moreover, even if uncertainty is resolved, investment may still be more or less attractive depending on what policies the governments ultimately settle on.

[1] US and EU policy uncertainty indices come from Baker, Bloom and Davis (2016). Geopolitical risk comes from Caldara and Iacoviello (2021) and Trade policy uncertainty comes from Caldara, Iacoviello, Molligo, Prestipino, and Raffo (2020).

[2] The analysis is based on impulse response functions from a large quarterly Bayesian VAR that models the impact of uncertainty on macro-outcomes, controlling for a year’s worth of macro-history.