Update on our Fed and ECB views

We have made some changes to our Fed and (more modestly) ECB views. In this note, we set out the changes as well as the implications for our rates forecasts. The first Fed cut is now seen in September, with a slower pace of rate cuts initially. We have removed a July ECB rate cut from our base case, but see rate cuts at each meeting after that. Bond yields have been revised higher, but they are still seen dropping, with curves steepening.

Co-author: Sonia Renoult

Fed to start rate cut cycle in September

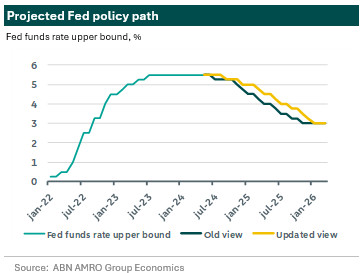

We now expect the Fed to delay the first rate cut to September (previously July), with one more cut this year in December following a pause in November. This entails a total of two 25bp cuts in 2024 (previously three). We expect the Fed to remain cautious and ease gradually until the first quarter of 2025, with only one 25bp cut in March. After this, we expect cuts at every FOMC meeting, until reaching our estimated neutral level of 3% in the upper bound of the fed funds rate, in January 2026. The update to our view is a combination of a delay of the rate path by one meeting, and a single additional pause in January. The slower pace should allow Fed officials to obtain greater confidence that inflation is on track to meet its target in the course of 2025. The timing of our update may seem odd, as April data released over the past month finally showed some sign of waning inflationary pressures. There are two reasons for our change of view. The first is the fact that the April inflation figures were still substantially elevated, with even core PCE coming in at 3% annualized. The second is the generally hawkish communication by Fed officials since the last FOMC meeting, which has made it clear that inflation readings need to come in substantially lower for an extended period of time for the Fed to start cutting rates.

US inflation will come down, eventually

Despite an apparent improvement in the inflation figures for April, they are still far from consistent with a 2% y/y inflation rate. Headline and core CPI inflation, as well as headline PCE inflation, came in at 0.3% m/m, while core PCE provided the first 0.2% m/m increase of the year. However, even the lowest of the inflation rates, core PCE, annualizes to 3.0%, as the unrounded figure was 0.249%. Indeed, the analysis of inflation is currently a second or third decimal exercise, which is a key indication that inflation is not yet where it should be. We believe the Fed needs to see a sequence of readings closer to 0.20% before gaining the confidence to cut. As summarized by Governor Waller: ‘(…) I look forward to the day when I don’t have to go out two or three decimal places (…) to find the good news.’ By the July meeting, we will only get two more inflation readings, which will likely not be sufficient to give that confidence, even if the outcomes are benign. By September, however, the Fed will have seen four more CPI and three additional PCE readings. We project these upcoming readings to come in lower than the April figure, and this should then provide the needed confidence to cut. The more hawkish Fed communication is part of the natural discourse. Disagreement within the board is not new, and officials use the media to try and steer the debate towards their view. Chair Powel’s press conference performance and later appearances were on the more dovish side of the spectrum, while the most hawkish officials, such as Governor Bowman, have advocated for no cuts this year. We do not think the latter to be a likely outcome, but even the most dovish officials have said they need more confidence in the face of uncertainty following the first quarter inflation readings. The Fed has the time to obtain such confidence in light of the generally resilient state of the economy. In light of the above, we judge that, once they do gain that confidence that inflation will reach its target, they can cut with equal confidence. As a result, the Fed eases more quickly in 2025 in our baseline projection compared to both market pricing and consensus. Indeed, our medium-term inflation outlook has not changed. Pipeline pressures such as wage growth and market rents remain benign, and we expect the disinflation process to continue, with the Fed’s target PCE inflation ultimately reaching 2% y/y in the course of 2025.

First signs of a slow-down of the US economy?

What about the recent softer growth and labour market data? GDP growth for Q1 was revised downward to 1.3% (from 1.6%), primarily due to a revision in consumption. Indeed, personal spending since fell by 0.1% in real terms in April. However, the Q1 growth weakness can still largely be attributed to net imports, and underlying indicators of demand were still strong, with gross domestic purchases increasing by 3.0% q/q. Activity indicators like the manufacturing PMI and ISM provided a similarly mixed signal, with the services PMI even pointing to an acceleration in activity. Putting these numbers in a greater context, one should be careful to draw too strong conclusions from a single month of data. Additional releases coming in the next month should start to clarify the extent of a potential slowdown. Second, slowing growth is consistent with our base case for the US economy of modestly below trend growth, which actually would be a rather welcome outcome. Indeed, it is a feature of restrictive of monetary policy, not a bug. The Fed is attempting to orchestrate that rare soft landing, but to land the plane must come down.

ECB pause in July, but ongoing rate cuts from September

Turning to the ECB, we no longer expect a follow up rate reduction in July, following the Governing Council communication and recent data. At yesterday’s meeting, the Council refrained from giving any guidance about what happens next in its official statement (see our note here). However, in the Q&A, President Lagarde hinted that a signal on a future move would come only after the July meeting. This already followed more cautious official rhetoric in the weeks leading up to the meeting. At the same time, the latest inflation data also seemed to support a wait-and-see approach, with services inflation (one gauge of domestic inflationary pressures) re-accelerating. Nevertheless, looking forward, we expect disinflation to resume. First of all, the second round effects on the core rate from the past fall in energy price inflation still have some way to go. Second, leading indicators of wage growth point to a significant decline going forward. At the same time, as Ms Lagarde made clear in the press conference, policy rate are far above a neutral level. There is some debate about exactly where neutral is. Our estimates are on the lower end of ranges, reflecting trends in demographics and productivity, evidence that rate hikes credit demand hard and the upcoming consolidation implied by the new fiscal rules. We expect the next rate cut at the September monetary policy meeting and at a 25bp pace at subsequent meetings, until rates reach 1.5% during the course of next year.

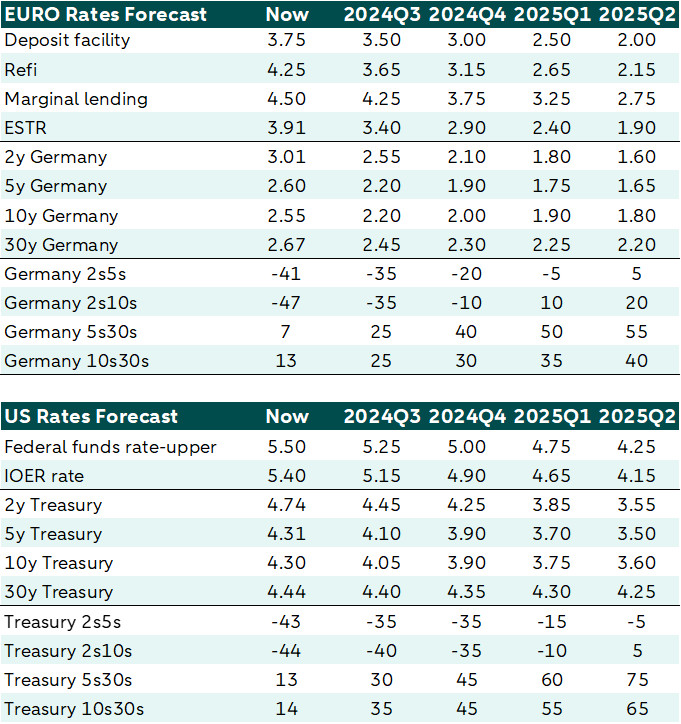

Upward revisions to bond yield forecasts, but direction still lower

Following the changes from our Fed and ECB view, we have revised our forecasts for both US Treasury yields and Bund yields higher. As shown in the table below, the main changes were skewed to the front-end of the yield curve (the 2y and 5y bond yields) as those rates are more anchored to the near term monetary policy path than longer bond maturities. The revision reflects that we now have 50bp less Fed rate cuts than previously and one pause in July for the ECB. As a consequence, the shape of the curve is now expected to steepen to a lesser extent and at a later stage also in the US. Thus, we expect a slight decoupling in the short-term between the US Treasury and Bund yield until the Fed catches up the ECB on the rate cut cycle later in the year. This means that we expect the decline in rates to be bigger in the Euro area with steeper curves while the US Treasury curve is expected to slowly dis-invert with the 2s10s spread turning positive only as we move into 2025.

Although the main changes are skewed to the front-end of the curve, we still expect long-term rates to fall going forward. Now that the ECB started its rate cut cycle (and Fed expected to follow suit) the main question will be on its terminal rate. In our view, the market still has to adjust its estimate of the terminal rate lower for both the Fed and ECB as it is likely well above the respective neutral rates. As mentioned above, we forecast a neutral rate of 3% for the Fed (vs 3.7% by the market) and 1.5% for the ECB (vs 2.5% by the market). Moderate outcomes in activity data and disinflation should be the trigger for market to revise its terminal rate lower in our view.