Green expenditures of new 20y green DSL

The Green Bond Framework of the Dutch State has been updated and the expenditures are fully mapped against the EU Taxonomy. Moody’s assessed the new framework as very good in a Second Party Opinion. The expenditures under the Delta fund programme now fully adhere to the EU Taxonomy. There are sufficient eligible expenditures available for the allocation of the proceeds to this issuance and taps in the coming years.

The Green Bond Framework of the Dutch State has been updated and the expenditures are fully mapped against the EU Taxonomy

Moody’s assessed the new framework as very good in a Second Party Opinion

The expenditures under the Delta fund programme now fully adhere to the EU Taxonomy

There are sufficient eligible expenditures available for the allocation of the proceeds to this issuance and taps in the coming years

Introduction

On Tuesday 17 October, the DSTA will issue a new green bond, the DSL 15 January 2044 and this will be the second green bond the DSTA issues, following the issuance of the first AAA-rated green bond in 2019. In the run up to the auction, the Dutch State Treasury Agency (DSTA) updated its Green Bond Framework and it now adheres, according to the DSTA, to best market practises. In this note, we will focus on the updated framework, the assessment of the framework by Moody’s as a Second Party Opinion and the categories of eligible expenditures that will be used from the proceeds of this new green DSL.

Delta Fund expenditures now fully mapped against EU Taxonomy under new Green Bond Framework

The DSTA published its Green Bond Framework in 2019 when it issued its inaugural green bond, the DSL 2040. Since then, significant developments in the field of sustainable finance have materialised resulting in an update of the framework in 2022 and in 2023. In this update, the DSTA aligned the framework with the EU Taxonomy Climate Delegate Act on a best effort basis1) and became the first sovereign to do this.

On 8 September 2023, the DSTA published a new updated Green Bond Framework in the run up to the issuance of the new green bond, the DSL 2044. The framework is aligned with the existing EU Taxonomy as well as the upcoming EU Green Bond Standard, again on a best effort basis2). Furthermore, the new framework also aligns with the proposed EU Taxonomy criteria regarding flood risk prevention and protection, and nature-based solutions for flood and drought risk prevention and protection as published on 13 June 2023 by the European Commission. This means that, compared to the previous framework, the expenditures in the category ‘Climate Change Adaptation & Sustainable Water Management’ have been mapped against the amendments to the EU Taxonomy, which were released in June this year. As the new additions to the EU Taxonomy contain criteria for flood risk prevention and nature-based solutions for flood risk prevention, the Delta Fund expenditures are now fully mapped against the Taxonomy criteria. The Delta Fund programme has the aim to protect the Netherlands from flooding, to secure sufficient supplies of freshwater and to make the country climate-proof.

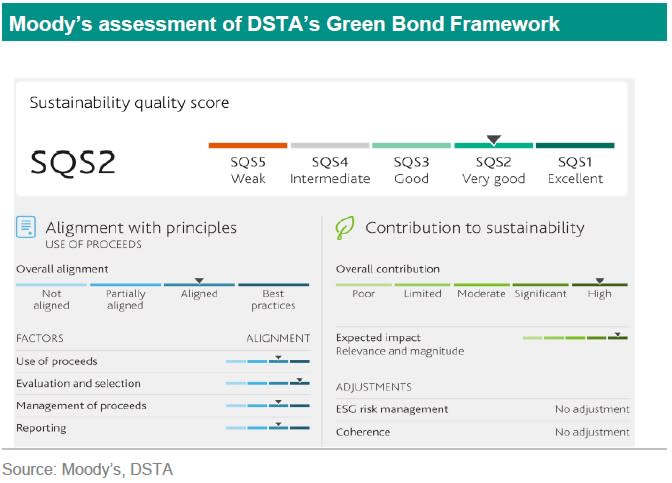

Second Party Opinion (SPO) from Moody’s

The DSTA has appointed Moody’s as a SPO for an external review of the Green Bond Framework following a tender amongst interested parties. The assessment focused in particular on whether the Framework is aligned with the ICMA Green Bond Principles (2021, with June 2022 Appendix I), adheres to the EU Taxonomy Climate Delegate Act (June 2021) and to the proposed analysis of the coherence of the framework with overall national policies and action plans (Environmental Delegated Act, June 2023)3).

Moody’s has assigned a Sustainable Quality Score of ‘Very Good’ (SQS2) to the Government of the Netherlands’ green bond framework (see graph below). As shown in the second party opinion report, the framework is aligned with the core components of the ICMA Green Bond Principles 2021 (including the June 2022 Appendix 1) and demonstrates a high overall contribution to sustainability. In addition, Moody’s considers that 11 out of 12 economic activities adhere to all the EU Taxonomy criteria relating to both substantial contribution and do-no-significant-harm (DNSH), based on information provided by the Dutch State. For the economic activity where this was not fully possible (transport by motorbikes, passenger cars and light commercial vehicles), it is considered that all criteria adhere to the EU Taxonomy, except for the pollution prevention control and DNSH criterion.

Use of proceeds

The proceeds from the green bonds issued by the Dutch State are intended to exclusively finance or refinance expenditures, which are part of the Central Government Budget or tax relief measures which are included in the Budget Memorandum (Miljoenennota) and contribute to the EU Environmental Objectives of Climate Change Mitigation and Climate Change Adaptation (‘Green Expenditures’) and Sustainable use and protection of water and marine resources (‘Blue Expenditures’).

The eligible expenditures are limited to Central Government Budget expenditures in the budget year preceding the issuance, the budget year of issuance and the two years following the issuance. The DSTA intends to allocate at least 50% of the net proceeds of the issuance to expenditures in the budget year of issuance or future budget years.

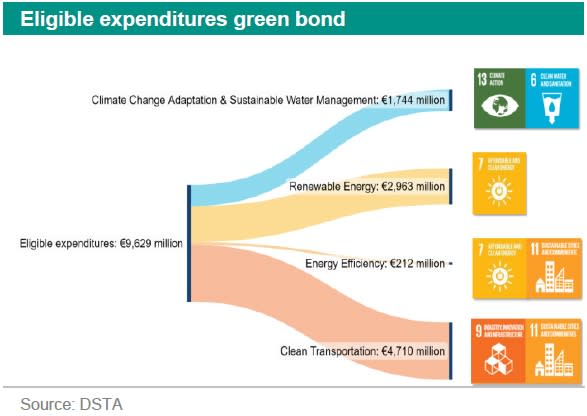

The Dutch State included four categories of eligible expenditures, which are also mapped to the Green Bond Principle categories, the relevant UN Sustainable Development Goals (SDGs) as well as Economic Activities and Environmental Objectives under the EU Taxonomy. The four categories are:

Renewable Energy

Energy Efficiency

Clean Transportation

Climate Change Adaptation & Sustainable Water Management

In total, the DSTA has identified EUR 9.6bn of expenses that meet all the eligibility criteria in the Central General Budget of 2022 and 2023, implying that sufficient expenditures can be allocated to the proceeds of the upcoming issuance of EUR 5bn of the DSL 2044. However, this amount is the sum of all the planned expenditures that have been found in the General Budget of the 2022 and 2023 and therefore represents the maximum amount that can be allocated to the proceeds of the green bond issuance on 17 October. In practice, this number will be lower and perhaps even significantly lower as some of the projects will be postponed due to tight labour market conditions, while other expenditures will not take place due to other developments. For example, the direct investment of the Dutch State of around EUR 1bn in TenneT, the Transmission System Operator for the Netherlands, could be cancelled if the sale of the German part of TenneT would take place next year. Furthermore, the actual subsidies for renewable energy generation (via the SDE subsidies) have been substantially lower in 2023 than what was budgeted due to the higher energy prices in 2023. As such, the actual eligible expenditures will be significantly lower than the total of EUR 9.6bn, but there will remain still sufficient eligible expenditures for this new issuance of the DSL 2044. Furthermore, as there will be new eligible expenditures available from the Central Government Budget in 2024 and beyond, there will be sufficient expenditures available to tap the new green DSL 2044 in the coming years.

As can be seen in the graph below, almost half of the eligible expenses (EUR 4.7bn) are in the Clean Transportation category of which the lion’s share comes from railway-related expenses, including maintenance and management of railway infrastructure (excluding freight railway infrastructure). This category also includes (re)development of railway stations and bicycle parking space at railway stations.

The second biggest part of the total eligible expenditures is the Renewable Energy category, including the SDE subsidies for generating renewable energy and the possible direct investment of the Dutch State in TenneT. New on the list is the support of the production and transportation of hydrogen.

Finally, the expenditures related to the Delta fund programme are linked to the Climate Change Adaptation and Sustainable Water Management category.