The Netherlands - A story of domestic demand

First quarter GDP showed an unexpected contraction by 0.1% q/q. We have revised our growth forecasts to 0.5% (was 0.7%) in 2024 and 1.3% (was 1.2%) in 2025. Growth will be driven by internal demand. Later in 2024, as financial conditions ease and external demand increases, growth is set to normalize further. The coalition parties came to an agreement, with spending shifting away from longer term investments towards short-term spending and purchasing power increases.

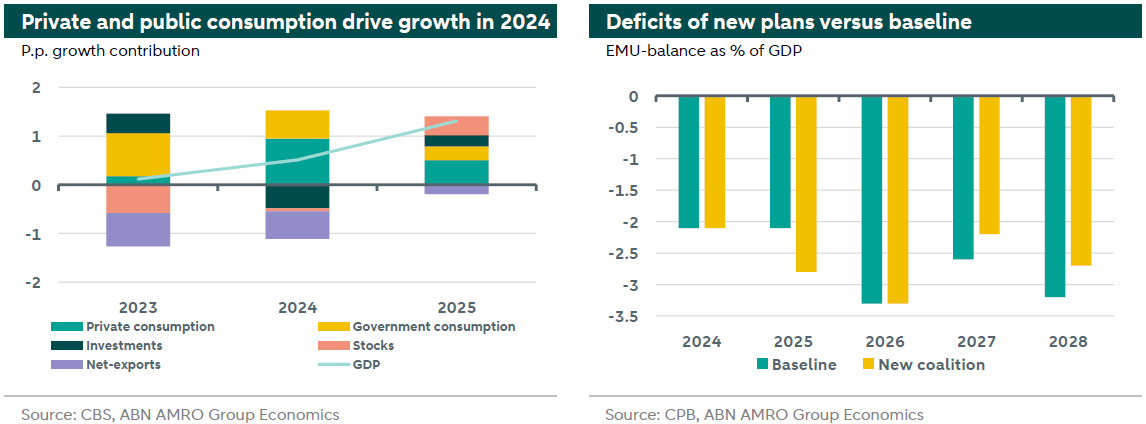

The Dutch economy unexpectedly contracted by 0.1% q/q in Q1 (ABN: +0.2%, consensus +0.3%). This contraction contrasts with figures from neighbouring countries. The German economy grew by 0.2% q/q and the eurozone as a whole grew by 0.3% q/q. The contraction in the Netherlands was largely driven by a decline in net exports and further stock depletion. Goods exports contracted (-1.3% q/q), while services exports grew (+4.7% q/q). The contraction in goods exports was driven by weakness in the manufacturing sector. The sharp decline in inventories also hurt growth, but the cycle of stock depletion seems to be reaching its end, in line with the of the industrial sector.

Despite the downside surprise, the published figures support our view of the 2024 growth outlook, as the domestic subcomponents did increase on a quarterly basis. For instance, private consumption rose by 0.7% q/q as households benefited from a recovery in real incomes on the back of further declining inflation and strong wage growth. Government consumption also increased by 0.6% q/q. Despite formation talks, the caretaker government continues to contribute to growth through spending on healthcare, education and defence. Finally, investments surprised to the upside, growing 0.4% q/q, even though weak growth prospects and high interest rates limit the rationale for investments. Indeed, investments mainly increased due to replacement investments, for instance in transportation and machinery, and not due to capacity-increasing investments.

Looking forward, the outlook for 2024 remains positive but weak. Growth will be driven by domestic demand, both from households and the government. Later in 2024, as financial conditions ease and external demand increases, growth will pick up further. Taking into account the Q1 realisations we have revised our growth forecasts to 0.5% in 2024 (was 0.7%) and 1.3% for 2025 (was 1.2%), up from 0.1% in 2023.

The coalition parties reached an agreement (read more ), with limited macroeconomic effects. The plans focus on curtailing migration, lower taxation, the business climate, the agricultural sector and housing construction. The plans are expected to marginally increase economic growth in de short-term, mostly through consumption and investment. Consumption benefits from increased real incomes by measures such as lower income taxes, the extended decrease of fuel taxes, and higher rental allowances. Investment is for instance increased through higher housing investments, as the coalition prioritises new housing sites. The coalition parties plan to shift spending away from longer term investments and goals (such as climate) towards more short-term goals, which increases the budget deficit compared to the baseline in 2025 and 2026. The agreement states spending will be cut in 2027 and 2028, but we argue that these spending cuts are uncertain and unlikely to succeed, which puts upward pressure on the deficit in those years.