The Netherlands - Economy in a technical recession

The Dutch economy contracted by 0.3% qoq in Q2 and by 0.4% in Q1. We expect yearly growth to slow down from 4.5% in 2022 to 0.5% in 2023, and to 1.1% in 2024. Inflation is declining, but underlying price pressures remain firm.

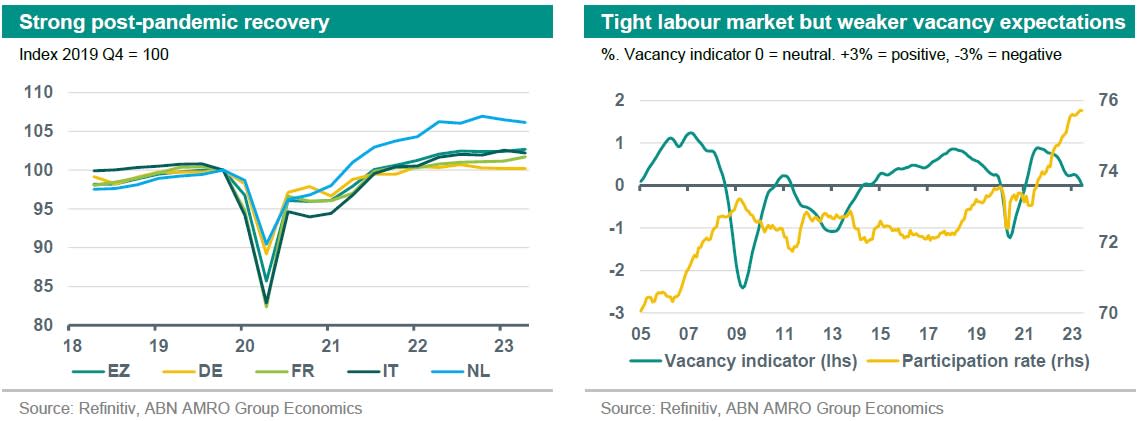

The Dutch economy contracted by 0.3% qoq in Q2. As GDP had already contracted by 0.4% qoq in Q1, the Netherlands was in a technical recession during the first half of the year. Eurozone GDP expanded by 0.3% qoq in Q2, which means that the Dutch economy underperformed the eurozone aggregate. Still, in level terms, the Dutch economy has significantly outperformed the eurozone aggregate in the post-pandemic period (see graph below).

The contraction in Q2 was driven by the trade balance and private consumption. Weak external demand – particularly for (chemical) industrial goods – caused total exports to contract while imports grew. This resulted in a negative contribution from the trade balance to GDP. As the growth outlook for the eurozone remains subdued, the trend of weak demand for Dutch exports will most likely remain in place for the remainder of the year. Meanwhile, inflation has weighed on private consumption, causing it to contract by 0.2% qoq in Q1, with a much bigger fall of 1.6% in Q2. Although goods consumption contracted, services spending prevented a bigger drop in overall consumption. Some services sectors might still benefit from post-pandemic catch-up spending. We expect consumption to grow modestly over the rest of the year, as household spending is supported by a still exceptionally tight labour market, accelerating wage growth, and government support such as the energy allowance and the (energy) price ceiling.

Despite weak growth prospects and higher financing costs, fixed investment stood out, expanding by 1.3% qoq in Q2. The strength in investment was driven by infrastructure investment, transport and machinery, and sustainability related investment such as insulation, solar panels and heat pumps. Housing investment, by contrast, contracted on the back of the cooling housing market.

Despite the technical recession, the Dutch economy remains resilient; the labour market is still tight and bankruptcies – although increasing in recent months – are still below 2019 levels. Still, we expect growth to remain sluggish in the coming quarters. We have slightly adjusted our growth forecasts from 0.7% to 0.5% for 2023, and from 1% to 1.1% for 2024

Inflation is on a downward trend. It fell to 5.3% in July, down from an annual average of 11.6% in 2022. Core inflation has remained more elevated and stood at 7.2% in July. Inflation is expected to come down further over the coming year and to average 4.8% in 2023, and 3.5% in 2024. As such, inflation is unlikely to return to 2% any time soon. Wage growth is likely to remain historically elevated, as workers seek to make up for past declines in real wages amid a very tight labour market (see graph). This is expected to last at least until the end of next year, putting upward pressure on labour-intensive services and goods. As the Dutch economy continues to have a positive output gap, the risk is that inflation remains well above the eurozone total for a considerable period. Some cooling of the economy, particularly domestic demand – as seen in the latest GDP figures – is therefore welcome.

This article is part of the Global Monthly of August 23