Global manufacturing - New disruptions on the horizon

Global manufacturing PMI rose to eight-month high in February. Both DMs and EMs show gains, but Canadian and Mexican PMIs sharply down on US tariffs. Improvements at both supply and demand side; export PMIs down for US, Canada, Mexico. Price components suggest pressures from industrial goods’ prices are building again. Spot container tariffs keep falling so far. US port fee plans may lead to serious disruptions in global shipping.

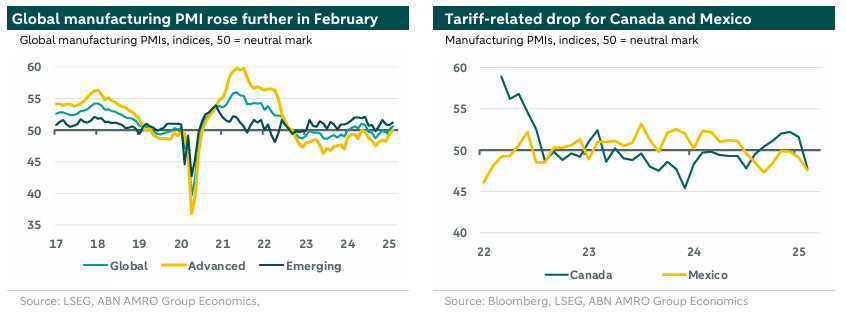

Global manufacturing PMI rose to eight-month high in February

The global manufacturing PMI moved up further in expansion territory, climbing to an eight-month high of 50.6 in February (January: 50.1). The index has now risen by almost two points since the last cyclical low in September. Still, the improvement seen in global industry is relatively modest so far compared to previous upturns – in line with our views. Our outlook for 2025 assumes headwinds from a US trade tariff shock (see for a recent update) drive a slowdown in global GDP and (goods) trade in H2-2025 and in 2026, which will likely form a drag on global industry as well. That said, the stepping up of fiscal support in Europe (see ) and China (see ) will act as an offsetting factor to this. On the short term, trade frontloading ahead of US tariffs may even support global trade and industry to some extent.

Both DMs and EMs show gains, but Canadian and Mexican PMIs sharply down on US tariffs

The further improvement in the global manufacturing PMI in February was broad-based, with aggregates for both developed markets (DMs) and emerging markets (EMs) moving up. The DM index rose by another 0.7 points to 50, the first move out of contraction territory since May 2024. S&P Global’s index for the US rose by 1.5 point to 52.7, the highest level in almost three years. That said, the alternative index for the US (ISM) went in the other direction, falling back by 0.6 points to 50.3. The rose to a two-year high of 47.6, remaining well below the neutral mark. Germany and France showed improvement but were still relatively weak, while the Dutch manufacturing PMI climbed back to an eight-month high of 50.0 (see ). The improvement in EMs was driven by , with Caixin’s manufacturing PMI at a three-month high of 50.8. Meanwhile, the manufacturing PMIs of Canada and Mexico dropped sharply (see chart), which looks related to the 25% US tariffs (although their coverage has been reduced).

Improvements at both supply and demand side; export PMIs down for US, Canada, Mexico

The improvements in the global manufacturing PMI shown in February were visible at both the supply and the demand side, with the global components for (future) output and domestic orders all rising compared to January. The global export orders sub-index also showed an improvement, but only a marginal one, and remained (just) below the neutral mark, at 49.6. This improvement was driven by EMs, with China’s two export components clearly improving (possibly reflecting some US-China trade frontloading). Meanwhile, the export component for DMs dropped back to 47.8. We note a remarkable drop in this component for the US (-2.9 points to 46.8), Mexico (-4.9 points, to 44.2) and Canada (-3.5 points, to 46.8) – ostensibly tariff/trade policy uncertainty related (in the case of Canada/Mexico outweighing potential effects of frontloading).

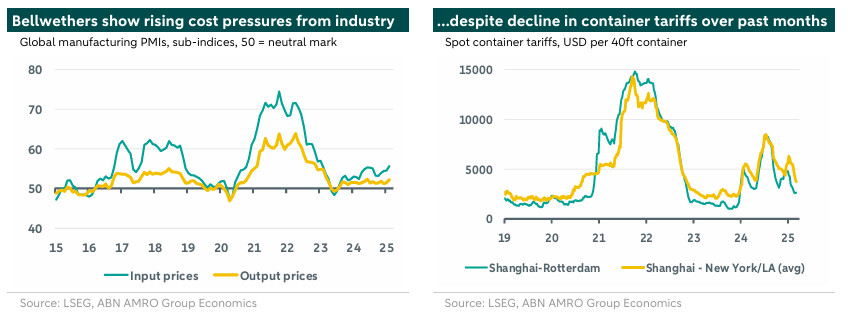

Price components suggest pressures from industrial goods’ prices are building again …

Tariff/trade policy also seem to be impacting to some extent the global manufacturing PMI’s price components, bellwethers for global cost-push pressures from industrial goods. The global PMI component for input prices rose by more than a full point in February, to 55.6, the highest level since January 2023. The output price component also picked up in February, rising by 0.7 points to an eight-month high of 52.2, but is still much closer to the neutral mark. This suggests that producers may still be somewhat hesitant to pass on higher input costs fully to their customers. Amongst the key economies, the US clearly showed (one of) the strongest rise in these subindicators. The input price component for the US jumped by almost five points to a 27-month high of 62.1, while the output price component rose by 2.1 points to a two-year high of 57.5. Although both the global and US input/output price components remain well below the peaks seen during the pandemic episode of widespread supply bottlenecks in 2021-2022, this should serve as a reminder that industrial goods’ cost price pressures are picking up again.

… although spot container tariffs keep falling so far

Unlike in 2021-2022, global container freight tariffs are not contributing to a rise in global industrial goods’ price pressures at the moment. After spikes in late 2023, throughout 2024 and early 2025, driven by disturbances in the Middle East, container tariffs have clearly come down again in recent months, both for Chinese-European and Chinese-American shipping routes (see chart). Hence, there are no signs that trade frontloading is driving up rates for shipping towards the US so far, possibly partly thanks to the gradual expansion in global shipping capacity and perhaps also reflecting use of other ways of transporting into the US.

US port fee plans may lead to serious disruptions in global shipping

While the further easing of container freight rates is a positive development for exporters and importers around the world, a US plan to sharply raise port fees for shipping companies that own Chinese (built) ships is leading to renewed fears of disruption in global shipping. The proposals include a sharp increase of port fees for China-related vessels (to a maximum of USD 1-1.5 mln per visit/entry, from around USD 50.000,-- currently), additional surcharges for companies who have orders outstanding at Chinese shipyards, and more stringent checks/restrictions on China-linked vessels leading to delays and higher costs. There are also proposals aimed at gradually reducing the share of total US exports transported on non-US ships by non-US shipping firms (to 85% in year 7 after the implementation of the new rules).

With these measures (based on a Sector 301 investigation launched by the Biden-administration), the US aims to reduce China’s dominance in shipbuilding: China’s share in global shipbuilding output was 51% in 2023, followed by South Korea (28%) and Japan (15%). As China-related vessels account for almost a third of the cargo visits to US ports each year, the proposals – if implemented in full – will likely have a big impact on freight costs, and will lead to other shifts in global shipping as well. According to some shipping experts, the expected rise in freight costs will be negative in the first place for US exporters (particularly those of bulk/agricultural goods) and for US consumers. Some other potential effects are 1) a longer-term shift in global shipbuilding from China to for instance South Korea and Japan (the US is not so well-positioned given capacity constraints), 2) a restructuring of shipping fleets and/or of shipping holding companies (while placing China-linked vessels into firms that do not visit the US), 3) an avoidance of US ports by shipping into Mexico and Canada and link with rail transport into the US; this may lead to a surge in rail freight rates given capacity constraints, but this route may lose attractiveness if the US broadens the 25% tariff scope on Canada/Mexico and 4) a reassessment by financial institutions of their exposure to Chinese-built shipping assets.

It is yet unknown whether the initial proposals would indeed be fully implemented. There is currently a consultation period, with a public hearing scheduled on the 24th of March, and it is also possible that (refined) proposals may be challenged in court later on. However, even if these proposals would be partially watered down over time, they are already creating uncertainties for global shipping, meaning that some of the longer-term shifts mentioned above are likely to start anyway.