Spotlight China - No quick turn in 'Zero-Covid' as Xi's third term arrives

CCP summit: Ongoing focus on state-led development, national security/tech self-sufficiency. Covid-19 policy: No quick turn, more pragmatism depends on progress with vaccinating elderly. Headwinds from Covid-19 policy, real estate, slowing global growth, and US-China tensions remain.

This article is part of the Global Monthly of October 2022

As expected, the 20th National Congress of the CCP held in Beijing last week resulted in a third term for Xi Jinping as the party’s General Secretary, paving the way for a third presidential term. Impressions from the summit broadly point to a continuation of policies that were set in motion under Xi, with his allies being appointed to the high-level Politburo Standing Committee. This means an ongoing focus on state-led development towards national security/tech self-sufficiency in a more hostile world. One of the key questions – both from a macroeconomic and investment point of view – is to what extent Beijing will stick to its strict Covid-19 policies as Xi’s third term arrives.

Covid-19 policy: No quick turn expected; move to more pragmatism depends on progress with vaccinating elderly

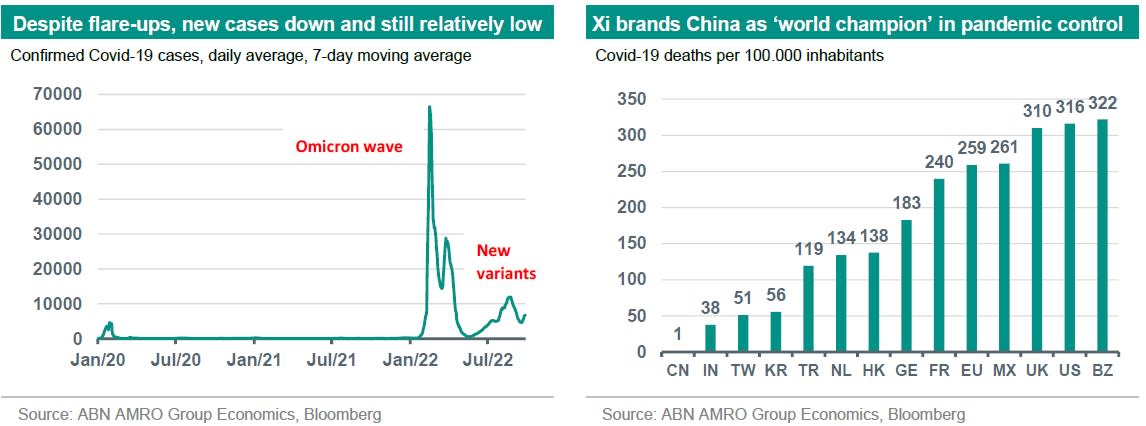

Whereas most other key economies have moved towards living with Covid-19 as an endemic disease, China has maintained its strict ‘Zero-Covid’ policy, although it has evolved over time to ‘mass testing and mini lockdowns under dynamic clearing’. Adherence to this policy is continues to hit consumption and confidence, aggravating the property downturn and hurting the ambition to boost consumption as a growth driver. At the same time, there have been more signs of public discontent over the policy. Nevertheless, Xi defended this vigilance at the CCP summit, pointing to the relatively low numbers of infections (despite renewed flare-ups) and deaths. With Covid-19 policy having become highly politicised, we deem a rapid move to laissez-faire unlikely. As the eldest, most vulnerable part of the population is still relatively undervaccinated, and herd immunity is far away, such a shift would lead to a sharp rise of the death toll and hospital capacity issues. The overall vaccination rate has gradually moved up to 90% in the course of this year, but only 67% of the 60+ population has received a booster. All of this does not preclude a cautious move towards a more pragmatic approach at a later stage, particularly after the National People’s Congress in March 2023, when all major policy committees will have reconvened. Initial signals of such a future shift are the reports on a potential further easing of restrictions for inbound travelers, the channelling of more resources into healthcare, and the cautious move towards introducing mRNA vaccines. A recent study by China’s Centre for Disease Control and Prevention also advocated a more pragmatic approach in Covid-19 policies.

Headwinds to remain significant

All told, a key takeaway from the CCP summit is that a major shift in Covid-19 policy should not be expected in the near term, and that it remains to be seen how much room there will be for more pragmatism next year. All of this could also hinder the recovery of the property sector. Coupled with the impact from the global growth slowdown and the flaring up of US-China tech tensions – following the recent US move to restrict the sale of advanced semiconductors and related machines to China – headwinds to the Chinese economy remain significant.