ESG Strategist - Omnibus: watering down EU’s climate ambitions

Yesterday, the European Commission (EC) published the Omnibus proposal (1). This proposal follows the recommendations of the Draghi report (2) and the EC’s promise to reduce administrative burdens by at least 25% and by at least 35% for SMEs before the end of the mandate in 2030. It aims to provide substantial simplification in the field of sustainability regulations, while squaring the EU’s ambitions towards a sustainable transition and enhancing EU companies’ competitiveness. The package released by the EC includes amendments to the Corporate Sustainability Reporting Directive (CSRD), the Corporate Sustainability Due Diligence Directive (CSDDD), the InvestEU Regulation, and the Carbon Border Adjustment Mechanism (CBAM), which we will analyse in a later note. The package is accompanied by a draft Taxonomy Delegated Act for public consultation. In this note we will analyse the proposed changes and compare them to the previous regulations. Moreover, we conclude by making an assessment of how these changes will impact the transition and the achievement of EU’s 2050 climate targets.

The European Commission (EC) released the Omnibus proposal yesterday

The documents signal a relaxation of the EC’s climate standards

The biggest change regards the number of entities required to report under the CSRD which is likely to decrease by 80%, excluding all SMEs or companies with fewer than 1,000 employees

The former would only need to report under voluntary standards (VSME)

Moreover, according to the proposal, financial entities are also exempt from reporting obligations under the CSDDD

With regards to changes in the Taxonomy Disclosures Delegated Act, loans to SMEs are excluded from Green Asset Ratios’ calculations

The proposal still requires approval by the European Parliament and Council, so further changes are expected

Nonetheless, we view this proposal as a relaxation of the EC’s standards, risking a deterioration in ESG data quality and availability

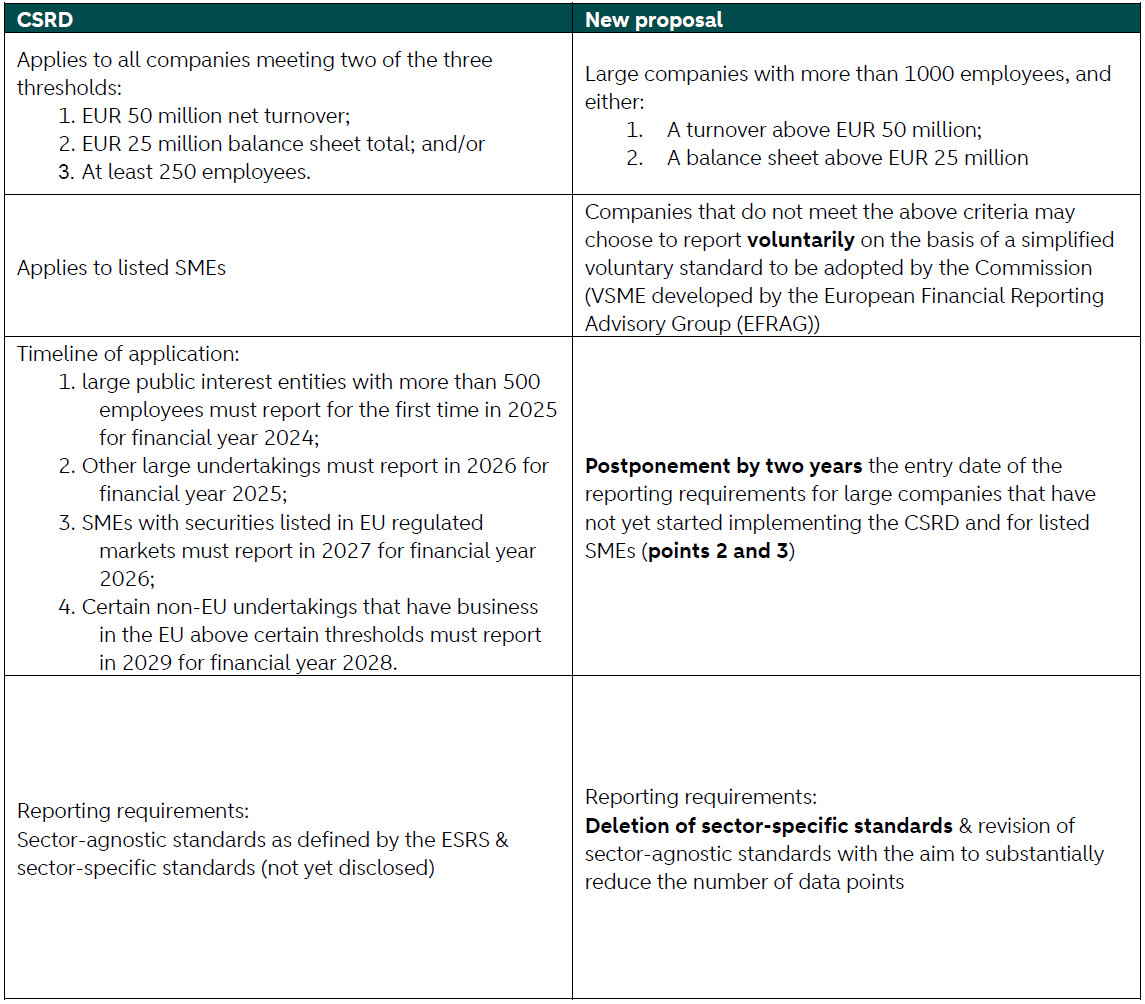

CSRD

In the table below we compare the CSRD adopted in November 2022 with the new proposal.

Some of the changes are in line with the recommendations we shared in our previous note, but the Omnibus also includes some surprises which might indicate a relaxation of the European Commission’s standards, and ultimately, of their climate ambitions.

For example, based on the numbers disclosed by the European Commission, the number of companies subject to the CSRD will decrease by about 80% if the European Parliament adopts this proposal. This would exempt listed small and medium-sized enterprises (SMEs) and companies with fewer than 1,000 employees from the reporting requirements. However, SMEs collectively contribute a significant share of total enterprise emissions, accounting for 63.3% of all CO2 and greenhouse gas emissions by enterprises, as noted in a previous report. Therefore, these companies will still need to reduce emissions if the European Commission is to uphold its climate commitments. Excluding them from reporting requirements does not address the obstacles they face in transitioning, nor does it equip them with the necessary tools for measuring and monitoring emissions. Removing the incentives for SMEs to gain insights into their emissions will likely reduce their motivation to lower those emissions as well.

Furthermore, banks and other large non-financial entities are still required to comply with the SFRD and the CSRD. To fulfil these obligations, they depend on disclosures from SMEs, as the carbon footprint of SMEs is effectively part of their own carbon footprint. Allowing SMEs to make disclosures voluntarily could hinder the reporting obligations of these larger entities, resulting in large data issues. Ultimately, this will likely affect investors as well, as they rely on such disclosures to assess and manage risks. In short, data credibility and availability is at stake.

Finally, in what regards the standards developed by the ESRS, we are supportive of their revision and consequent simplification. As mentioned in our previous note, emphasis should be placed on developing robust quantitative metrics that are genuinely useful for decision-making by investors, rather than generating lengthy qualitative statements. Ultimately, qualitative criteria are harder to assess and require a judgment call from investors.

However, concerning the proposal to delete sector-specific standards, this would also hinder the progress done so far. Indeed, various stakeholders agree that tailored guidelines are crucial to more effectively address the unique challenges and impacts of different industries. For instance, industries such as mining, energy, agriculture, or technology have distinct environmental and social impacts that generic standards might not adequately capture. Also investors often favour sector-specific standards for reporting because they provide more detailed and comparable data, enabling better assessment of risks and opportunities within specific industries.

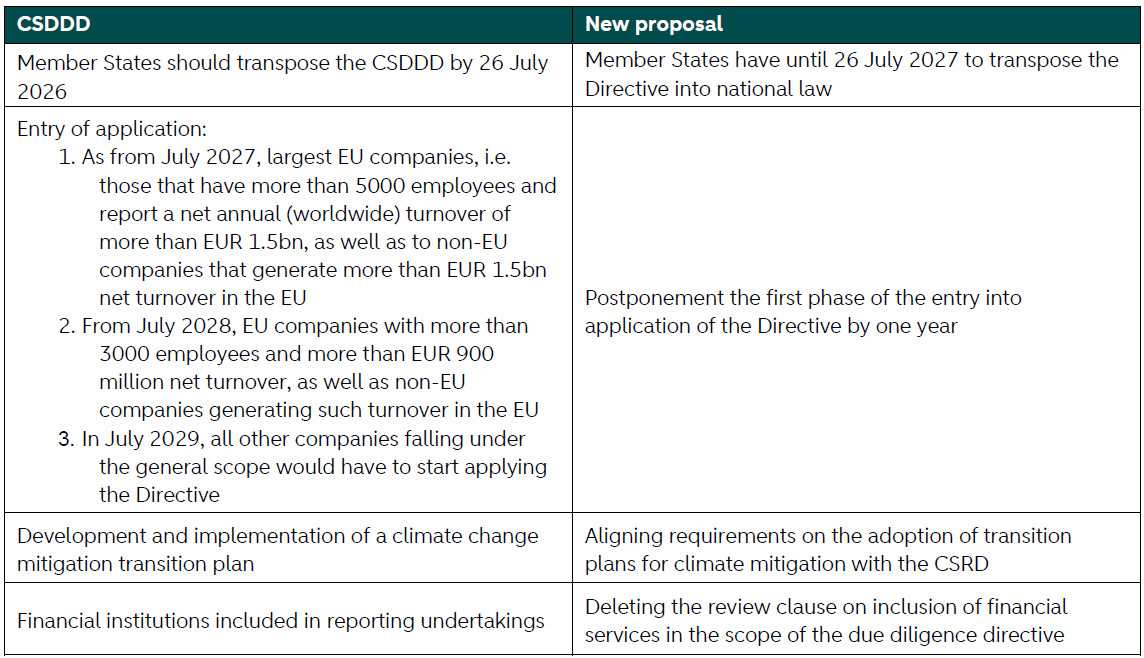

CSDDD

Below we present the main differences between the previous CSDDD proposal and the new proposal.

Regarding the changes in application dates, we agree that postponing the adoption of the Directive is the best course of action. This delay will provide companies some additional time to prepare for implementing the new framework. Meanwhile, it is important for the Commission to advance the necessary guidelines to July 2026, enabling companies to better develop best practices and lessen their dependence on legal counselling and advisory services.

Furthermore, streamlining regulatory expectations for transition plans constitutes a positive change to the directive, given that it will improve clarity and support effective implementation. This change will further help investors access valuable data and support their ability to evaluate the transition efforts effectively.

However, the exclusion of financial companies from reporting undertakings – were to be approved – would represent a weakening of the EC’s standards, as highlighted in our previous note. In July 2024, The assessed the world's 2,000 most influential companies and found that about 90% of financial institutions scored zero on human rights due diligence. This aligns with the findings, which revealed that 80% of financial institutions did not acknowledge their environmental or societal impacts. Despite the progress observed in the industry, these figures underscore the need for mandatory measures to promote responsible conduct in the finance industry, driving the transition to a more just and sustainable green economy.

Taxonomy Climate Delegated Act

The Taxonomy Climate Delegated Act sets out reporting obligations laid down in Article 8 of the EU Taxonomy. It specifies key performance indicators for financial and non-financial undertakings. While non-financial undertakings have to report on the Taxonomy-alignment of their turnover, capital and operation expenditures (turnover, CapEx, OpEx KPIs), financial undertakings report on the percentage of their investments and their assets under management that are aligned with the EU Taxonomy. As regards credit institutions, the key metric in this assessment is the Green Asset Ratio (GAR), which measures the proportion of Taxonomy-aligned assets to total covered assets in a credit institutions’ current (GAR stock) and future portfolios (GAR flow). Therefore, and in line with the changes to the CSRD, loans to SMEs were excluded from the GAR, regardless of their environmental credentials, as per the Taxonomy Disclosures Delegated Act.

Some changes are still expected to the final Omnibus

To conclude, the changes proposed under the Omnibus proposal seem to constitute a loosening of the EC’s standards, despite a few positive changes.

The most notable change is the 80% reduction in the number of companies required to report under the CSRD. If this change is approved, banks, large enterprises, and investors would become increasingly reliant on voluntary reporting. Moreover, for financial undertakings, it will prove even more challenging to comply with reporting standards were these to remain unchanged Ultimately, there is a clear risk that these proposed changes could undermine the credibility of the data. Therefore, it remains to be seen whether providing detailed guidelines and support to SMEs for their reporting requirements would be more beneficial and efficient than excluding them from the regulations.

However, it is important to note that this Omnibus proposal is still just that—a proposal. The legislative proposals will now be submitted to the European Parliament and the Council for consideration and adoption. The changes to the CSRD, CSDDD, and CBAM will only take effect once the co-legislators have reached an agreement on the proposals and they are published in the EU Official Journal.