US Watch - Robust Q3 growth driven by strong consumption

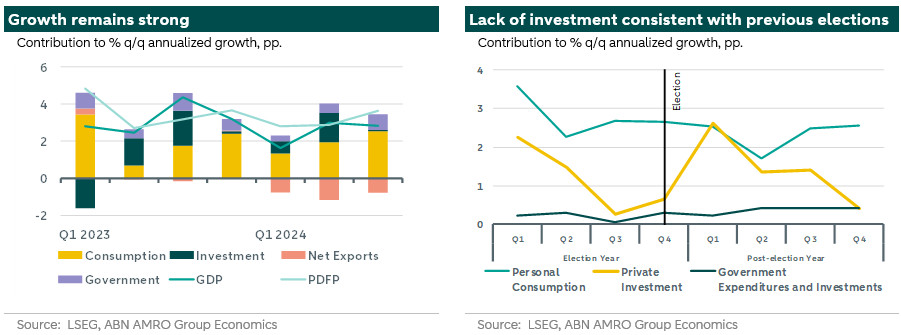

The US economy continues its trajectory of solid expansion, with Q3 GDP growth coming in as expected at an annualized 2.8% (2.9% consensus). Growth was predominantly supported by strong consumption (3.7%, 3.3% consensus), and government spending (5.0%). Investment grinded to a halt, consistent with previous election cycles (1). Net exports subtracted 0.6%. Private domestic final purchases (PDFP), which excludes inventory investment, government spending and net exports, and sends a clearer signal of underlying demand, came in strong at 3.5% annualized, the highest in a year.

Consumption growth was broad based, with an uptick in goods consumption, particularly in non-durables, with a larger role for healthcare in the form of prescription drugs. Services consumption growth came in similar to last quarter, with a strong contribution from healthcare consumption, led by outpatient services. Food services contributed strongly and saw a large acceleration relative to last quarter.

Investment was a combination of a decline of 5.1% in residential investment - with the housing market struggling to deal with high mortgage rates and prices – and a weak 3.3% non-residential investment gain, dragged down by spending on structures. Spending on equipment, on the other hand, was the strongest in more than a year. Government spending rose on the back of national defense expenditures, which grew by 14.9%, the most since 2003. Excluding defense spending, federal government spending still grew at the strongest pace in a year.

Going forward, Q4 and 2025 are likely to show a slowdown compared to the robust growth this year, on the back of still restrictive monetary policy doing its work, and the dampening effects of economic policy and geopolitical uncertainty, which may or may not be partially resolved after next week’s election. For now, the economy is on track to beat the Fed’s 2.0% projection for the year. At the same time, inflation readings and labor market data are expected to give the Fed enough reason to continue to gradually reduce the policy rate in the coming period, including a 25 bps cut at the meeting next week.