ESG Strategist - Omnibus: simplifying or watering down EU’s regulations?

On November 8, 2024, the EC President Ursula von der Leyen announced that existing and upcoming EU ESG reporting requirements will be integrated into an omnibus regulation. An omnibus is a regulatory measure or set of rules that encompasses a broad range of issues or topics within a single document or framework. The EC’s goal with this approach is to streamline the growing number of requirements faced by companies, ensure consistency across related areas, and simplify processes for both regulators and those being regulated. In this overview, we will examine the three existing regulations likely to be unified under the forthcoming omnibus: the EU Taxonomy Regulation, the Corporate Sustainability Reporting Directive (CSRD), and the Corporate Sustainability Due Diligence Directive (CSDDD). Our objective is to clarify the purpose of each regulation, explore each regulation’s flaws and discuss how the upcoming omnibus might overcome these flaws and streamline the three regulations.

In November 2024, the European Commission (EC) announced that existing and upcoming EU ESG reporting requirements will be integrated into an omnibus regulation

The omnibus intends to streamline the growing number of requirements faced by companies and avoid the overlapping of existing regulations

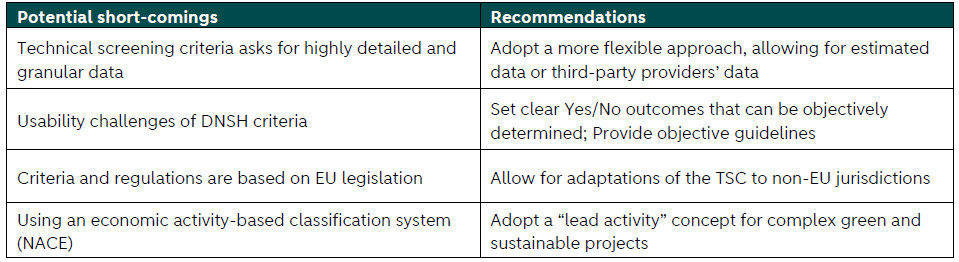

With regards to the Taxonomy Regulation, some criticisms regard the lack of flexibility of the Technical Screening Criteria (TSC), the excessive reliance on EU legislation, and the complexity of using an economic activity-based classification system (NACE)

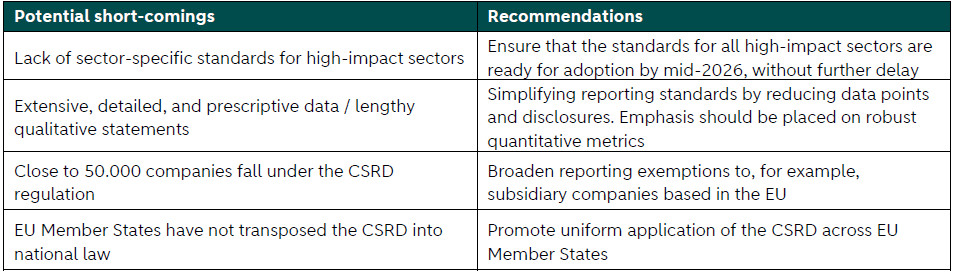

Criticisms of the CSRD include the delay of sector-specific standards for high-impact sectors, the extensive qualitative details, and the lack of uniformity across EU Member States

Finally, several regulators agree that the adoption of the Corporate Sustainability Due Diligence Directive (CSDDD) should be delayed until the omnibus is implemented, and find that the reporting and implementation of transition plans should be streamlined across EU legislation

Leaks concerning the omnibus suggest that the number of reporting companies could be reduced, and financial companies might be excluded from CSDDD reporting

These changes would weaken the previously established reporting standards across Europe, representing a setback towards achieving the 2050 targets

Nevertheless, the omnibus could still prove positive if it just guarantees the simplification and streamlining of regulations

“There are many barriers that lead to companies in Europe to “stay small” and neglect the opportunities of the Single Market. These include the high cost of adhering to heterogeneous national regulations, the high cost of tax compliance, and the high cost of complying with regulations that apply once companies reach a particular size”.

The Future of European Competitiveness, Mario Draghi (September 2024)

EU Taxonomy Regulation

The EU Taxonomy Regulation was the first regulation to be published after the announcement of the European Green Deal in December 2019. The Taxonomy defines a classification system to establish which activities qualify as ‘green’ or ‘sustainable’. Moreover, its role has been expanded to serve as a metric for sustainable reporting and as a way to measure progress towards the policy objective of a sustainable financial and economic system in the EU.

The Taxonomy Regulation defines as environmentally sustainable all activities that:

Substantially contribute to one or more of the environmental objectives (SC): the activity must significantly advance at least one of the six environmental objectives outlined by the EU Taxonomy;

Do no significant harm any of the other environmental objectives (DNSH): while contributing to one objective, the activity must not significantly harm any of the other environmental objectives;

Meet Technical Screening Criteria (TSC): the activity must satisfy specific technical screening criteria that are detailed for each sector and type of activity. These criteria provide quantifiable benchmarks and thresholds to ensure that the activity genuinely contributes to environmental sustainability; and

Comply with Minimum Standards (MS): the activity must adhere to minimum social and governance standards, which are currently aligned with guidelines such as the OECD Guidelines for Multinational Enterprises and the UN Guiding Principles on Business and Human Rights.

Despite being an important step towards a greener economy, and having been used as a precedent for many other jurisdictions, the EU Taxonomy has its flaws.

Most of the criticism has focused on the criteria defining an activity as environmentally sustainable. One key issue is that the TSC demands issuers to possess highly detailed data, which is often unavailable. The lack of such data hinders the ability of market participants to provide ESG-related disclosures (such as the Green Asset Ratio (GAR), as highlighted in our previous note – see here). This issue can be even more pressing for smaller companies and projects, ultimately making it disproportionately harder for these entities to demonstrate alignment with the EU Taxonomy. To overcome this issue, the International Capital Markets Association (ICMA) suggests adopting a more flexible approach to the TSC assessment, and to allow corporates to use estimated data or data from third-party providers, where data is unavailable. Regarding the heightened difficulty for smaller companies and projects, there are proposals about making the criteria looser (particularly for the DNSH assessment) for projects with no or insignificant foreseeable impact given its type or location, for instance.

Moreover, issues have also been raised with regards the DNSH criteria. For instance, the Platform on Sustainable Finance recognises that DNSH poses significant usability challenges to preparers of Taxonomy reporting and therefore recommends the EC to review and provide supplementary guidance to reporters. The Platform recommends the EC to ensure that all DNSH criteria:

Have clear Yes/No outcomes that can be objectively determined; and

Minimise subjective language in technical screening criteria, while ensuring that guidance is given on what a suitable Yes/No outcome is for process-based tests, in the form of supplementary guidance.

Additionally, the TSC are based on EU legislation, posing challenges for assessing Taxonomy alignment for activities that are not conducted in the EU. The Minimum Standards also reference international agreements not adopted universally. Moreover, references to EU Directives within the TSC could lead to inconsistent application of the EU Taxonomy within the EU itself, as different Member States may have varying transposition laws. This inconsistency could further complicate ESG disclosures for non-EU exposures of financial entities. To address international differences, the Taxonomy Regulation should allow for adaptations of the technical screening criteria to non-EU jurisdictions, such as incorporating location-based contextualization for SC and DNSH assessments. This would acknowledge regional variations and existing market frameworks.

Finally, there is criticism of using an economic activity-based classification system (NACE). While some projects are straightforward and align easily with the Taxonomy's economic activity definitions, others, such as large-scale infrastructure projects, complicate Taxonomy alignment assessments. A green or sustainable project may involve multiple economic activities, each potentially aligning with different environmental objectives and Taxonomy Delegated Acts. A case study (see ) revealed that a single development project (for instance, a development project to be constructed on lands that previously constituted a brownfield site on reclaimed land) in the EU could involve 25 economic activities, each requiring compliance with several SC TSC and DNSH TSC, along with detailed data points. ICMA suggests simplifying the NACE classification for complex green and sustainable projects by adopting a “lead activity" concept.

CSRD

The CSRD mandates that companies adhere to specific standards to meet their legal obligations for sustainability reporting. Alongside the EU Taxonomy Regulation and the Sustainable Finance Regulation Disclosure (SFRD), these form the core elements of the EU's sustainability reporting framework, integral to its sustainable finance strategy.

Since 2024 listed companies with over 500 employees that previously had to comply with the Non-Financial Reporting Directive (NFRD) have to also apply the CSRD rules (in 2024 reports due in 2025). The reporting companies will be expanded to all large companies (more than 250 employees though some supplementary financial metrics are also used to define this category) from 2026 (annual reports of 2025). Finally, small and medium (SMEs) listed companies will start such reporting in 2027 (annual reports of 2026), although with an option to delay for two years. As of 2029, also non-EU parent companies with at least one European branch will have to comply with the CSRD.

The CSRD stipulates that all reporting companies must disclose information regarding their perceived risks and opportunities from social and environmental issues ("outside-in") and the impact of their activities on people and the environment ("inside-out"). This approach is known as the double materiality assessment. To facilitate this process, the Commission has introduced the European Sustainable Reporting Standards (ESRS), which assist companies in more effectively communicating and managing their sustainability performance.

Parts of the ESRS (for instance, regarding the adoption of sector-specific standards for high-impact sectors) has been postponed until 2026. Without targeted disclosures, reporting entities in these sectors may face challenges in conducting comprehensive materiality assessments of their significant exposures and impacts, in alignment with the sector-neutral ESRS. As such, market participants have been urging the Commission to guarantee that the standards for all high-impact sectors are ready for adoption by mid-2026, without further delays.

With the implementation of the ESRS, companies are now required to meet extensive, detailed, and prescriptive data requirements, provided they are material. However, as we previously discussed, data availability can also prove to be an issue to comply with these reporting requirements, particularly for smaller entities. Furthermore, there are question marks about whether the extensive qualitative details required are genuinely beneficial and decision-useful for investors and stakeholders. Emphasis should be placed on developing robust quantitative metrics that are genuinely useful for decision-making by investors, rather than generating lengthy qualitative statements. Ultimately, qualitative criteria are harder to assess and require a judgment calls from investors. Nevertheless, we do agree that, where quantitative data is not available, qualitative data should be provided.

Moreover, the adoption of the CSRD has broadened the universe of companies that need to comply with it. For instance, while 11,700 companies had to comply with the NFRD, this number increased to 46,000 with the adoption of the CSRD (including listed SMEs). The latter includes companies based in the EU, have subsidiaries in the EU or are listed on its regulated markets. However, some suggest that the CSRD should extend the reporting exemption to subsidiary companies that are large undertakings and public-interest entities, provided their reporting is included in the consolidated report of the parent company. In the instance of the parent company being located outside the EU, this might involve aligning the parent company’s sustainability practices with EU standards to facilitate compliance at the subsidiary level.

There is also a discussion regarding increasing the threshold for CSRD compliance (that is, only companies with more than 1000 employees would need to report on CSRD), resulting in less companies being subject to the extensive ESG reporting requirements. This argument is based on the additional cost and lack of data availability that can be particularly challenging for smaller entities.

Lastly, promoting uniform application across EU Member States is essential. Currently, several member states have not yet transposed the CSRD into national law, leading to fragmentation, confusion, and an uneven playing field within the EU. Improvements to the regulatory instruments addressed by the omnibus should aim to garner broad support for consistent implementation throughout the Union.

CSDDD

The CSDDD establishes a corporate due diligence obligation for large companies to identify and address negative impacts on human rights, such as child labour, and environmental issues, such as pollution, within their own operations, those of their subsidiaries, and across their "chain(s) of activities." Additionally, the Directive requires large companies to develop and implement a climate change mitigation transition plan. This plan aims to ensure, through best efforts, that the company's business model and strategy align with the transition to a sustainable economy and support the goal of limiting global warming to 1.5°C, in accordance with the Paris Agreement and the EU's 2050 targets.

The development and disclosure of transition plans overlap with Article 19 of the CSRD and the Capital Requirements Directive (CRD). Although companies that provide transition plans under the CSRD are exempt from additional plans under the CSDDD, the EU's regulatory regime for transition finance remains a fragmented and non-mandatory patchwork, as seen with the CSRD. This inconsistency limits investors' access to valuable data and hinders their ability to evaluate transition efforts effectively. Furthermore, if a company lacks targets and transition plans, the current rules allow them to simply explain this absence, highlighting a 'comply or explain' gap in the EU framework. Streamlining regulatory expectations for transition plans would improve clarity and support effective implementation. The IIGCC suggests for the Commission to introduce detailed transition plan requirements under the CSDDD's Level 2 standards, closely aligning them with the CSRD to ensure a consistent approach to transition plan adaptation and implementation across the EU.

Many IIF members consider that the date of application of the CSDDD (from 2027 onwards) should be delayed pending the finalisation of the omnibus process and the development of the necessary implementation guidance. Also, ICMA suggested to adjust timelines for pending legislation to allow for logical sequencing and implementation feedback. Even though ICMA does not comment on the CSDDD specifically, the agency suggests that delaying the enforcement for reporting might be the best solution for the time being.

To conclude: simplifying or watering down EU regulations?

A lot of investment is necessary to meet the European Union's 2050 climate targets. Much of the funding for this investment must come from the private sector, making investors vital in directing capital towards climate solutions. However, for investors to make informed, data-driven decisions, they require access to high-quality, comparable data, positioning them as key users of sustainability disclosures.

The existing ESG disclosure regulation in the EU was designed as to ensure that reporting on sustainability-related matters is widely available, standardised and applied consistently, closing many of the data gaps that are repeatedly cited by financial market participants as a key barrier to sustainable investment and meeting their own reporting obligations.

As such, EU sustainability regulations help investors to manage risks, identify opportunities, and ultimately reorient capital towards a more competitive, equitable, and prosperous net-zero economy.

However, the current set-up of EU ESG regulations might be hindering these objectives, as we discussed previously. As such, simplifying and improving the coherence of the EU sustainable finance framework could help to address this issue. Such revisions can effectively reduce reporting burdens and complexity and promote a more coherent approach to the transition across the value chain. As long as those revisions are not done at the expense of loosening standards for firms.

Recently, have suggested potential changes with the upcoming Omnibus implementation. One proposed change involves the size of companies required to report under the CSRD and CSDDD. While currently, all companies except non-listed SMEs and micro listed entities are expected to report from 2027, the new proposal limits reporting to companies with more than 1,000 employees (that is, the threshold for compliance would be reduced). This change would loosen the standards and could prove significant. In a previous publication, we discuss how SMEs, despite their smaller size, are on aggregate high carbon contributors to the EU (contributing to around 63% of all CO2 and greenhouse gas emissions by enterprises). As such, excluding those from EU reporting requirements can threaten the ability to ensure that capital is efficiently allocated to high carbon-emitting entities. Hence, such relaxation of the scope of applicability of the CSRD would imply a step back in EU climate efforts, while a more effective solution would be to focus exemptions only on subsidiary companies located in the EU, as long as the parent company complies with EU standards.

Another concern is the potential exclusion of financial institutions from the CSDDD regulation. For example, in July 2024, the assessed the world's 2,000 most influential companies and found that about 90% of financial institutions scored zero on human rights due diligence. This aligns with the findings, which revealed that 80% of financial institutions did not acknowledge their environmental or societal impacts. Despite the progress observed in the industry, these figures underscore the need for mandatory measures to promote responsible conduct in the finance industry, driving the transition to a more just and sustainable green economy. Excluding financial institutions from the CSDDD would therefore represent a weakening of standards and a setback towards achieving EU targets.

The same leak disclosed earlier this week suggests also a possibility of the new CSDDD excluding requirements for companies to implement a transition plan. As long as this requirement is still included in the CSRD (which has a biggest scope than the CSDDD), such addition could prove not be so detrimental as originally thought, and would allow for a streamlining of expectations related to transition planning as we previously discussed.

Overall, it is crucial to evaluate whether the Omnibus genuinely simplifies the process or merely weakens the previously established reporting standards across Europe. Although the Omnibus aims to enhance climate investments throughout the European Union, relaxing these requirements might inadvertently hinder progress, potentially setting back the EU's ambitions. The first draft of the omnibus will be published on 26 February 2025. We deem changes that deviate from the points discussed above as potential signal that the EU is watering down its ESG regulations.