ESG Economist – Is there a business case for sustainability?

Sustainability and climate change seem to have lost relevance in a world marked by tariffs, wars, and inflation. This note aims to establish a business case for sustainability, despite a loosening of regulatory standards and less participation of greens in the European Parliament.

According to the recent Eurobarometer, European households recognize the direct impact of climate change on their lives and believe that EU climate initiatives are necessary

Additionally, the costs associated with carbon pricing have significantly increased expenditures across various sectors over the past decade and are expected to rise further given the implementation of EU-ETS 2

Furthermore, a US-only trade war may have positive spillovers for Europe’s energy transition by reducing costs and increasing the profitability of investments into transition technologies

Overall, with better economics and continued consumer focus on sustainability, businesses should continue to prioritize sustainability ambitions

In recent months, discussions have been dominated by defence, tariffs, and interest rates, overshadowing other critical issues like the transition and climate change. These environmental topics were prioritized during more stable macroeconomic times but now seem to have lost relevance. For example, European policymakers have postponed the setting of their 2040 ambitions and are whether to relax the 90 percent emission reduction target.

As this shift in focus occurs, businesses may question whether their priorities should also change and whether sustainability remains a viable business strategy. In theory, the case for businesses to transition to more environmental-business models rests on three primary reasons:

Regulation: Governments or regulatory bodies enforce rules that require businesses to operate more sustainably;

Consumer preferences: households increasingly prefer products and companies that are green;

Profitability: Investing in sustainable practices and/or business models results in an increase in profitability

In this note, we explore these three angles to assess whether sustainability still retains its business value.

Stringent regulatory standards for sustainability might loosen

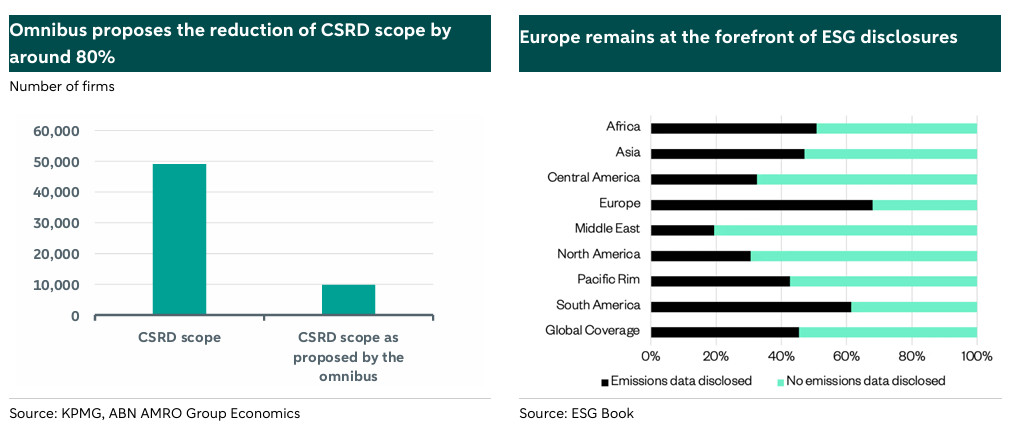

In 2019, the EU announced a strategic roadmap to make EU climate-neutral by 2050: the EU Green Deal. Part of that roadmap envisions more transparency on companies’ business practices and efforts towards sustainability. Due to that, EU regulators have been pioneers in the development of sustainability-related disclosure regulations. Nevertheless, following several critics about the excessive regulatory burden on companies and the overlap of certain sustainability regulations, in February, the European Commission introduced an omnibus proposal to streamline and reduce the regulatory burden faced by companies. The omnibus provides substantial simplification in the field of sustainability regulations, while squaring the EU’s ambitions towards a sustainable transition.

As we highlighted in a previous note (), one of the proposals in the omnibus is to reduce by around 80% the number of companies required to report on sustainability indicators. Despite reporting not having per se a direct impact into companies changing businesses practices, the European Commission has repeatedly emphasised the important role that it has in assisting with the climate transition. For example, by mandating sustainability reporting, regulators focused on increased transparency into corporate activities, which increases accountability. Furthermore, the reporting aims at helping investors to evaluate sustainability performance of companies, ensuring that capital flows to sustainable investments. With a reduction in the number of companies required to report on sustainability, there is a question on whether these previous goals by the European Commission are also not jeopardized.

Furthermore, as we pointed out, the European Commission postponed their 2040 targets and there are discussions about potentially loosening the 90% emission reduction target. Several member states have already been vocal about the need to reduce the target ().

All of these points might indicate that the EU seems to be easing its sustainability ambitions and loosening the regulations that it uses to achieve those ambitions. However, it is noteworthy to highlight that besides that loosening, the EU continues to be the most stringent in terms of sustainability practices. Furthermore, even though the omnibus proposes the reduction of data points that a company needs to report, other European regulations, such as the Capital Requirements Regulation (CRR) applicable to banks, still mandate the reporting of several different sustainability indicators.

Finally, the omnibus remains only a proposal, which still needs to be approved by the European Parliament and the European Council. So far, only a delay in reporting of some of the Directives has been approved. As such, although regulatory push might be easing, the regulatory forces that drive businesses to adopt more sustainable practices still remain in place. Let's now examine the other two driving factors: consumer demand and profitability.

Sustainability remains a top priority for consumers

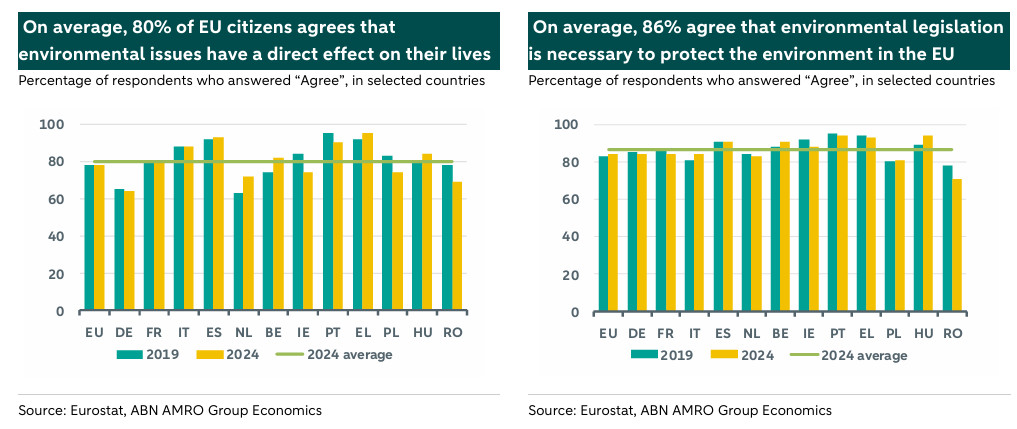

Academic literature acknowledges that a value-generating company benefits not only its shareholders but also enhances the value of all stakeholder interests, including those of customers and employees. Without creating value for customers, shareholder value cannot be realized. At the same time, the end demand for their products might well be impacted by the values and preferences of their customers. Therefore, it is important to consider how households perceive sustainability and EU environmental actions. The latest Eurobarometer included two questions on environmental issues: "To what extent do you agree that environmental issues directly impact your daily life and health?" and "How necessary is EU environmental legislation for protecting the environment in your country?" Below, we present the average results per country.

On average, in 2024, 80% of EU citizens agreed that environmental issues directly impact their lives – a number that only slightly decreased since 2019. Furthermore, 84% of EU citizens are of the view that EU environmental legislation is necessary to protect the environment in their country, although the overall average has also slightly decreased from the 2019 figures. As such, although with a small reduction over the years, the data from the Eurobarometer demonstrates that sustainability still remains a very important topic for EU citizens.

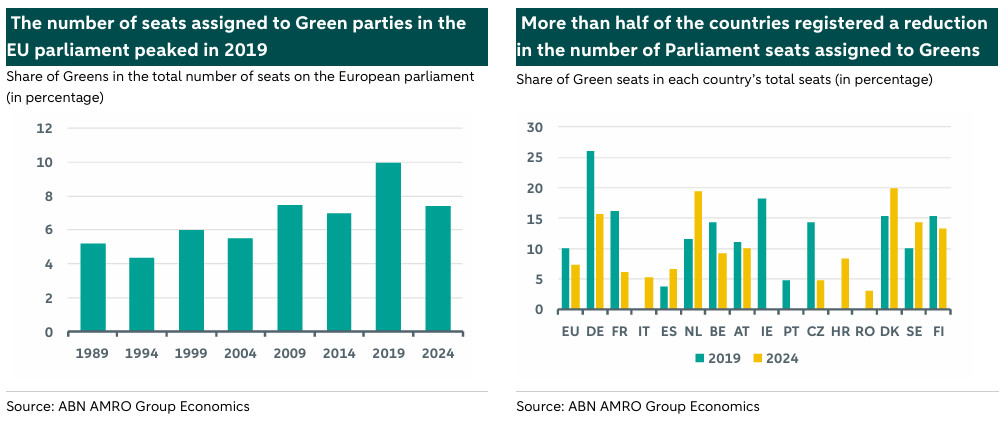

However, as we show in the charts below, this perceived importance has not been fully reflected into citizens’ voting behaviour. As indicated by the chart on the left below, the Green parties experienced their highest allocation in 2019, securing 10% of the total seats. However, this figure has recently decreased to just below 8% in the latest election. In our opinion, this is a clear reflection that, despite recognizing sustainability as a significant issue with direct impacts on their lives, households may still prioritize other topics, such as defence or economic growth, over environmental concerns. Hence, while consumers continue to regard sustainability as crucial, it may not be as pressing as other issues at present.

Overall, the data seems to indicate that sustainability remains part of EU citizens’ consumer preferences, although the political sphere reflects that sustainability might not be the most imminent and pressing concern at the moment. This political shift might also help explain the loosening of sustainability regulation, as we discussed in the previous section. Nevertheless, we still deem the demand force to continue to exert some pressure on businesses to transition to more environmental-friendly practices.

Transitioning will also prove cheaper for consumers and businesses

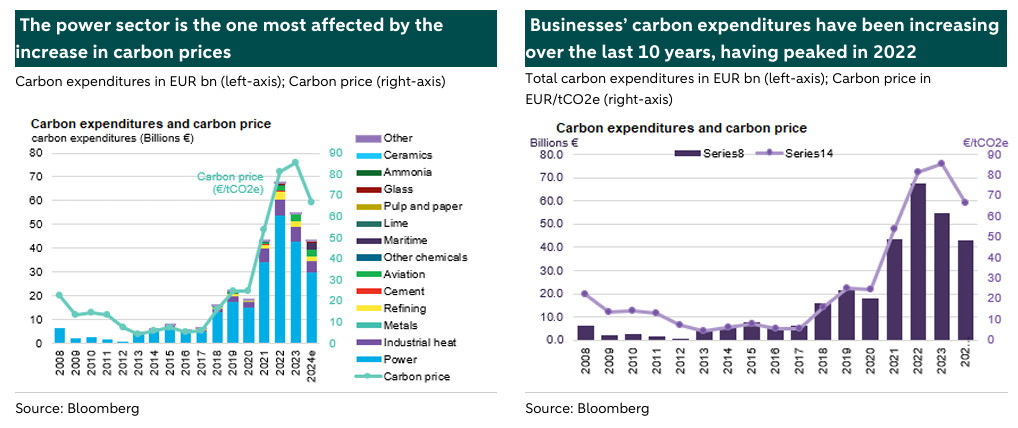

Lastly, we discuss whether from an economical point of view, there is still a business case to be made towards sustainability. We explore this topic through two different angles: the ETS and the macroeconomic environment. Over the years, the EU has implemented two cap-and-trade systems aimed at reducing greenhouse gas emissions: the European Union Emission Trading System (EU-ETS) and EU-ETS 2. EU-ETS 2 will be gradually introduced starting in 2025 and will be fully operational by 2027. Although both systems function similarly, they target different sectors. EU-ETS covers emissions from electricity generation, heavy industry, aviation, and international shipping, while EU-ETS 2 addresses emissions from road transport, buildings, and other light industries. The aim is to annually reduce emissions at a linear reduction factor of 4.3% for ETS1 and 5.15% for ETS2, which should also be helped by increasing the trading prices of emission allowances.

According to the graphs above, total carbon expenditures by businesses have been increasing since the introduction of the carbon price. They have nevertheless peaked in 2022 following the start of the Ukraine-Russian conflict.

In a recent note, we explained how EU-ETS 2 will affect end consumers through various channels, both direct and indirect (). Indirect costs are related to overall price increases, particularly for products heavily reliant on heating and transportation. Businesses might pass on increased fuel costs to consumers in sectors like agriculture (e.g., produce from greenhouses), construction (e.g., building materials), chemicals, or metals. For reference, the European Central Bank (ECB) anticipates that EU-ETS 2 could raise inflation in the euro area by 0 to 0.4 percentage points in 2027, with a milder impact in 2028. This highlights the need for proactive carbon mitigation strategies. Besides the financial incentives that the ETS provides for businesses to reduce carbon emissions, some climate-friendly measures might also prove to be earnings accretive in the long-term. For example, in previous pieces ( and ), we highlight how energy efficiency renovations for real estate companies can be financially attractive due to expected savings on energy costs, despite the large upfront investment.

Besides the ETS, which is a governmental policy and not applicable to all sectors and/or businesses, we should also evaluate whether the macro environment still allows for positive economics from investing in more clean/green technologies. In a recent a note we explored how the trade war might affect the energy transition, which you can access

Investing in transition technologies is affected by different factors, such as regulation, infrastructure readiness, financing and technology costs, as well as the resilience of supply chains. Accordingly, trade policies would affect the transition through their impact on investment costs (both CAPEX and OPEX), infrastructure development, global supply chains of critical metals and transition technologies, and financing costs. Different forms of trade barriers would reshuffle trade flows and supply chains of key transition technologies. All of which will affect cost structures and investments in clean technologies.

If a trade war were to occur between the US and the rest of the world, but without tariff escalation between the EU and China, the EU's energy transition could potentially benefit from decreased technology and financing costs. The latter would be driven by lower interest rates, which constitute approximately 40% of the total costs for renewable energy technologies. However, there is also a risk that banks may tighten lending conditions, driven mainly by a slowdown in the economy, which could drive up corporate default rates.

Concurrently, technology costs could be reduced under the scenario where the EU keeps their tariffs on Chinese imports unchanged, implying that a US invoked trade war with China would decrease equipment prices for European developers and push the transition forward which would enhance European energy security and achieve climate outcomes. At the same time, the trade war could result in European manufacturers of clean technologies having to face increased competition from Chinese products. The overall effect of such a US-initiated trade war will depend on factors like the business cycle, emerging bottlenecks, the progress in developing supporting infrastructure, and any shifts in climate goals, targets, commitments, or regulations. Still, the current macro and geopolitical scenario could prove to be a tailwind for transition technologies by reducing costs and hence, improving the profitability and the economics of these investments.

Overall, transitioning seems to be the way forward

In summary, despite the political shift towards topics like defence and economic growth, reflected in the reduced presence of green parties in the European Parliament, sustainability continues to present a viable business case for companies. This is largely driven by three key factors: regulation, consumer preferences, and profitability. Regarding regulation, although there is a proposal to ease the compliance burden on companies, which still awaits adoption by the European Parliament and Council, existing regulations remain in effect, and banks and large companies are expected to adhere to stringent sustainability reporting standards.

Regarding consumers, there is a consensus that environmental issues adversely affect their daily lives, and they recognize the importance of taking action. In terms of profitability, after several years of clean technologies experiencing increased costs that negatively impacted margins and internal rate of returns, the macro environment appears to be heading towards more favourable conditions for these investments, despite the risk that banks tighten lending conditions on the back of lower growth prospects and higher default rates. That is because, if the trade war is confined to a US-initiated conflict rather than a global one, investors might benefit from a strengthened EU-China alliance. This could alleviate cost pressures on investments in transition technologies and ultimately boost their profitability, further encouraging other businesses to invest in the transition.