US inflation still alarmingly high

Inflation surprised once again to the upside in January, with both headline and core CPI up 0.6% m/m (consensus/ABN: 0.5% for core inflation, 0.4%/0.3% for headline). This took annual headline inflation to 7.5% y/y, and core inflation up to 6.0%. While yet another set of alarming numbers, the details provided some comfort – the upside surprise was entirely driven by energy (+0.9% m/m), food (+0.9%) and goods (+1.0%) prices, with core services inflation coming in line with our forecast at a still-elevated 0.4% m/m.

On the back of January's report and an upward revision to our oil price forecasts, we have raised our CPI inflation forecast for 2022 once again to 5.0%, up from 4.6% previously. We have also made a smaller upgrade to our forecasts for core CPI (to 4.7% from 4.5%) and core PCE (to 4.2% from 4.1%). We continue to expect much lower rates of inflation in 2023, albeit staying somewhat above the Fed’s 2% target on core measures (core CPI: 2.6%; core PCE: 2.4%).

Labour market will be key for the outlook

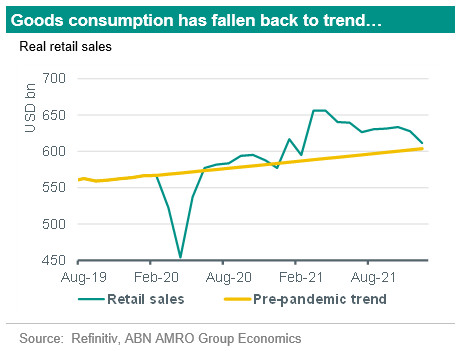

Looking ahead, there are some encouraging signs that goods inflation will start to fall back. One of the main drivers – used car prices – is starting to come down again at the wholesale level, and the sharp drop-off in car demand suggests this will continue – we estimate auto sales fell to around 3% below the pre-pandemic trend in December, the first below-trend reading since the start of the pandemic. Similar trends, albeit to a lesser degree, are visible broadly in goods consumption. Given the excess in consumption that we have seen (some of which has likely been brought forward from the future), the risk is that demand here cools even further. This, combined with the expected modest easing in supply bottlenecks, means core goods is likely to become a drag on inflation from Q2 onwards.

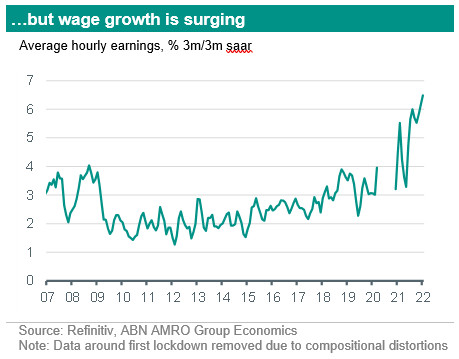

This will leave the major upside risk to the inflation outlook emanating from the labour market. Last Friday’s payrolls report showed wage growth continuing to accelerate, with hourly earnings up 6.5% on a 3m/3m annualised basis – around double the pre-pandemic pace of wage growth. We currently take the view that this is being driven partly by short term frictions in the labour market, such as from the decline in participation (which, on a positive note, has recovered somewhat more than expected). However, the longer that elevated inflation and wage growth persist, the bigger the risk that expectations become entrenched at a higher level, requiring a more forceful policy response (and a higher unemployment rate) to bring back down.

Fed base case unchanged; risk still tilted to more hikes

Our base case continues to be for the Fed to raise rates four times this year, with the first hike coming in March. Given the continued upside inflation and labour market surprises, however, the risk of a more aggressive Fed response has grown further. We think current market expectations for a 50bp rate hike in March look excessive, but see a much bigger risk of consecutive 25bp rate hikes at each FOMC meeting once lift-off begins in March. For more, see our , where we sketch out a more aggressive scenario for interest rate rises.