ESG bank bonds make strong start to 2023

Issuance of green, social, and sustainability bank bonds in euro rose in January by 174% compared to 2022, with covered bonds and senior non-preferred debt accounting for most of the increase. ESG bank bonds attracted larger demand than non-ESG peers, also resulting in lower new issue premia.

Issuance of green, social, and sustainability bank bonds in euro rose in January by 174% compared to 2022, with covered bonds and senior non-preferred debt accounting for most of the increase

Green bond issuance was almost four times larger than bank debt in social format, reflecting that the green bond market is more established than the social bond market

The increase also mirrors the overall flood of supply of bank debt in January, as the share of green and social bank bond issuance remained relatively stable in January versus the 2022 average for the year as a whole

ESG bank bonds attracted larger demand than non-ESG peers, also resulting in lower new issue premia

The primary market for euro bank debt has started 2023 on a very strong footing, as almost EUR 100bn of covered bonds, senior paper as well as Tier 2 debt was issued in January. This was a 78% increase compared to January 2022. In this note, we look at last month’s issuance of green, social, and sustainability bank bonds (hereby all three flavours referred to as ESG bank bonds), as well as pricing dynamics and demand for these bonds.

Issuance rising, share in total stable

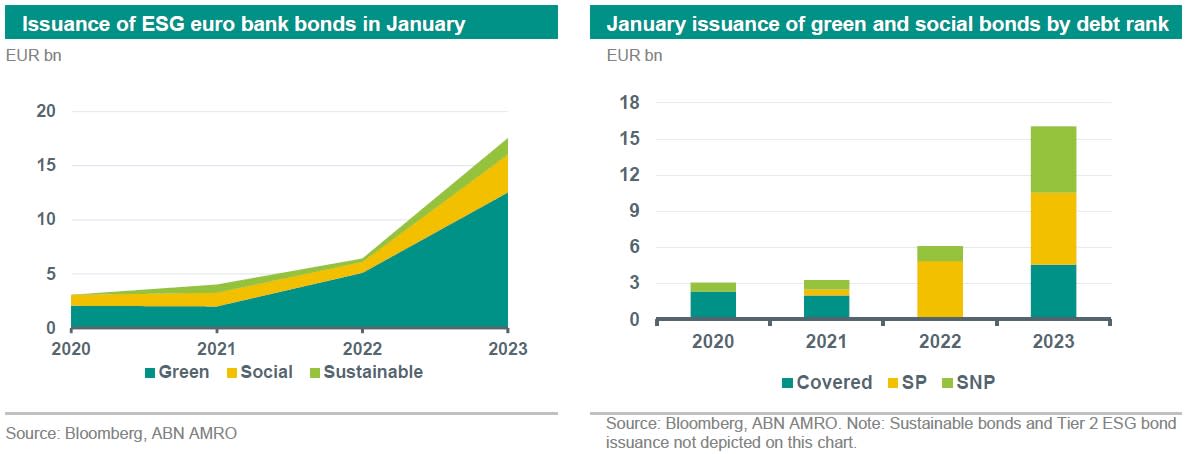

The graph on the left side above shows that issuance of green, social, and sustainability bank bonds, denominated in euro, also rose sharply in January of this year. EUR 18bn of ESG bank bonds were issued last month, which was a 174% rise compared to the volume of issuance in January 2022 (EUR 6.4bn). In volume terms, the largest increase was in issuance of green bank bonds, which increased by EUR 7.5bn, while the volume of supply of social bonds increased by EUR 2.5bn. Sustainability bonds also almost quadrupled in volume, reaching EUR 1.5bn in January 2023. Overall, issuance of ESG bank bonds is already 25% of total ESG bank bond issuance in 2022.

A breakdown by asset type and focussing on bonds in green and social format shows that covered bonds and senior non-preferred bonds (SNP) were the key reason for the strong growth in issuance of ESG bank bonds (see graph above right). However, we base this on only one month’s data, and we must bear in mind that no green/social covered bond was issued in January last year, while already eight such covered bonds were issued this year. The increase in issuance was also driven by larger supply of green and social senior non-preferred bonds, which rose to EUR 5.5bn in January this year versus EUR 1.25bn last year. Still, senior preferred debt accounts for the largest chunk of issuance in green and social format (EUR 6bn vs EUR 4.9bn in January 2022).

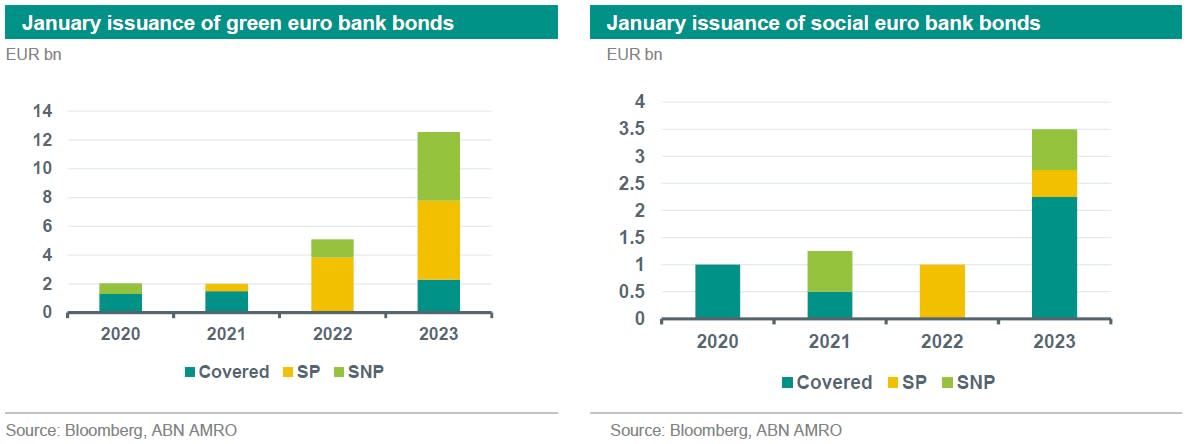

Digging a bit deeper in the data by splitting issuance of green and social bonds per bank debt rank, reveals that green bond issuance was almost four times higher than the supply of social bonds in January (see graphs below), likely reflecting that the market for green bonds has been more established than that for social bonds. This, in turn, is perhaps related to the fact that the green bond market has developed more robustly over the past few years, driven by, for example, clearer guidelines for green bonds (e.g., the EU taxonomy) than that for social bonds. Social bond issuance in 2020 and 2021 was also in general largely driven by Covid-19 related investments, which are not very common anymore. Covered bonds form the majority of social bank debt issuance, probably as they finance, among others, social/affordable housing, which fits the character of most cover pools well.

Meanwhile, supply of green senior non-preferred bank bonds got off to strong start this year, with six issuers printing EUR 4.75bn. This bodes well for the market going forward. Unlike last year, this year the green format is not being used to get deals done because of unfavourable market conditions, but they are coming to the market under favourable conditions.

Turning to the share of ESG bank bond issuance in total issuance shows that it has remained rather stable so far this year. We focus exclusively on green/social issuance (sustainability bond issuance was mainly in Tier 2 format). In the covered bond space, 10% of total euro-denominated issuance was in green/social format in January, which was 1% higher than the average for 2022 as a whole. The share of green/social senior preferred issuance dropped to 23% of the total, down from 28% on average last year. Finally, in the senior non-preferred market, green/social issuance remained stable at 24% of the total volume of new supply compared to 2022. If this remains the case for the entire year, we will see a slight reduction in social and green bank debt issuance in 2023 as a whole, despite the strong start to the year. This is because we expect, on balance, lower issuance of euro bank debt (including covered bonds) this year than in 2022.

ESG bank bonds attract strong demand, while new issue premia lower

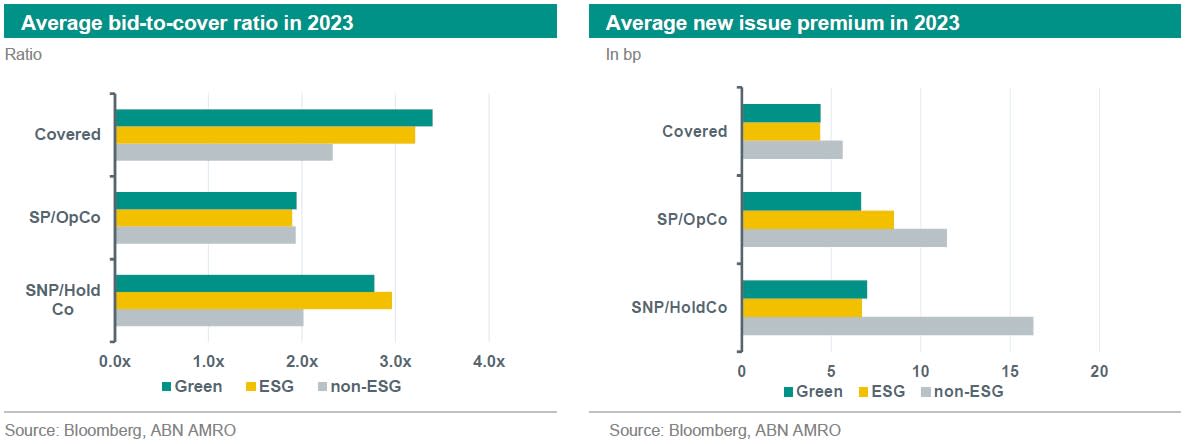

The relatively large volume of new supply of ESG bank bonds in January was well absorbed by investors, which seem to have a clear preference for green, social, or sustainability bank debt. This is reflected by higher average bid-to-cover ratios (see graph on the next page, left), which is particularly observable for covered bonds and senior non-preferred debt. Indeed, the average bid-to-cover ratio for green covered bonds was 3.4x, while this was 2.3x for non-ESG covered bonds. Of course, this could also be due to other factors, such as the tenor and/or the issuer profile, but we think it is fair to assume that the green/social element is also a material factor at play. The same also holds for senior non-preferred debt, whereas demand for green and social senior preferred bonds was roughly in line with that of non-ESG peers. This, in turn, was probably because some green senior preferred debt was issued by banks with a lower credit quality. In any case, in terms of pricing, issuers paid lower new issue premia for ESG bonds, irrespective of the debt rank. This suggests that greeniums are still very much alive in the primary market. This is especially true for senior non-preferred bank debt, where the average new issue premium for bonds in ESG format was more than half that of non-ESG peers. This could also be related to other factors, but it fits the view that the potential for a ‘greenium’ is larger for bank debt that trades at wider levels. Overall, it seems fair to conclude that the market for green, social, and sustainability bank bonds has made a positive start to 2023, which in itself bodes well for the remainder of the year.