SustainaWeekly - Limits to international issuance by eurozone green heavyweights

In this edition of the SustainaWeekly, we first look at the current dynamics in bond yields amongst EUR and USD for corporate EUR IG ESG bond issuers to see if direct funding in their overseas markets is cheap. In particular, issuers can choose to either issue at the domestic level and swap the proceeds to a foreign currency or issue directly in the foreign bond market. We find that the pricing differential between issuing in foreign currency or swapping domestic issuance to the foreign currency, despite the cross-currency basis, is large at this stage and would therefore limit international issuance by eurozone green bond heavyweights. We go on to analyse the European Commission’s latest electricity reform proposals, which focus on encouraging the availability and use of long term pricing solutions. Finally, we assess the viability of the EU’s goal to produce at least 40% of clean technologies in the EU by 2030.

Strategy: The large European ESG debt issuers have international operations and we assess if direct funding in their overseas markets is cheap. Despite the existence of a cross-currency basis, we show that large European utility issuers pay-up considerably when issuing directly in USD markets. The large US real estate green bond issuers also benefit when issuing locally and using cross-currency swaps for their EUR funding needs. Economist: The European Commission’s latest electricity reform proposals address a key weaknesses in the design of the existing wholesale energy markets by encouraging the availability and use of long term pricing solutions. Long term pricing contracts will protect consumers, support investment and bear down on funding costs. However, these benefits will occur over time and as such they will not provide consumers immediate relief. Sector: The EU’s goal is to produce at least 40% of clean technologies in the EU by 2030. The 'Green Deal Industrial Plan' is about maintaining competitiveness of the EU cleantech sector, energy independence in general and to foster a faster transition to climate neutrality. The additional investments from the 'Green Deal Industrial Plan' are positive for the cleantech sector. The plan helps to remove current obstacles to the sector.ESG in figures: In a regular section of our weekly, we present a chart book on some of the key indicators for ESG financing and the energy transition.

EUR green bond issuers not stealing the limelight in other currencies

The large European ESG debt issuers have international operations and we assess if direct funding in their overseas markets is cheap

Despite the existence of a cross-currency basis, we show that large European utility issuers pay-up considerably when issuing directly in USD markets

The large US real estate green bond issuers also benefit when issuing locally and using cross-currency swaps for their EUR funding needs

In this note we look at the current dynamics in bond yields amongst EUR and USD for corporate EUR IG ESG bond issuers. We focus on the two largest sectors in the corporate green bond market, being utilities and real estate, given large investment requirements in this space, also at an international level. Issuers can choose to either issue at the domestic level and swap the proceeds to a foreign currency or issue directly in the foreign bond market. Issuing in the foreign market and thereby expanding the investor base could be beneficial for the issuer, especially should they have large and recurrent capex intentions outside of the eurozone such as the installation of windfarms in the US or buying/constructing energy efficient properties in the UK. Unfortunately, the pricing differential between issuing in foreign currency or swapping domestic issuance to the foreign currency, despite the cross-currency basis, is large at this stage and would therefore limit international issuance by eurozone green bond heavyweights.

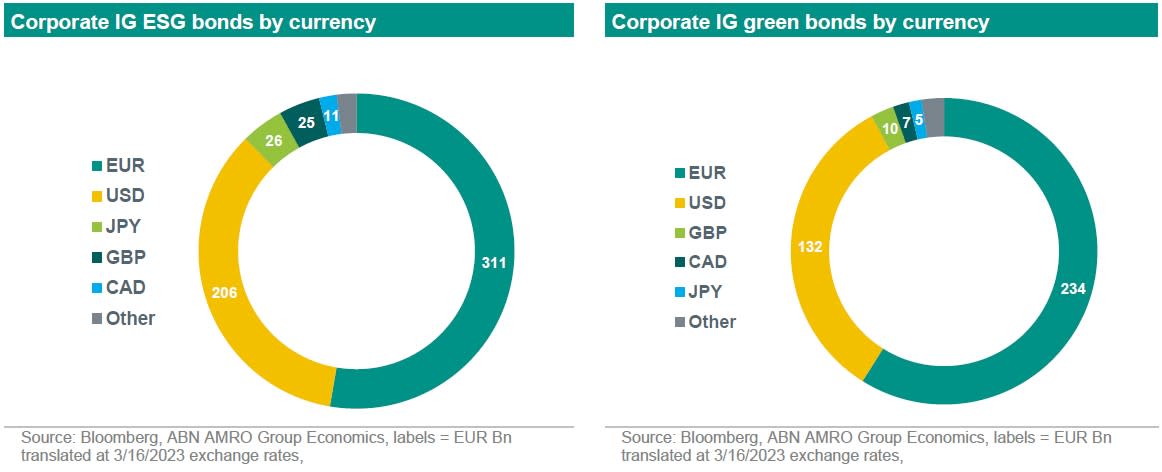

EUR currency dominates in corporate ESG bonds issuance

In 2007, it was the EIB which printed the first ever green bond, and this was in EUR currency. Since then there has been a great deal of issuance but also currency diversification across the ESG bond space, but the EUR currency continues to dominate the ESG bond market as can be seen in the charts below.

Issuers have managed to grow their international presence and in 2021, Enel and Iberdrola for example generated 42% and 49% respectively of electricity in countries outside of the European Union. Still, the level of foreign currency debt at these issuers according to Bloomberg DDIS data is limited to 8% and 6%, respectively. Iberdrola (including Avangrid) has 14% foreign currency public ESG bonds, while at Enel 38% of their ESG bonds are in USD denomination.

If only the cross-currency basis would be higher

As we mentioned in the introduction, in order for euro-based issuers to obtain foreign currency funding they could either issue directly in the foreign market or issue locally and revert to their banks in arranging a cross-currency swap (CCS). Under a CCS the issuer and swap dealer bank exchange principal and coupons for the desired length of the contract. An issuer would then, after switching principle amounts, at the start of such a swap receive a EUR coupon (which they can match against the EUR coupon payment on the actual bond) and in turn pays a USD coupon. This nets out in paying only a USD coupon and normally the interest rate to be paid on the USD leg would be driven by forward exchange rates and the existing EUR interest rate. But cross-currency swap markets are constrained by the cross-currency basis, which in the case of the EUR to USD swap reflects an additional payment made by the issuer because of a supply/demand imbalance in EUR vs USD. For example, today’s fiercer tightening cycle by the Fed compared to the ECB creates less USD liquidity in markets and this supply imbalance is reflected in a higher basis, which the issuer needs to pay. Indeed, since the Fed started with rate hikes since March 2022, the short-term USD/EUR cross-currency basis has outgrown the basis in longer dated tenors, implying that this extra-cost is most penalizing in the short-end (readers should actually interpret the negative basis as what needs to be added to the USD coupon when EUR issuers want to swap to USD). Furthermore, as we do not expect the ECB peak rate to be as high as that of the Fed, this basis should remain in place.

Still, paying an additional 30bp does not look like a lot of additional charge, especially given the much wider yield differences noted between USD and cross-currency swapped EUR to USD bonds, as we show in the next paragraph.

USD bond market prefers local utility companies

The issue that large European ESG bond issuers have when printing bonds in the USD market seems to be their unfavourable debt metrics. The chart on the next page shows the Bloomberg BVAL bid yield curves on two yankee issuers, Enel and EDF, against similarly-BBB1-rated US domestic issuers Appalachia Power Co and Nextera. All these issuers have a mix of generation and regulated activities as well, enhancing the comparison. Most striking is the high yield being commanded on Enel debt in USD market, despite it offering mainly SLBs. EDF’s weak metrics mainly hurt in the very long-end. US investors also seem less bothered on Appalachia scoring horribly on the environmental front and clearly draw comfort from both Appalachia’s as well as Nextera’s better debt metrics (in this case expressed as Moody’s latest adjusted RCF/Debt levels).

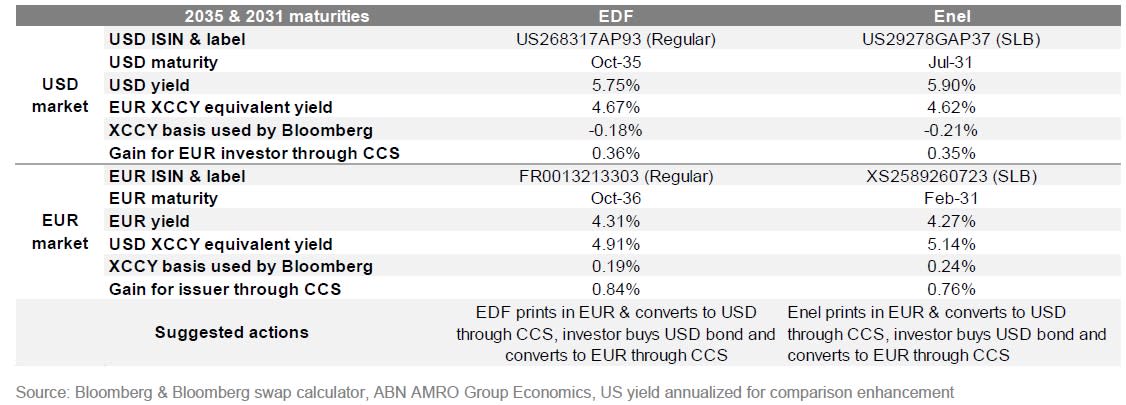

These European ESG bond issuers are on the backfoot and the below table compares how much they are quoted for a placement in the USD market (by looking at secondary pricing) against what a similar EUR maturity would cost them after swapping to USD through a cross-currency swap.

Clearly the issuers gain close to 0.8% through swapping a EUR deal into USD versus issuing directly in the US market, and clearly the cross-currency basis is not large enough to act as a drag. On the flipside, investors are better off by purchasing the dollar tranches and swapping them back to EUR. At EDF we calculate a 0.7% saving for the issuer on a hypothetical 2025 maturity, while the outstanding USD tranche in this case was a green bond and the green label could have narrowed the gap to print directly in USD.

While the large yield in direct USD issuance could be explained by the EUR issuer’s weaker financial profile versus US peers, we also see such a disadvantage of the EUR names when they want to print in the GBP space. EDF, Enel but also National Grid and Orsted would be better off printing (ESG) bonds in EUR and then swapping to GBP instead of issuing directly in the GBP market. The universe of names seems rather similar in the GBP space, hence it could also be that the still beneficial effects of the ECB’s much larger corporate security purchase program are still having desirable effects despite the ECB having halted net purchases a long time ago.

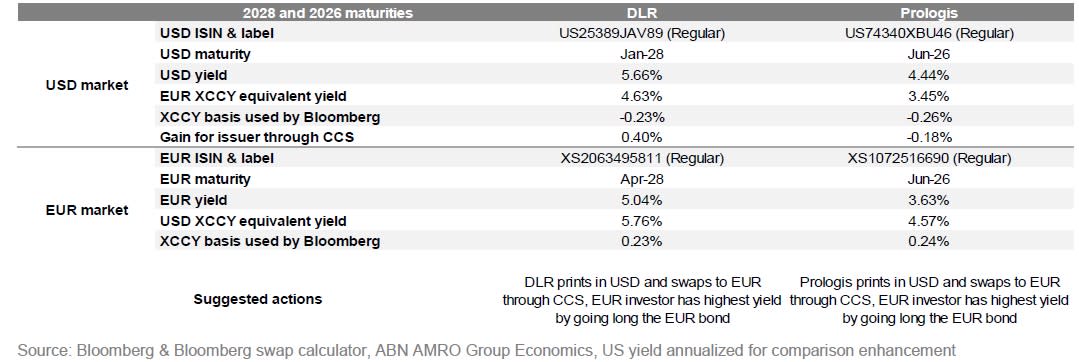

US real estate green bond issuers should stick to local markets

The real estate ESG bond space is less internationally focussed. Still, we note that US names such as DLR and Prologis have tapped the EUR ESG bond market for funding, also because they have a sizeable part of their assets in Europe. Still, current market dynamics prescribe that an approach of these issuers staying in USD and swapping to EUR works much better. While DLR does not have green bonds outstanding in the USD space, we note that a greenium is visible on the secondary USD bonds of Prologis, which could make the benefits even larger if this greenium would be applied in the USD primary market as well. US investors clearly like DLR and Prologis much more than European investors.

EUR investors anticipating green real estate issuance from the more solid US names could therefore be set for disappointment. For other EUR IG real estate bellwethers, such as Gecina, Vonovia Covivio and CTP such USD issuance would only take place if there’s a funding benefit by issuing in USD and swapping back to EUR versus a direct EUR issuance. But European real estate names tend to be much more aggressive in their leverage, which puts them on the back foot and will likely drive wide yields in USD space. Furthermore, both the EDF and Enel cases have confirmed that the ESG label in their USD bond has little bearing in bringing down yields.