The small universe of healthcare real estate bonds

So far there are only three issuers have a clear focus on healthcare real estate and have accordingly issued social or sustainability bonds. The sector offers various structural tailwinds and the recent distress at tenant Orpea is manageable. But we do see lack of consistency in bond pricing.

The EUR IG healthcare real estate bond space is scarcely populated with only 3 issuers focussing on either being a landlord of elderly care (Cofinimmo and Aedifica) or of both clinical & elderly care (Icade Sante) properties. Each of these issuers has printed public debt under a use of proceeds banner, either as a social bond (Icade Sante) or a sustainability bond (Cofinimmo and Aedifica). One would assume that the scarcity in bond supply plus the structural tailwinds behind healthcare properties due to for example the ageing population should normally drive a strong bid towards healthcare issuers relative to issuers focusing on other property types.

The benefits offered by healthcare real estate

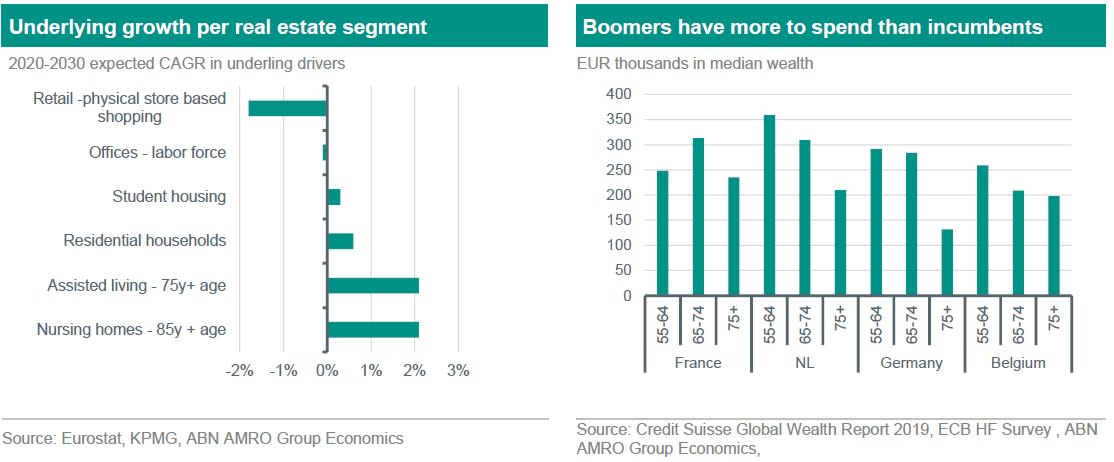

We like the various attributes offered by healthcare real estate. The triple or double net lease structures make the tenant responsible for property maintenance and/or opex. Supply of healthcare property is set to remain low in the imminent course as Europe lacks developers that can quickly ramp up supply. Finally, a recent survey conducted by broker/advisor Knight Frank revealed that more institutional investors in regular residential real estate had plans to expand their presence in elderly healthcare. Presumably due to diversification benefits, the ability to raise rents in line with inflation (which is being held back in the residential space due to rent regulation) and also long term higher rent growth potential. The left hand chart below shows the long-term growth drivers per real estate sub-class (e.g. for assisted living this would be ageing of population). Clearly elderly care stands out in terms of growth potential. The chart on the right then shows that the upcoming population of elderly care recipients (55-64 years of age) have at least the same or even a higher median wealth than the current care population. Hence, with an imbalanced supply/demand picture, the future does look bright for elderly care real estate.

Healthcare tenant troubles, but Orpea concentration is limited

The troubles at one of the big elderly healthcare operators and tenant, Orpea, could lead to investor caution towards the healthcare landlords. Next to maltreatment of residents resulting in huge reputational damage, Orpea is also facing an existential threat. Orpea had the intention to dispose real estate assets to raise funds, yet its failure to attract decent bids creates an imminent cash crunch and the company claims that liquidity could dry up as early as next month. Orpea’s failure to sell assets is also a warning that the market for large scale healthcare property transactions is pretty much dead at the moment (like other real estate assets by the way), which makes price discovery for the underlying assets at Cofinimmo and Aedifica also difficult. However, neither Cofinimmo or Aedifica have intention to dispose healthcare real estate assets and remain acquisitive in this area.

Also, both Aedifica and Cofinimmo have not yet accrued unpaid rents from Orpea and given the manageable exposure of only 5% in annual rents, we deem a potential insolvency at Orpea to be manageable for the Belgian landlords. Actually, given that Orpea holds a vast amount of real estate assets, a potential bankruptcy proceeding could be rather straightforward and the successor company could be up and running quite quickly. Looking at other large tenants such as Korian and Colisee (which represent 23% and 14% of Cofinimmo’s annual rent roll), we see mixed results in terms of rent service ability. Korian’s 2022H1 EBITDAR (=EBITDA before rents) of EUR 528mn was plentiful in comparison to EUR 245mn of rents. In the case of Colisee there are no public financials, yet the latest Moody’s report dated Aug 2022 suggests that the tenant would generate only EUR 210mn EBITDAR, which leaves limited headroom to cope with EUR 176mn rents and the risk of higher expenses such as staffing costs. Colisee only represents 7% of contractual rents at Aedifica.

Lack of consistency in bond pricing across this niche segment

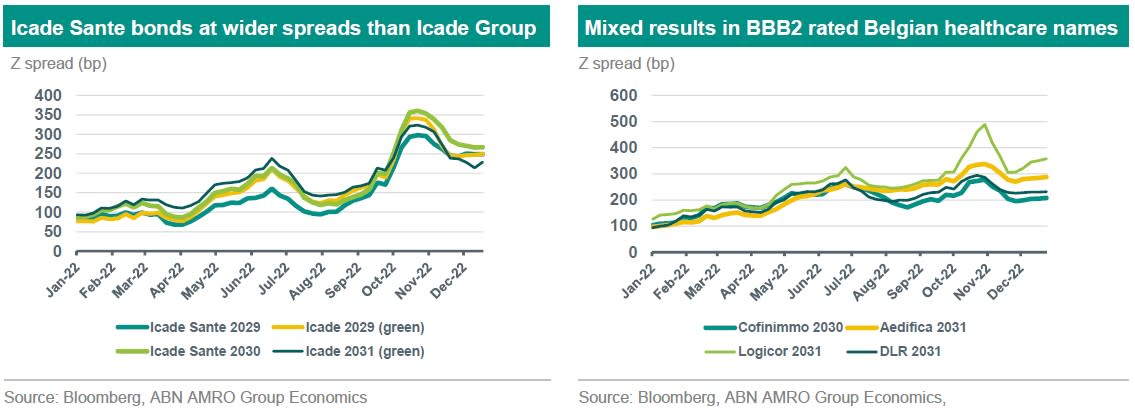

As we make ourselves comfortable with the structural tailwinds and fundamentals of this niche part of the real estate bond market, one would assume rich pricing in the underlying bonds. Looking back over 2022, the charts below show that performance of healthcare real estate issuer bonds has not been straightforward.

First, the purest of comparison you can get is between the Icade group bonds and the company’s designated healthcare real estate unit Icade Sante bonds, as shown on the left hand chart. On the 2029 maturity, the credit spread seems to be even, but the difference opens up to 38bp in favour of the group bond when comparing the Icade Sante 2030 against the Icade group 2031 bonds. At the start of 2022 the spreads on both of these bonds were equal. One could perhaps argue that the Icade group 2031 bond also has indirect exposure to healthcare real estate and it also attracts a larger crowd of investors due to it being a green bond (the Icade Sante is a social bond). However, even though both issuers have the same BBB1 composite credit rating, we note that Icade Sante actually carries less debt in relation to both EBITDA as well as total capitalization versus the parent company, which would argue for a lower credit spread on the Icade Sante bond, in both the 2029 and 2031 maturities. We would expect at least equivalence in credit spreads between the pair shown.

In contrast, the second comparison (right hand chart previous page) still shows big appreciation for Belgian healthcare real estate issuer Cofinimmo. All of the real estate issuers in this selection have a BBB2 composite credit rating and issuers Logicor and DLR also operate assets that benefit from structural tailwinds (such as logistics and datacentres). Firstly, we note that the Cofinimmo bond spreads trade relatively tight in this selection, also considering that the company has the highest leverage (13x ND/EBITDA according to S&P). Furthermore, Cofinimmo still owns a range of Brussels office real estate, which could face headwinds in rents due to the upcoming weaker economy and needs yet to crystalize work from home effects on upcoming renewal of leases. The other BBB2 rated Belgian healthcare issuer, Aedifica, seems to have a more normal appreciation by the debt market. Credit spreads on the Aedifica 2031 trade fair in comparison to similar duration bonds issued by datacentre operator DLR or logistics real estate operator Logicor, when expressed in spread per tick of issuer leverage.