Global industry still expanding, despite disturbances

Global manufacturing PMI drops marginally in June, remaining in expansion territory. Outperformance emerging economies continues. Excess supply conditions continue. Container tariffs keep rising, pick-up in industrial input/output prices more moderate so far.

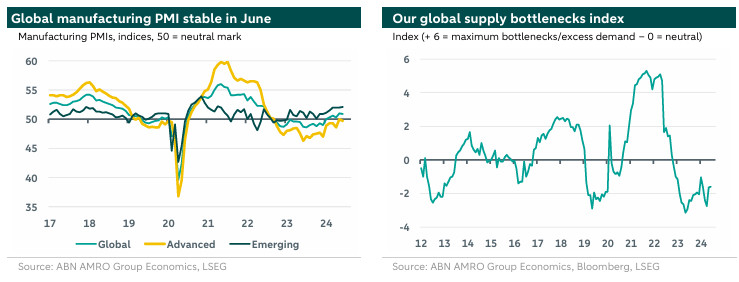

Global manufacturing PMI drops marginally in June, remaining in expansion territory

After having risen to a two-year high of 51.0 in May, the global manufacturing PMI dropped a touch in June, to 50.9, staying above the neutral mark separating expansion from contraction. The rise from a cyclical trough of 48.5-49.0 in the summer of 2023 to the current levels is consistent with our anticipation of a recovery in global industry, despite the flaring up of disturbances stemming from geopolitics. This view leans on our growth expectations for the key economies, with the eurozone bottoming out, China more or less stabilising amidst ongoing headwinds from the property sector and the US gradually cooling. That said, we still deem a very sharp rebound in global manufacturing unlikely for the moment – as rates remain restrictive, and the stepping up of trade tariffs is adding additional risks.

Outperformance emerging economies continues

Emerging economies continue to outperform, with the average EM index picking up marginally to a three-year high of 52.1 (May: 52.0). All BRICs showed improvements, with India (58.3) remaining the star performer. Caixin’s manufacturing PMI for China (included in the EM aggregate) reached a fresh high of 51.8, but the divergence with the NBS equivalent remained (see our comment on China’s June PMIs here). The aggregate index for the developed economies dropped back, to 49.7, after a jump in May. The deterioration amongst developed economies was particularly visible in Europe this time. Following a pick-up in May, the eurozone manufacturing PMI fell back even deeper in contraction territory, to 45.8, with the indices for Germany and France dropping to 43.5 and 45.4, respectively (see our comments on eurozone flash PMIs and our May Global Monthly for more on European competitiveness). The index for the Netherlands stayed in expansion territory, but fell back to 50.7 (May: 52.5) – see our comment here.

Excess supply conditions continue

Meanwhile, the various subindices of the global manufacturing PMI show that the supply side remains stronger than the demand side (see our April Global Monthly for more analysis on this). On the demand side, the global domestic orders component dropped back to 50.8 (May: 51.2), while the global export orders component fell below the neutral 50 mark again, to 49.4 (May: 50.4). On the supply side, the global output subindex also came down, but at 52.3 (May: 52.8) remained clearly in expansionary territory. These developments are also visible in our global supply bottlenecks index, for which an excess supply/demand metric is one of the key components. Due to this, our global supply bottlenecks index remained in excess supply territory in June, although other components (including shipping tariffs and delivery times) have moved this index a bit towards ‘neutral’ in recent months.

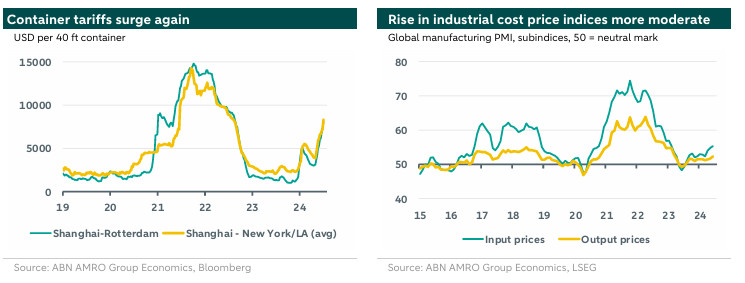

Container tariffs keep rising, pick-up in industrial input/output prices more moderate so far

As we highlighted in previous reports including our , spot container freight tariffs have surged again in recent months due to a combination of factors. The container tariff benchmark index has more than doubled since late April, although remaining below the 2021 peaks seen during the pandemic episode. While this situation bears close watching, we still think it is unlikely that these higher freight tariffs by themselves will move the needle on global goods inflation much, given the small contribution shipping costs make to the final cost of a good (around 1% on average), and given that (expected) capacity additions should at a certain moment in time act as a containing factor. More broadly, the current disturbances in global shipping are not comparable with the broad range of disturbances in global production and transport during the pandemic episode, at times when global demand conditions were also stronger.

That said, the global manufacturing PMI’s components for input and output prices – bellwethers for cost-push factors in global industrial goods’ prices – rose further in June, confirming once more that the disinflation in global industrial goods prices is fading. However, these bellwethers for cost-push factors remain well below their peaks seen in 2021/2022, and their rise is much less aggressive compared to the renewed spike in container tariffs. The input price component of the global manufacturing PMI rose to a sixteen month high of 55.3 (May: 54.9). The global output price component also picked up to 52.3 (May: 51.7), but remains at more moderate levels – suggesting that producers are still be a bit hesitant to pass on higher input costs, possibly reflecting demand concerns.