Housing Market Monitor - Price correction behind us, but big challenges ahead

The bottom for home prices is at a higher level than previously thought. Housing affordability will improve due to wage growth and lower interest rates over the long term. Our price estimates are revised upward: from -5% to -3% in 2023 and -3% to +2.5% in 2024. The number of transactions for existing homes remains low as few new homes are being built and sold. Transaction estimates remain the same at -5% in 2023 and -2.5% in 2024. Major challenge to make housing stock more sustainable gets boost from new mortgage lending standard.

ABN AMRO Group Economics

Author has left Group Economics, see text

This article is written by Bram Vendel

Despite poor sentiment in the housing market, prices appear to be rising again after a decline. On balance, prices are still 4,3% lower than the July 2022 peak, but the price index has risen slightly over the past 4 months. Furthermore, we see that homes with a lower energy label experienced a larger price decline and are now also rising less than higher labels. Since the rise in energy prices, consumers have started to pay more attention to energy costs when buying a home and this is reflected in their housing preferences. This effect will intensify when next year the energy efficiency of a home is included in lending standards. The big challenge is to build enough new energy-efficient homes and to make the existing housing stock more sustainable.

Prices are rising slightly and the price index appears to be stabilizing at a higher level than we previously expected. Despite the fact that prices have previously fallen and are now rebounding slightly, housing affordability remains moderate. Interest rate hikes worsened affordability. The price correction that followed slightly improved affordability. The accompanying wage increases further improved affordability. However, the price decline and wage increases together make up for only part of the deterioration in affordability since the interest rate hike. Because of the relatively more favorable development in recent months and expectations for the future, we are adjusting our price estimates upward from -5% to -3% in 2023 and from -3% to +2,5% in 2024.

The end of the housing price correction comes from factors such as a tight labor market, a historically large housing shortage, faltering new construction and stabilizing mortgage rates. Unions and workers are well positioned to negotiate for higher wages due to rising inflation combined with the tight labor market. This ensures that, on average, workers are experiencing strong wage growth and purchasing power is recovering. Meanwhile, the need for housing continues to grow steadily toward an all-time high, while new housing starts cannot keep up with this pace. An ECB survey shows that home buyers are getting used to higher interest rates and anticipate stable interest rates in the future. However, it will take time before the affordability, net housing costs divided by net income, of homes moves toward the long-term average. Until then, transactions for existing and especially new construction homes will remain at lower levels.

As new construction growth falters, housing transactions are under pressure. The construction of new housing is prevented by great political uncertainty following the fall of the government. Policy uncertainty over issues such as under resignation minister Hugo de Jonge's proposed rental market regulation is playing a major role now and towards the November elections. Also of great influence are the increased costs of labor and materials, higher interest rates and . Fewer permits are being issued and some projects are no longer economically viable, causing the plug to be pulled. Due to a lack of new homes, the throughput in the housing market is drying up which is depressing the number of transactions. Our estimates for transactions remain the same at -5% in 2023 and -2.5% in 2024.

Sentiment subdued, but rebounds slightly

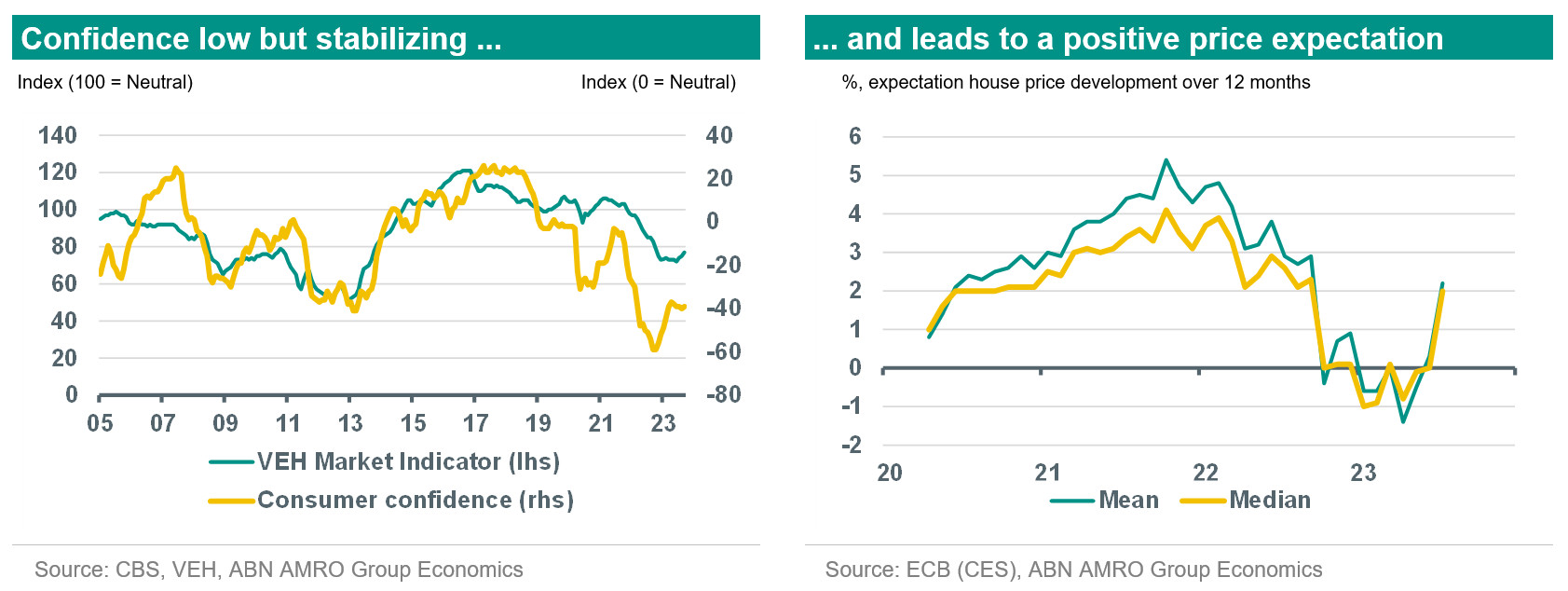

Although prices are rebounding slightly, sentiment in the housing market remains subdued. In the past quarter after stabilizing for a while, the market indicator of the (Vereniging Eigen Huis) rose from 72 in June to 77 in September. However, this is still far below the neutral level of 100. Respondents are more positive as interest rates and house prices developed more favorably over the past few months. In addition, consumer confidence, measured by CBS, has improved significantly since the end of 2022 and has been stable around -40 points in recent months, but still well below the neutral level of 0. A possible supporting factor for confidence is that housing affordability has improved slightly due to price declines and wage increases.

The difference between the depressed sentiment now and a more positive mood for the future becomes clear when looking at expectations about house price trends. Consumers, in contrast to last year, are more positive about house prices. In fact, the ECB's Consumer Expectation Survey shows that consumers expect prices to rise again. On average, consumers expect house prices to be around 2% higher in 12 months' time. This increase will mainly be concentrated in homes with a better energy label. This is because home buyers' housing needs and preferences are more focused on energy efficiency.

Positive outlook for the future lets demand rise and overbidding pick up

The positive outlook for the future seems to be having its effect on the housing market. After the turnaround last summer, more homes came up for sale and sellers received fewer viewings. However, this trend seems short-lived. Meanwhile, fewer homes are for sale again than six months ago and the of homes is also decreasing somewhat. The change to a buyer's market, where buyers have time to make a well-considered decision for perhaps the biggest purchase of their lives, seems to be stagnating again.

Viewings are getting busier and more and more buyers are coming forward to buy a home. With increased competition, buyers are slowly having to bid against each other more often to be sure of the home. Makelaarsland, the largest online NVM real estate agent, reported that overbidding is also increasing again. The percentage of overbid transactions is now 42%, compared with only 10% in December.

Price decline appears to turn into rise

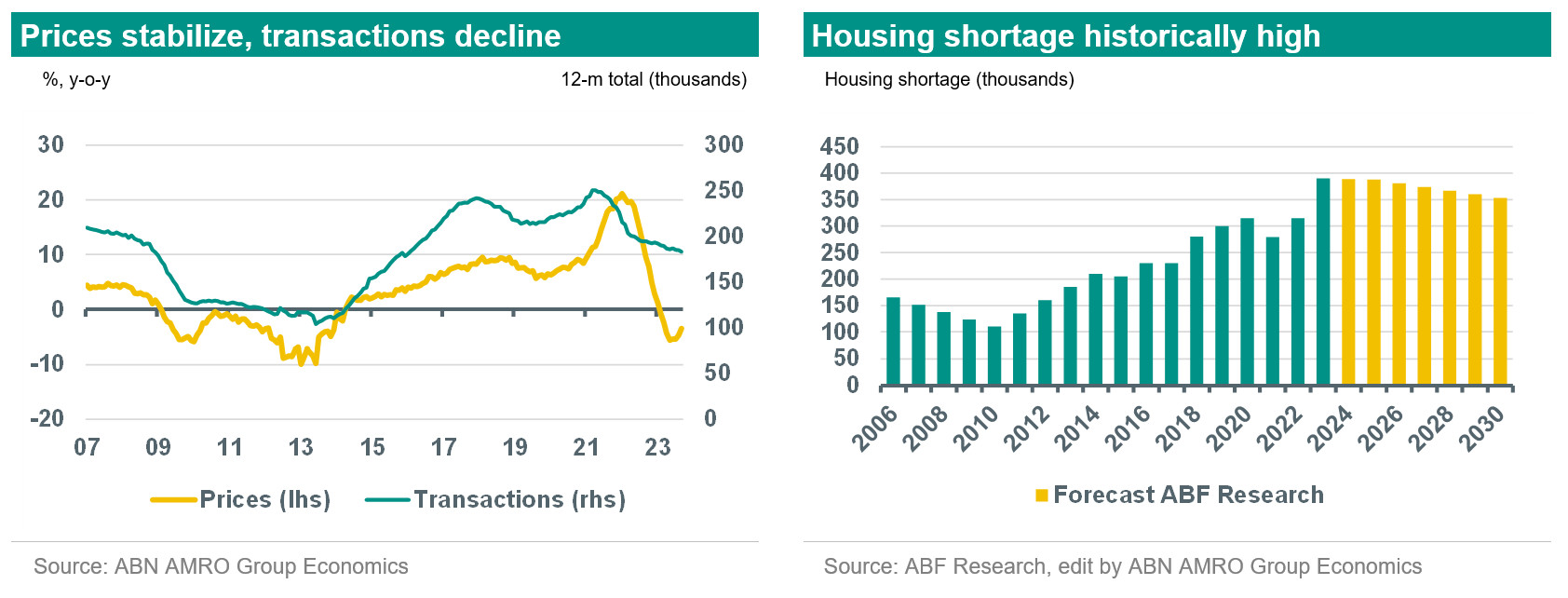

After almost a year of declining prices, there is again a sign of recovery. Over the past 4 months, prices have risen slightly. Meanwhile, the average price level measured by CBS and the Land Registry (Kadaster) in September is about 1.9% higher than in May. The summer months are historically better months on average when looking at price trends. Caution is warranted, but the price correction seems to have occurred. Despite this slight increase, homes for sale were still 3.5% cheaper in September than a year earlier.

Taking inflation into account, the price correction is larger than the 3.5% suggests. At first glance, this decline, especially compared to a decade ago, appears to be a short-term one and not very substantial. However, when looking at the real price level - the price level where you factor in inflation - it has fallen a lot more. Since July's peak last year, the nominal price level is now 4.3% lower, while the real price level is about 9% lower. When the prices of goods and services rose, house prices fell. This has caused house prices to be worth a lot less in real terms. The real price level has remained fairly stable after falling since April, meaning that house prices are currently moving along with the general price level.

An important factor in the stabilization of prices is the significant increase in wages. High wage growth gives households more financial room, allowing more people to look for homes. Our expectation is that collective wage growth will remain elevated for 2024 as well. In addition, stability in mortgage rates has contributed to the recovery. Long-term interest rates have remained fairly stable since the summer of 2022, giving potential buyers more security and encouraging them to take the step toward buying a home. Finally, the shortage of available homes, which estimates to be at an all-time high of 390.000 this year, is increasing competition among buyers which is supporting prices.

New construction falters and depresses transactions

The shortage of available housing, in addition to driving up prices, is creating a negative transaction effect nationwide. With few available homes and lagging new home additions, existing homeowners are less able to find their flow to suitable and often more expensive new construction homes. As a result, existing homes do not become vacant, putting a squeeze on throughput. This puts a brake on the number of existing- and new-construction transactions. Unabated high demand will support prices, while the lack of suitable supply is causing transactions to lag.

The number of existing-home transactions fell less sharply than before due to sentiment recovery and more positive future expectations. As of September, 183,000 homes had been sold in the previous 12 months. This is 5.8% fewer than in the 12 months before September 2022, when the counter stood at 194,000. The NVM that the number of transactions in the third quarter compared to the second quarter fell by 2% less than before. For the same quarter-on-quarter decline in 2022 or 2021, the declines averaged around 10% and were thus a lot more negative.

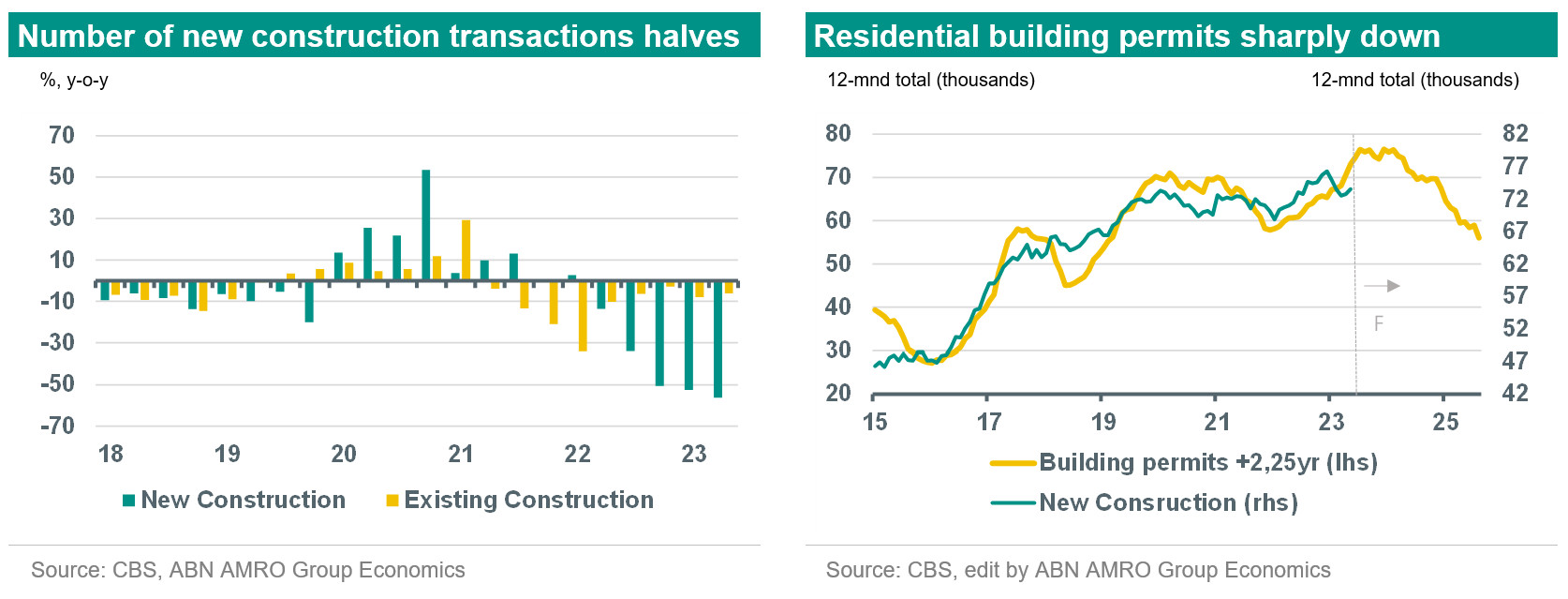

Unlike the number of transactions of existing homes, the number of new construction transactions fell hard again in the second quarter of 2023, according to CBS. The number of transactions halved year-on-year for three quarters in a row already. NVM's figures, which are often slightly ahead of CBS', that the number of new homes sold rose slightly in the third quarter compared with the first and second quarters. It is still early to draw conclusions, but the outlook for new home sales seems a bit brighter again after a low point.

High interest rates make it difficult for buyers to purchase a relatively expensive new construction home. Developers - unlike sellers of existing homes - have a harder time lowering their price. They are currently still very reluctant to reduce prices to mitigate any losses. One solution that offers relief is to modify the construction project during the design phase. For example, they can build smaller homes that are more affordable. Should this option not be feasible, as is the case with apartments, for example, they will have to proceed to cancel purchase contracts before the construction phase. The number of building permits applied for and issued is also decreasing. The graph on the top right shows that the number of new homes realized follows the issued permits with a delay of several years, indicating a lower number of new construction realizations in the future. This hinders the number of long-term transactions of new construction, as well as existing owner-occupied homes.

Transaction outlook uncertain

The outlook for the number of transactions remains moderate. To ensure more transactions and a good flow, the distressing housing shortage must be addressed. The under resignation cabinet therefore wants to build 900,000 homes through 2030. This plan is very ambitious and it remains to be seen whether this number will actually be achieved. Researchers from the Economic Institute for Construction (EIB) that in 2023 and 2024, per year, no more than 70,000 new homes will be built. This is much less than expected and far below the 100,000 that the outgoing cabinet aspires to.

There is also the question of whether homeowners will move on quickly to these available new homes. Sentiment may have improved slightly, but new-build homes remain very expensive due to lack of price reduction and high interest rates. In addition, high loan bridging costs, which have arisen due to the sharp rise in short-term interest rates, are a major obstacle. The long lead time and uncertainty between purchase and completion of the home does not help either. On a positive note, some homebuyers actually prefer to choose a new-build home. The main reason is the sustainability features of new construction, from both a cost consideration and a preference for a more sustainable home.

Changing mortgage lending standards important for sustainability

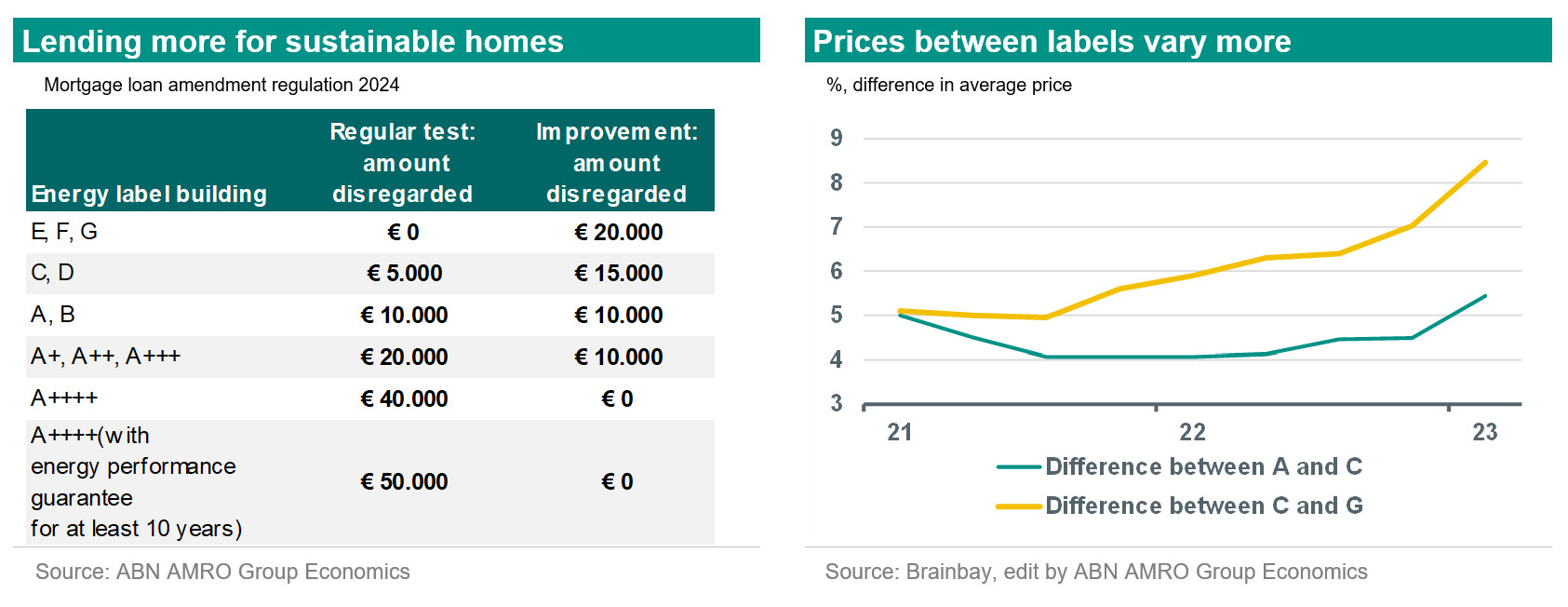

The change in lending standards could potentially improve the accessibility of new construction homes. As expected, from 2024 the energy consumption of a home will be taken into account when calculating the financing burden. This means that for the same income, more may be borrowed for a more sustainable home, which could be as much as €50.000. The idea behind this is that the money households save on energy can be spent on housing costs. Sustainable new-build homes can become available to a larger group of buyers through the extra borrowing capacity, which will help them move on.

Also, for an existing poorly insulated home (E, F, G), €20.000 may soon be disregarded when calculating the loan if it is invested in making it more sustainable. This amount may be borrowed regardless of income and associated borrowing capacity. This will reduce the monthly cost of energy consumption and accelerate the transition to a sustainable housing stock.

However, there may be a downside to this amending regulation. Brainbay previously that higher energy prices led to greater price differences between poor and good label homes. The mortgage loan modification regulation will potentially reinforce this price trend. The difference in price differentiation and borrowing capacity between labels will affect certain groups differently as a result. Move-up buyers, who on already live in more energy-efficient homes, may benefit as sellers from the wider borrowing capacity among buyers. First-time buyers, on the other hand, will more often be forced to choose relatively cheaper homes with a lower energy label and greater sustainability challenges. On average, first-time buyers bring in less equity and have a lower income, so they will be faced with a large expense item. A possible consequence is that in the future they will have to wait longer for a suitable house and next step in their housing career.

Homeowners attempt to keep interest costs low

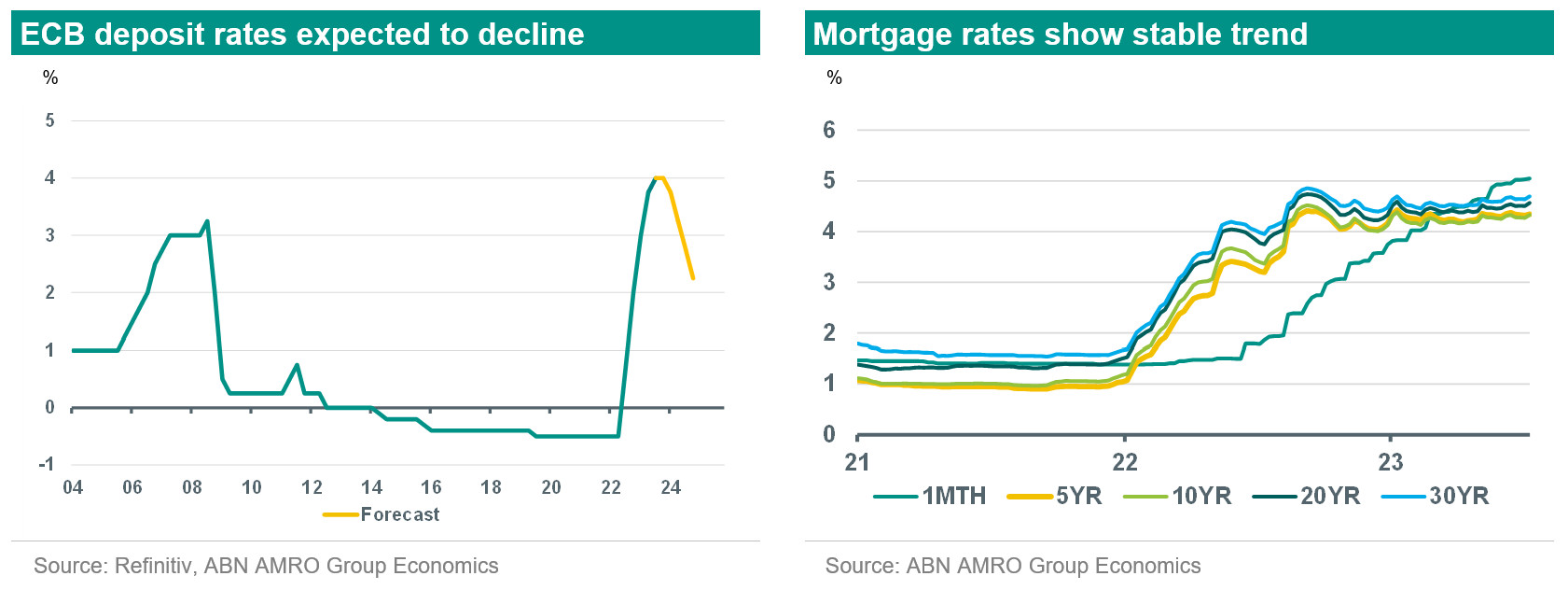

Short- and long-term mortgage rates that have risen hard since early 2022 are not helping buyers of existing- and new-build homes. Whereas the interest rate for a 10-year fixed-rate loan was 1.75% in January 2022, it is now above 4%. The reason for this is central banks raising policy interest rates to combat high inflation. After an interest rate pause by the U.S. central bank and an increase by the European Central Bank (ECB) to 4%, we expect that they both have landed at the peak of their interest rate cycle. Our expectation is that the ECB will begin rate cuts rather than increases in March next year.

The end of the interest rate cycle and possible interest rate declines in the future can also be seen in mortgage rates. These have shown some stability over the past year. Variable interest rates, on the other hand, have continued to rise because they are strongly linked to the ECB's deposit rate. We recently revised downward our growth forecasts for the Eurozone for this year and next. With weaker demand, companies will have more difficulty passing on higher prices to consumers. As the signs of declining inflation become clearer and the threat of an economic downturn more realistic, we expect the ECB to lean toward lowering interest rates rather than raising them.

However, this rate cut is not expected to affect mortgage rates as much. When the economic situation worsens, credit risks increase and this forces mortgage lenders to increase their risk premium. Before mortgage rates come down in the longer term, new buyers, and increasingly existing homeowners with a mortgage, will face higher interest rates. Our own research shows that existing homeowners have, on average, been paying more for their mortgages since the beginning of this year. Homeowners with mortgages eventually have to revise their mortgage rates and are worse off on average with new higher rates.

Finally, the period of poor affordability and high inflation is causing homebuyers to seek every possible way to reduce the cost of housing expenses. Higher mortgage rates now, and lower interest rates ahead, mean that short fixed-rate periods are especially in demand. More than half of all mortgage applications are for interest rates shorter than 10 years. These have a lower rate, and with deteriorating affordability, is no luxury. It also offers home buyers and owners more flexibility and potentially anticipates lower interest costs in the long run. Also, the ability to take any lower interest rates on the old mortgage with them when they move offers move-through buyers perspective. All in all, there are major challenges ahead over time, but also positive developments that can strengthen the market.