The ECB starts disclosing the climate impact of its portfolio

The ECB has published its first climate disclosure report on its EUR 344bn corporate bond holdings purchased under the CSPP and PEPP. Emission intensity has been declining since 2018, through good luck as well as good management. In addition, it has a greater share of holdings in issuers with reduction pathways than its eligible universe.

The ECB published its first climate disclosure report on its corporate bond holdings

Emission intensity has been declining since 2018, through luck and management

It has a greater share of holdings in issuers with reduction pathways than its eligible universe

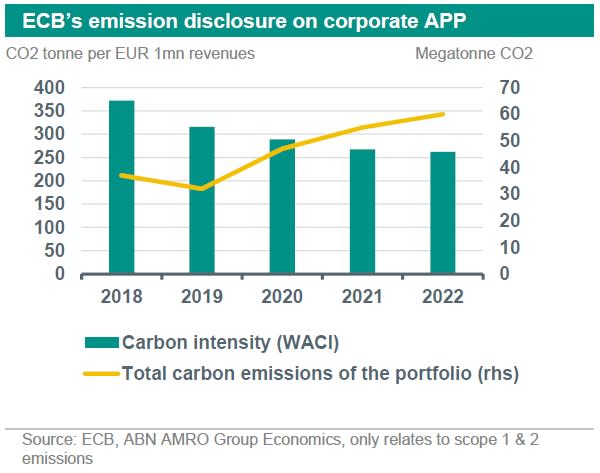

Two weeks ago the ECB reached a milestone on its large holdings of corporate bond securities worth EUR 344bn purchased under the CSPP and PEPP. For the first time it published the carbon impact of the portfolio as this was also part of its earlier climate action to improve climate disclosures to the public. Earlier the central bank had already decided to tilt the reinvestments of bond purchases, which we expect to end in the second half of the year when it comes to the CSPP, towards issuers with better climate performance based on 3 pillars being their existing emissions, their ambition to reduce emissions and the quality of their climate disclosures (see our previous notes and ).

In the disclosure, the ECB weighs the carbon intensity of each issuer (limited to scope 1 & 2 emissions divided by revenues) and then calculates a weighted average based on each issuer’s share in the corporate bond portfolio. This is also known as the WACI approach. It also has calculated a non-intensity based total portfolio emission, which relates total emissions to the size of ECB holdings divided by the issuer enterprise value. Due to significant growth in the size of holdings over the past few years this absolute measure has risen considerably. Limited historical data reliability precluded the years before 2018 in the historical comparison (remember the ECB started purchasing corporate bonds back in early 2016) and due to reporting time limitation the 2022 numbers actually reflect 2021 emission and financial data re-arranged for the latest holdings. The chart below shows the WACI and the absolute portfolio emissions.

The WACI has been on a clear downward trend from when recording started. For 2019 the ECB states that greater decarbonization efforts by issuers were the main driver behind this improvement. During 2020, the collapse in revenues at pandemic affected sectors (such as transport and utilities) would have led to higher intensity, but the ECB steered a larger share of its purchases to less carbon intensive (but also less revenue affected) sectors during this year, which kept the WACI on a descent. The reductions in intensity during 2021 and 2022 were purely because issuers were able to raise revenues fast in the pandemic recovery, since primary issuance from carbon intensive sectors was large. In the final quarter of 2022, when the ECB implemented climate change considerations in their mandate, the WACI on purchases fell considerably, but given the large stock of debt held by the ECB the portfolio impact was very limited. It seems that the decline in WACI seems to be a combination of luck and active management by the ECB.

Finally on future emission targets, which is the second pilar of the ECB’s issuer climate criteria, 59% of the holdings relate to issuers which have certified science based carbon reduction targets. This contrasts against only 42% of all eligible issuers having some form of carbon reduction targets, confirming that the ECB is taking serious steps already to green its portfolio.