UK - In the early stages of a wage-price spiral

The real income shock is pushing the economy into a recession that is likely to persist into 2023. Inflationary pressures have intensified, with the economy looking to be in the early stages of a wage-price spiral. As such, we now expect the BoE to hike rates by 50bp at the coming two meetings.

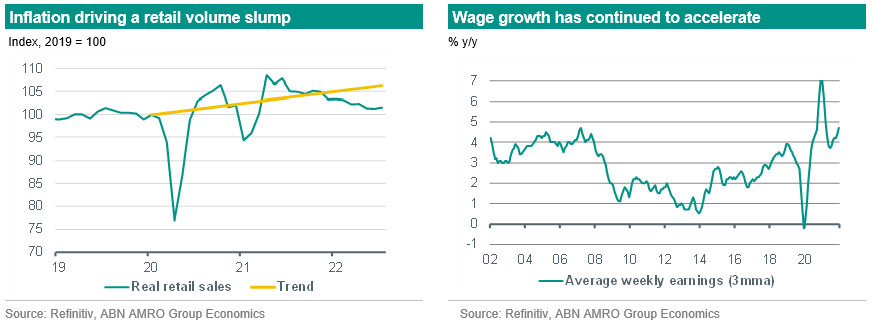

The economy performed marginally better than expected in Q2, as weakness in private and government consumption was offset by a continued strong inventory buildout. However, the economy still contracted by 0.1% overall, and we expect that contraction to continue over the next few quarters. While some rebound in private consumption is likely in Q3, on the back of the post-pandemic summer travel surge, in other respects demand continues to weaken on the back of the inflation shock to real incomes, and this is likely to lead to much lower levels of inventory accumulation – with outright declines likely later this year and into 2023. The inflation shock is expected to intensify, with Ofgem’s 80% announced rise in the energy price cap pushing inflation more firmly into double-digit territory when the cap is officially raised in October (as of July, inflation had reached 10.1%). Ofgem is shifting to a 3 month cycle for its energy price cap changes, with the next move therefore due in January (previously, the cap was adjusted every 6 months). Given the most recent surge in wholesale gas and electricity prices, we expect inflation to see another lift in early 2023 – and ultimately for it to peak at over 13%. Similar to the eurozone, we expect the inflation hit to real incomes and the burden of astronomical energy prices on business to drive a deep recession in the UK, with a contraction of -0.9% now expected in 2023.

The announcement of the new Prime Minister on 5 September is unlikely to help. Current opinion polling suggests foreign secretary Liz Truss is likely to comfortably win the Conservative Party leadership contest against former chancellor Rishi Sunak. Her stated policy is to implement a raft of tax cuts upon becoming PM, providing stimulus to the economy just when the Bank of England is trying to push in the opposite direction by raising rates to dampen demand. Indeed, the ultra-tight labour market has led to a further pickup in wage growth recently, with the UK now seemingly in the early stages of a wage-price spiral, as higher wage pressures push companies to pass on higher costs evident in the rise in core inflation. Tax cuts would add fuel to the inflationary fire, and while they might make the expected recession in the UK more shallow than otherwise, they will not help the economy avoid a recession entirely (see this month’s Global View for more).

As a result of the worsening inflation situation, and the increasing role that the labour market is playing, we now expect the Bank of England to hike its policy rate by another 50bp when it next meets on 17 September – taking Bank Rate to 2.25%. Subsequently, we expect another 50bp hike in November, followed by a final 25bp hike in December. As such, we now expect Bank Rate to peak at 3% by the end of this year, compared with our previous expectation of 2.5%. Our new forecast is still well below market pricing, which foresees rates rising above 4% by early next year. Our view assumes the BoE’s own longer term projections are realised, as these suggest such a sustained high level of interest rates would lead to an even deeper recession than we currently forecast, with inflation significantly undershooting the Bank’s 2% inflation target by 2024. With this in mind, we continue to think the Bank will start cutting rates back again late next year, assuming that inflation and labour market tightness have sufficiently cooled at that point.