UK: Fiscal splurge to drive a further jump in interest rates

The new Truss government published details of its not-so-‘mini’ Budget this morning, which – alongside a generous support package capping household and business energy bills – came with an array of tax cuts in an attempt to stimulate the economy onto a higher growth path. We judge that the package merely delays the pain of economic adjustment that is necessary rather than avoids it, with the Bank of England likely to hike rates more to offset the demand impulse.

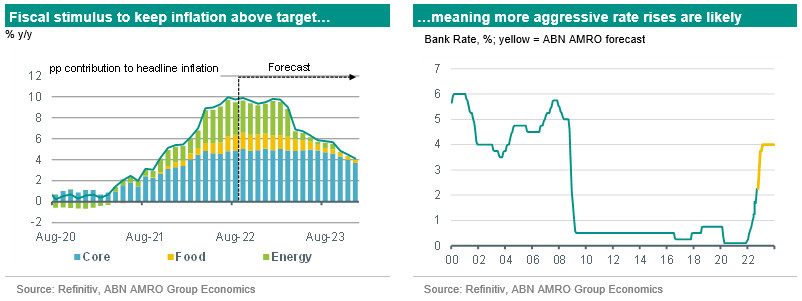

Both the support for energy bills and the tax cuts are entirely unfunded, meaning there will be a dramatic widening of the deficit next year, and it is also likely to put UK public debt on an unsustainable path. Just how much of a negative impact it has on government finances will depend significantly on gas prices; the combined fiscal impact could be anywhere from 3-5% of GDP for next year. Either way, it is an extraordinarily large fiscal impulse coming at a time of a constrained supply side, very high inflation and rising interest rates. The fiscal package does mean the UK is now likely to avoid a deep recession next year, and we have raised our 2023 growth forecast to -0.1% from -0.8% previously. The freeze in household energy bills will mean somewhat lower inflation in the near-term, but we now expect above-target inflation to persist well beyond 2023, meaning that the Bank of England will need to keep interest rates at a sufficiently high level to dampen demand for longer. Financial markets have reacted negatively to the budget announcement, with bond yields surging, and sterling weakening. Money markets also significantly raised expectations for interest rate hikes by the Bank of England, with Bank Rate now priced to reach 5.3% by August next year, up from 4.9% yesterday.

Bank of England hikes 50bp, with more aggressive moves to come

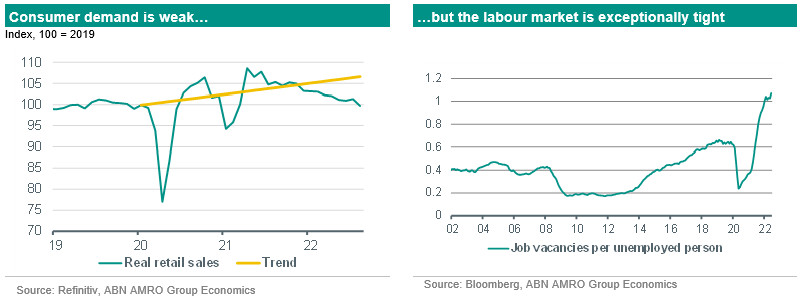

Ahead of today’s budget announcement, the Bank of England raised its policy rate by 50bp to 2.25% on Thursday, in line with our and consensus expectations, but disappointing some forecasters and market participants who anticipated a larger 75bp step. The vote split suggested a continued divide among MPC members, with 5 members (including Governor Bailey) voting for a 50bp hike, 3 voting for a 75bp move, and 1 voting for a smaller 25bp step. The highly unusual degree of division on the MPC reflects the conflicting signals over the outlook for the UK economy. On the one hand, demand is clearly depressed and has weakened further over the past few months – evident in falling real retail sales that are well below trend – but this contrasts with a continued ultra tight labour market, and increasing signs that elevated inflation is sparking a wage-price spiral (see here for more). While the BoE opted for a 50bp hike at this meeting, the new measures announced by the incoming Truss government to freeze household energy bills and to cut taxes would “all else equal (…) add to inflationary pressures in the medium term,” according to the policy statement. The MPC stated that the implications of the new fiscal plans for the outlook and therefore for monetary policy would be fully assessed ahead of the next BoE meeting on 3 November (coincidentally, the Bank will also then release updated growth and inflation projections in its quarterly Monetary Policy Report).

We now expect rates to reach 4% by early next year, with upside risks

Broadly, the fiscal plans will dampen near-term headline inflation and raise GDP forecasts – meaning that the projected recession we expect will be shallower than previously thought – but essentially they will merely delay the pain about to hit the UK economy rather than prevent it entirely. This is because, as the MPC notes, the stimulus to demand raises medium-term upside risks to inflation. The demand impulse from this stimulus will be coming just when the Bank of England is trying to push in precisely the opposite direction by raising rates to dampen demand. We think therefore that the MPC will be forced to offset the demand stimulus of the government by raising Bank Rate more aggressively than we previously expected, and our new base case is that the MPC raises rates by 75bp at the November and December meetings, with a further 25bp move in February – taking Bank Rate to 4% (previously 3%). The risks to this forecast are likely to be to the upside, as fiscal stimulus is likely to add further to labour market pressures in the near-term, and so the MPC may not wish to take its chances given that the pain later on might be considerably greater if it reacts too slowly.