What do we need to know about EU-ETS II?

EU-ETS 2 is a new separate cap and trade scheme that covers emissions from road transport, the built environment and industrial sectors that are not covered under EU-ETS. The system envisions a gradual phase in with emission reporting and monitoring starting in 2025 and 2027 as a first compliance year. It is important to analyse the impacts of EU-ETS II in combination with other climate policies to achieve an efficient transition.

EU-ETS 2 is a new separate cap and trade scheme that covers emissions from road transport, the built environment and industrial sectors that are not covered under EU-ETS

The system envisions a gradual phase in with emission reporting and monitoring starting in 2025 and 2027 as a first compliance year

A Social Climate Fund will be established to address any social implications of the new system on vulnerable end users. The fund will be financed mainly by auction revenues.

It is important to analyse the impacts of EU-ETS II in combination with other climate policies (regulation) to align incentives and achieve an efficient transition

Introduction

The European Union Emission Trading Scheme (EU-ETS) has been the EU flagship policy to reduce emissions in the power, aviation, and heavy industrial sectors. EU-ETS is a cap and trade system, where a cap is put on total allowed emissions in the covered sectors. The cap is further translated into emission allowances that can be traded in a market. EU-ETS has gone through reforms aiming at stronger emission reductions, extensions to cover emissions from maritime shipping, and establishing a new separate emission trading scheme to cover combustion emissions from road transport, industries not covered by the original EU ETS, and the built environment, which cover 34% of EU emissions, so called EU-ETS II. This note covers the main aspects of EU-ETS II such as the phase in process, associated mechanisms, and potential dynamics and impacts.

Gradual phasing in

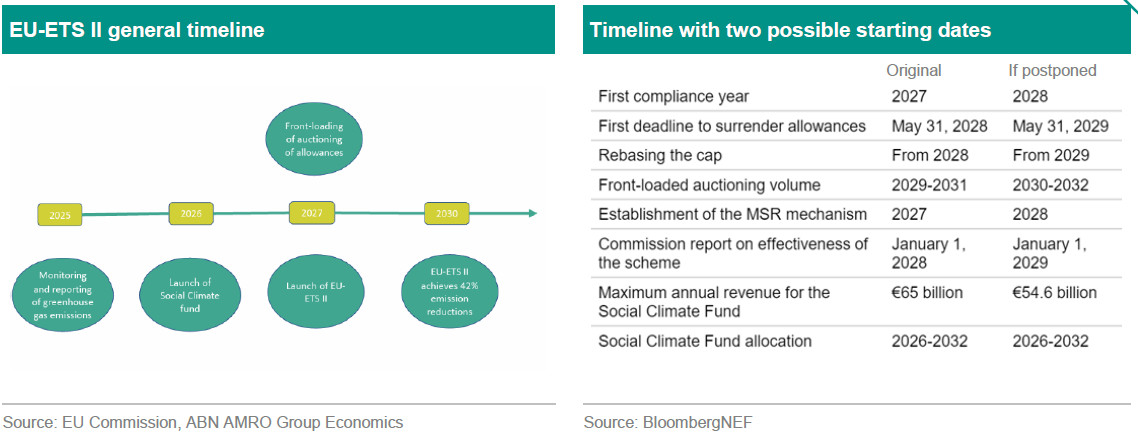

Currently, sectors that are not covered by EU-ETS are part of the Effort Sharing Regulation (ESR), which aims to collectively reduce member states’ emissions from these sectors by 40% in 2030 compared to 2005 levels. However, as part of the ‘fit for 55’ reform packages, and as of 2024, emissions from road transport and buildings will be regulated under a new separate emission trading scheme, known as EU-ETS II. Accordingly, 600 million allowances will be reallocated from the ESR mechanism towards the new EU-ETS II. Monitoring and reporting obligations for the new system will be in effect as of 2024, while the full operation is planned for 2027.

This gradual phase in of the new system, along with a less ambitious emission reduction target of 43% by 2030, compared to the 62% under EU-ETS, have been put in place with the aim of smoothing the transition for households and businesses. The cap will be set in 2027 along with the linear reduction factor to reach the 43% emission cuts in 2030.

Market Stability Reserve

The new system will have its own Market Stability Reserve (MSR), which aims at maintaining price stability by actively monitoring the supply of allowances. MSR will help avoiding excessive price fluctuations and maintain the balance between the supply and demand of allowances. Furthermore, the system will have a price cap of 45 euros, which will be valid until the end of 2029. The cap aims to limit the cost of the transition on households and other entities limiting the risks of a disorderly transition. The price cap will be maintained using the MSR.

Social Climate Fund

The social implications of the new system on vulnerable end users will be addressed by establishing a Social Climate Fund with a target of 65 billion euros of revenues raised through auctioning under the EU-ETS (50 million allowances) and EU-ETS II (150 million allowances) in the period of 2026-2032. Member states that already have a carbon tax or ETS for the road transport and building sectors in place can benefit from an exemption from the EU-ETS II until 2030 1).

EU-ETS II coverage

The EU-ETS II will cover CO2 emissions from fuel combustion for road transport, buildings, and industrial activities that are not covered by the original EU-ETS. All allowances will be auctioned, thus no free allocation. Regulated entities under EU-ETS II are those selling fuel for combustion to final consumers. These entities have to hold a permit by an assigned authority that is appointed by member states. At the end of the compliance deadline (31 May, starting from 2028), reporting entities have to surrender enough allowances to cover their emissions. Entities failing to cover their position will have to pay the carbon price augmented by a penalty for every additional uncovered ton of emissions.

Possibility of postponement

The EU-ETS II legislation incorporates the option to postpone the start of its implementation by one year if either the gas (TTF price) or oil (Brent) prices are deemed to be “exceptionally high” in comparison to historical levels. Accordingly, in July 2026 the commission will announce if the start date of EU-ETS II will be postponed or not.

EU-ETS II potential impacts

In practice, the effects of the new emission scheme on households and businesses will be reflected in higher fuel prices as regulated entities pass through the costs to consumers. Accordingly, any fluctuations in the new emission allowances price will be reflected in final consumer prices adding an additional volatility to these prices. However, the price cap for the first few years will limit these effects.

With regards to the effect of the system on the transition, if clean technological alternatives are not readily affordable to all income classes, the cost of the new scheme will hit the poor hard. For example, in the absence of an affordable second hand market for electric vehicles, many households could find themselves suffering from a high fuel prices, along with a drastic value loss of their fossil cars with an inability to switch to an electric alternative. Which induce a lock-in effect in old fossil technologies. In such cases, intervention is essential by using the social climate fund to limit and compensate financial losses, while facilitating the availability of affordable alternatives. However, time is of great importance here, thus intervention should be proactive with clear and timely agenda to avoid additional transition costs.

One thing to highlight is that the new EU-ETS II will be working in parallel to other climate policies, such as regulation in the built environment. Thus, it is of a high importance for the government to analyse the impacts of the combination of these policies, and make adjustments when needed to align incentives and achieve an efficient transition.

1) The allowances that would have been auctioned for these members will be cancelled.

This article is part of the SustainaWeekly of 30 October 2023