ABN AMRO fixed income - when US recession fears ebb, credit spreads will make a comeback

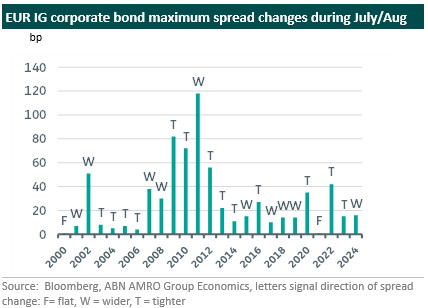

In this comment we analyze the sell-off in various spread sensitive European fixed income markets. European credit bond markets were obviously not immune to Monday’s market turmoil and the key gauges for synthetic credit spreads moved sharply, with 5y CDS spreads on the Itraxx main and cross-over widening by 5bp and 35bp respectively since Friday. Swap spreads and semi-core / peripheral country spreads reached levels seen during the French snap election. One could perhaps argue thin holiday liquidity as the key culprit behind the sharp moves. Looking back at summer months (July and August) over nearly 25 years, 16bp of widening in spreads on the broad corporate debt index actually looks reasonable in comparison to the spread widening during 2018 and 2019 for example. Actually, the absolute level of spread widening today is not meaningfully different than to 2018 when there were fears about too much central bank policy tightening as well.

Co-author: Sonia Renoult

US recession fears have started to creep into the markets and to us seems to be the chief reason behind the market sell-off, more so than geopolitical events or the unwinding of the Yen carry trade. Indeed, Friday’s non-farm payrolls disappointed, but our macro-team does not see this translating into an upcoming US recession (although recession risks have risen), yet more a sign of a balanced US labour market as labour supply starts to catch-up. The latest ISM services PMI released yesterday evening basically confirmed this picture, especially when you look at the new orders component. As such the Fed is not behind the curve in terms of restrictive policy and we also do not see them reacting with an ad-hoc rate cut (this is also not expected by market consensus).

Bond spreads are trading flat to yesterday’s close this morning, suggesting that the market has found some footing. Since the odds are still favouring the US economy to continue to grow, albeit at a slower pace, we believe that the recent widening in credit spreads is overdone and presents a buying opportunity. Below we provide the reasoning for various asset classes, including sovereigns, bank debt and utility debt.

Market Overreaction in rate space: anticipating yield and spreads corrections

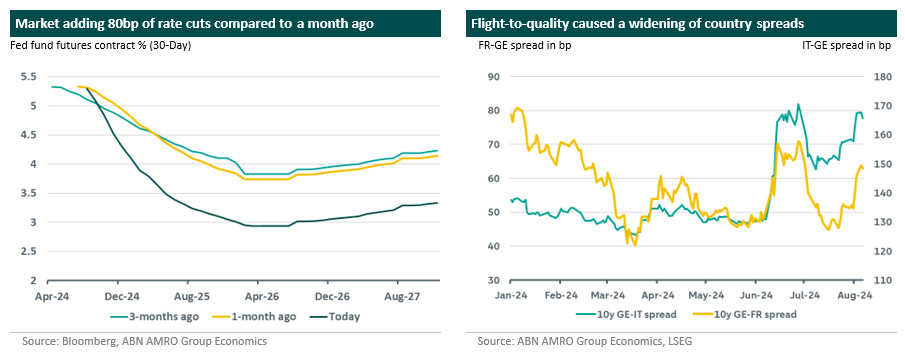

Based on our recently published macro update (see here), we believe that yesterday's market reaction in the rates space was overdone. As illustrated in the left hand graph below, the market has priced in as much as 80 basis points of additional rate cuts for 2025. Currently, the market estimates the Fed's terminal rate to be closer to 3%, a significant drop from 4.15% just a month ago. Thus, most of the move we have seen in US rates was triggered by the market’s repricing of the Fed policy rate on the back of rising recession fear.

While this recent development aligns the market's outlook more closely with ours—at least in the long term—we anticipate an upwards correction in Treasury yields over the coming weeks. We expect this correction to primarily occur at the front end of the curve, which has experienced the most significant rally in recent days. Despite last Friday’s weakness in labour data, our base case still entails a soft landing scenario, without the US falling into recession. Consequently, we believe that the market has prematurely adjusted its expectations for rate cuts in the upcoming FOMC meetings and should start to reprice it out again.

As such, we expect the Treasury yield curve to bear-flatten again until the excess rate cuts are priced out. This correction already begun today with the front-end of the curve shifting higher by a couple of basis points.

The rising fears of a U.S. economic recession has also influenced the European rates market, triggering a flight to quality that has led to a significant widening of both swap spreads and country spreads over the past week, as the Bund rallied. As previously discussed, we believe this recent market reaction to be excessive, and thus expect a retreat in swap and country spreads to occur as well.

In particular, we do not anticipate an economic recession in the Eurozone, and we expect the ECB to continue cutting rates this year and into 2025. Overall, this environment should support a tightening of peripheral spreads for the remainder of the year.

Bank debt has become even more attractive vs non-financials

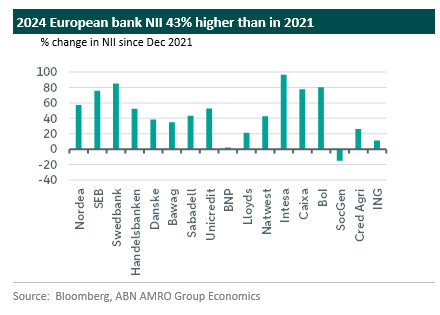

Bank debt spreads widened more than non-financials and the lower ranks of capital obviously took a larger beating. One could perhaps argue that the market is fearing aggressive rate cuts by central banks, which could take the tailwind out of banks’ profitability. Still our estimates for the terminal policy rates remain significantly higher than during the low interest rate environment of 2017-2021. Furthermore, the chart below shows the change in NII between the end of 2021 and mid-2024 for NII reliant European banks that have so far reported Q2 2024 numbers. Current profit generation remains solid, with the exception of French banks. This also indicates that when we reach the terminal rate the NII will remain comfortably above pre-2022 levels.

Many banks are already reporting a pick-up in lending growth to support stable to slightly declining liability margins. With European economies on the cusp of a (shallow) economic recovery, loan loss provisions should remain limited. This makes us still sanguine about bank profit growth through balance sheet expansion. We therefore stick to our earlier call for tighter spreads in the bank debt space and the recent spread widening already offers a buying opportunity. Investors might however want to wait until the post-summer new issuance in anticipation of higher new issue premiums, which could limit spread tightening in the very short-term. But this should not be long-lasting, given our base case of a cooling US economy will be confirmed by upcoming economic data. Tighter spreads should therefore be achievable by the end of Q3, also when the first US rate cuts have been implemented.

Non-regulated utilities struggle, but reversal already underway

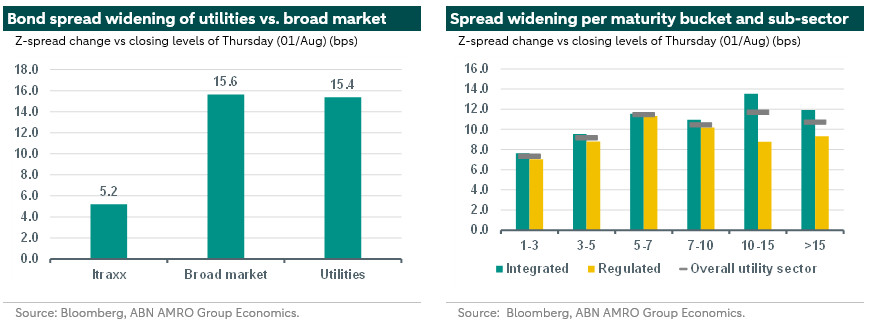

The sell-off was broadly everywhere, and utility bonds were therefore also not immune to it. However, given the still defensive nature of the sector, spreads widening were more or less in line with the broad market. This was also a trend seen in other defensive sectors, such as healthcare and food & beverage. As shown below, utility bond spreads widened as much as 15bps in comparison to Thursday closing levels – similar to the 16bps seen in the non-financial corporate universe. In terms of utility sub-sectors, most widening was concentrated within bonds of non-regulated (integrated) utilities, while regulated utilities actually outperformed the broad market, experiencing a widening of only around 9bps during the sell-off. This is in line with our previous analysis, where we show that regulated utility bonds tend to outperform once investors become more risk-averse. In terms of names, most spread widening was seen in names such as EON, Engie, EDF, Enel, as well as some regulated names such as Czech Gas Networks, Eurogrid and Amprion. Clearly, the bearish mood was concentrated in issuers exposed to countries that are more strongly hit by recession fears, such as Germany. Issuers that performed well during this period include: GAS Networks Ireland, REN and Vattenfall. In terms of bond maturities, most widening was concentrated on the 5-7y, as well as the 10-15y. Particularly for non-regulated bonds, there was a sharp bond spread widening in the longer part of the curve, ultimately increasing the curve steepness. The aggregate non-regulated utilities curve has now a pick-up of around 40bps against the aggregate regulated utilities curve in the 15y bond maturity, reversing some of the spread tightening we saw in the past couple of months.

That being said, and in line with our view that the sell-off was mostly a market overreaction, we see attractive opportunities for investors to step into non-regulated names at the longer part of the curve, and we would particularly focus on low-risk, low-volatility issuers in that space. In fact, non-regulated utility bond spreads have already been outperforming regulated peers since opening this morning.