US - Stronger growth unlikely to derail Fed rate cuts

We have raised our 2024 growth forecast on the back of the more resilient labour market. Still, we expect some slowdown in growth, given evidence of rising financial stress from high rates. Despite stronger growth, we still expect inflation to fall sustainably back to 2% by mid-2024, keeping the Fed on course to begin lowering rates at the June FOMC meeting.

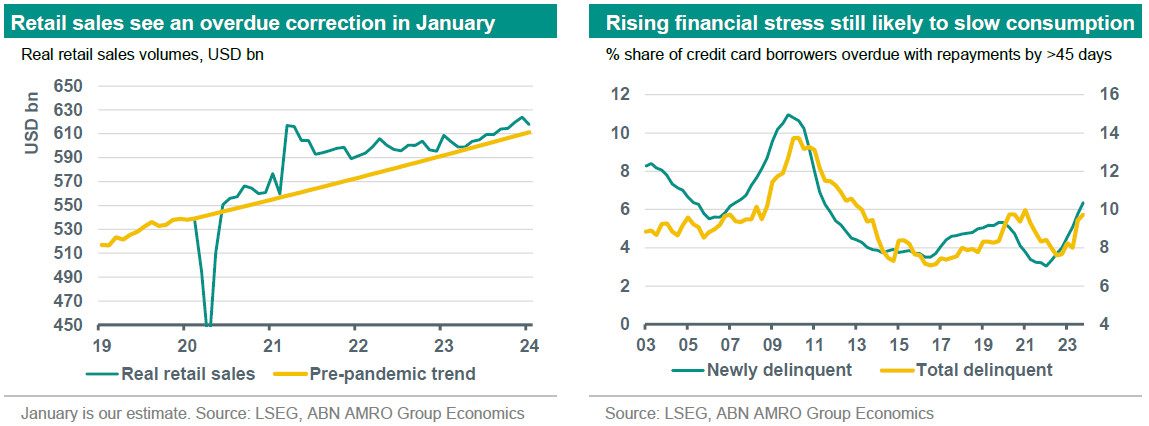

In contrast to the strong labour market data for January released earlier in the month, January activity data covering the consumption and production side of the economy came in on the weak side. Nominal retail sales fell 0.8% m/m, following a downwardly-revised 0.4% rise in December. Industrial production fell -0.1% following a downwardly revised flat reading for December, likely impacted by poor weather conditions over the period. The weakness in retail sales followed a strong run in the data over the second half of last year, and in our view represents an overdue correction given that goods consumption remains above trend in the US. As such, the decline is consistent with our expectation for a slowing in activity in 2024, rather than being a cause for concern over the outlook. Indeed, despite the weak tone to the January retail sales data, we are actually raising our 2024 growth forecast by 0.3pp to 2.1%, and for 2025 we are lowering our forecast by 0.1pp to 1.9%, reflecting the higher base of 2024. We were already above consensus in our growth forecast for 2024, at 1.8% vs 1.6%, and this change takes us further above the consensus forecast.

The update is driven by two main factors. The first is backward-looking – though the economy is slowing significantly, activity (particularly consumption) held up better than expected in the last months of 2023, and this ‘carry-over’ effect by itself lifts our 2024 forecast. The second driver of the change is the strength in the labour market. While we do not take too much signal from the blockbuster January payrolls data, given that it is based on a relatively low survey response, the significant upward revisions to employment in Q4 2023 suggest a bottoming out in the jobs slowdown. Given this, we expect only a marginal rise in unemployment (to around 4% from the current 3.7%). While higher credit card delinquencies and a reduced savings buffer still point to some consumption slowdown, the slowdown is shallower than we previously forecast.

Despite this more resilient growth picture, we still expect the Fed to start cutting rates from June. As Chair Powell stated at the January FOMC press conference, ‘we don’t look at stronger growth as a problem’. This is because much of the strength in growth has been driven by a significant improvement in the supply side, particularly the labour market. Indeed, although unemployment has held at historically low levels, this masks a major easing in labour market tightness below the surface. Specifically, the job vacancy to unemployed ratio has fallen from a peak of 2.0 in July 2022, to 1.4 as of December – only a little above the pre-pandemic level of 1.2. This has been driven by both improved labour force participation and cooling labour demand. As we describe in this month’s Global View, this has helped wage growth fall back to levels already close to what is necessary to meet the 2% inflation target sustainably. We expect PCE inflation to hit the Fed’s 2% target on a sustainable basis already by April, giving the Fed ample reason to start lowering interest rates at the June FOMC meeting.