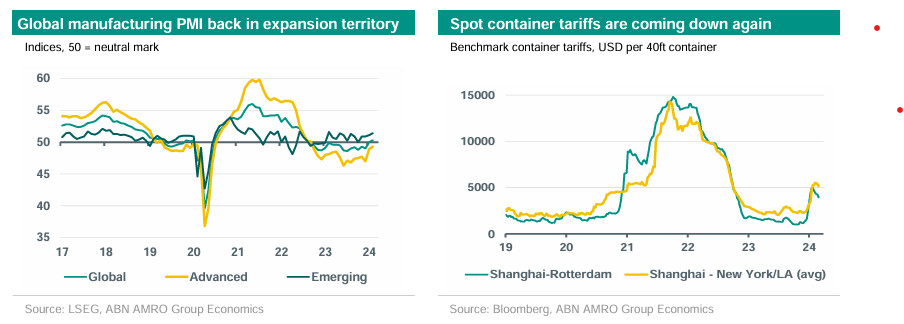

Global manufacturing PMI creeps back into expansion territory

Global manufacturing PMI rises to above neutral mark in February. This is in line with our expectation of a bottoming out in global industry this year. Impact of recent disturbances in global shipping seems to fade.

Global manufacturing PMI rises to above neutral mark in February, ...

Over the past few days, manufacturing PMIs for the month of February were published for various developed markets (DMs) and emerging markets (EMs). Following a full point rise in January to 50.0, the global manufacturing PMI rose further in February to 50.3. This marked the first reading above the neutral mark separating expansion from contraction since August 2022. The aggregate DM index improved further by 0.4 points to 49.3 (following a rise by almost two points in January), although it remained below the neutral mark. The EM aggregate index rose by 0.3 points to 51.4, remaining well above the neutral mark.

Amongst DMs, the improvement was driven by the US, with the index from S&P Global rising to 52.2 (January: 50.7). Notably, this was in contrast to the ISM manufacturing PMI in the US, which actually declined to further below the 50 mark. The manufacturing PMI for the eurozone was more or less stable in February, staying clearly below the neutral mark in February (at 46.5). However, there was a remarkable divergence between the index for Germany (which fell by three points to a four-month low of 42.5) and that of France (which rose by four full points to an eleven-month high of 47.1). The manufacturing PMI for the Netherlands rose further by 0.4 points to 49.3, after a surge of almost four points in January. Despite the improvements seen in France and the Netherlands, their respective manufacturing PMIs remained in contraction territory. Amongst EMs, Caixin’s manufacturing PMI for China (which is included in the EM aggregate) was more or less stable at 50.9, with the improvement coming mainly from other large EMs (Brazil, India, Mexico, Russia, Turkey) this time.

…in line with our expectation of a bottoming out in global industry this year

The further pick-up of the global manufacturing PMI in February is in line with our expectation of a bottoming out in global manufacturing this year, which fits to our growth views for the key economies (US, eurozone, China) – with ongoing US resilience leading us to upgrade our 2024 growth forecast (see ) and stabilisation in China on the back of more stimulus (see and ). We still deem a very sharp rebound unlikely at the moment, also taking into account the fact that alternative surveys – not included in the global aggregate – for both the US (ISM) and China (official PMI published by NBS) are still in contraction territory, while US industrial production does not appear to be very strong in monthly terms at the moment.

Impact of recent disturbances in global shipping seems to fade

Last month, we noted a significant improvement in the demand-related components of the global manufacturing PMI. In February, the global manufacturing PMI’s component for domestic orders rose further by 0.6 points to 50.4, the highest reading since May 2022 and the first reading above the neutral mark since June 2022. The export orders component also rose by 0.6 points to a twenty-month high of 49.4, although remaining in contraction territory for the time being. Regarding the supply side, the rise in the global output component was even stronger in February, by 0.9 points to a 9-month high of 51.2 (the increase mainly driven by DMs). All in all, supply conditions currently still look a bit stronger than demand conditions, which is keeping inflationary pressures in check. What is more, the impact of recent disturbances in global shipping (Red Sea and Panama Canal) on global industry seems to be ebbing somewhat. The global component for delivery times (which dropped in January, indicating somewhat longer delivery times) rose back above the neutral mark in February, the components for input and output prices have stabilised, and container freight tariffs have come down over the past few weeks following a surge in end-2023 and early-2024. All of this is also reflected in our global supply bottlenecks index, which moved back a bit further into ‘supply abundance’ territory.’