Housing Market Monitor - End of price correction in sight, but outlook remains subdued

Despite severely deteriorated housing market sentiment, the end of the price correction is in sight. We revise our price estimates slightly upwards from -6% to -5% for 2023 and from -4% to -3% for 2024. • Affordability will improve very gradually: via wage increases to offset increased inflation. The number of transactions will remain low due to moderate affordability as well as the lack of new housing starts. The transaction estimate for 2023 remains unchanged at -5%; for 2024 we reduce it from +2.5% to -2.5%.

In line with the deteriorating housing market sentiment, house prices fell sharply. The CBS/Kadaster price index was 6% lower in May than its July 2022 peak. House prices are under pressure in all regions, but have fallen most in major cities where house prices are more exposed to international cyclical fluctuations. Furthermore, it is mainly older homes with poorer energy labels that are experiencing a price correction. On the contrary, valuations of newer houses with a favourable energy label increased. As a result of increased energy prices, buyers have started to pay closer attention to the energy consumption of homes.

Despite recent price declines, the housing market is still moderately affordable. The ratio of net housing costs to net income is clearly higher than in the past. Housing financeability also leaves much to be desired. Set against the amount buyers are allowed to borrow based on their income, valuations are relatively high. Nevertheless, we take into account that a significant part of the price decline has already taken place. Partly because of the recently slightly more favourable data on price development, both from CBS/Kadaster and from NVM, we adjust our price estimates slightly upwards: from -6% to -5% this year and from -4% to -3% next year.

Part of the market correction needed for affordability and financeability will take place indirectly: via wage increases. Workers can force compensation for rising inflation in the form of higher wages due to the tight labour market. This is reflected in the increase in real disposable income, the income after adjusting for inflation. We expect incomes to continue to rise. Still, it will take time before wages are at the level where owner-occupied houses are again affordable and financeable. As long as that is not the case, the number of transactions of existing and new-build homes will be low.

The number of transactions is further hampered by the lagging construction of new homes. A series of problems plague the construction sector. The fall of the government has further increased policy uncertainty for the sector. This is affecting construction activity. The expected continued lack of housing realisations hinders the flow in the housing market. The lack of new construction puts a brake on the number of transactions, both new and existing homes. We maintain our earlier estimate of a 5% decline for this year, but lower the estimate for next year from +2.5% to -2.5%.

Housing market sentiment stabilises at low level

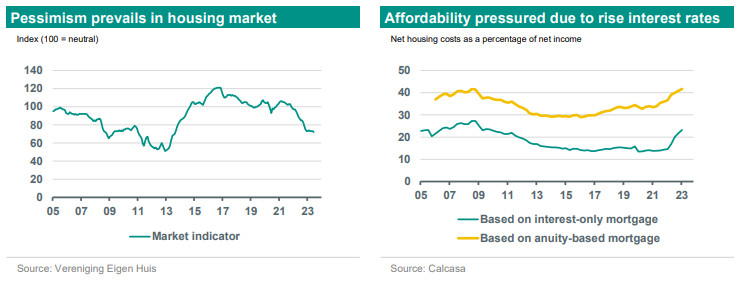

Confidence in the housing market has fallen significantly over the past year. In June, the stood at 72, well below the neutral level of 100. Last June, the indicator was still in the plus with a value of 104. The turnaround in housing market sentiment is mainly due to the rise in mortgage interest rates. As a result, buyers can borrow less on the basis of their income and net housing costs have increased relative to net income. In addition, the economic outlook is gloomy. For now, the worsened economic situation has hardly affected unemployment, but the labour market generally reacts to cyclical fluctuations with a time lag. We therefore expect unemployment to rise slightly.

The fall in confidence has now been halted, though. The market indicator has been at a similar level since December. This stabilisation stems from the outlook for mortgage rates. It is no longer rising, has remained more or less unchanged over the past six months and may be able to come down a bit again. In addition, house prices have already fallen considerably and incomes are rising. Both contribute to affordability. Furthermore, there are slightly more houses for sale, so buyers have some choice and the worst madness is over. Potential buyers notice this at viewings, which are less crowded. They can dwell a little longer on possibly the biggest purchase of their lives and experience a little less urge to overbid.

The housing market is still tense. The number of houses for sale rose to 31,500 in the second quarter, according to. That is sharply higher than in the same quarter last year, when there were over 25,000 houses for sale. But historically, the housing supply is still very low and well below the record 176,000 houses for sale at the end of 2012. Data on sales duration and the percentage of homes sold above the asking price also point to a historically tense housing market. In the second quarter of this year, homes were even sold slightly faster and more often above the asking price than in the first quarter.

Number of housing transactions under pressure

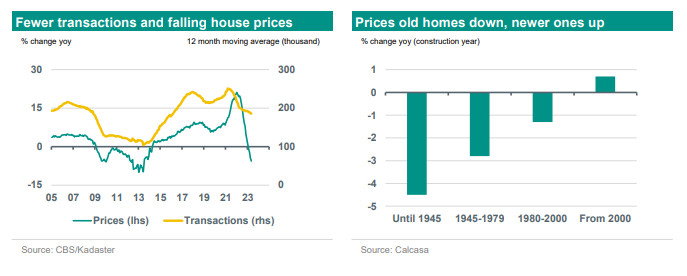

The stabilisation of housing market confidence at a low level is reflected in transactions. The number of transactions of existing homes is clearly falling less than before. In the 12 months to May 2023, a total of 186,000 existing homes went up for sale. This is 7% less than in the year to May 2022. Earlier, the number of transactions fell by 20% year-on-year. NVM figures also show that the number of transactions on a year-on-year basis is falling less sharply than previously.

However, the transaction outlook is anything but favourable. The number of purchases of existing homes is strongly related to how many new-builds come on the market and are sold. New construction creates room for flow within the existing home segment. Because of the persistent problems in new construction due to higher interest, wage and material costs, expensive building plots and the persistent nitrogen crisis, the number of realisations of new homes threatens to lag behind. Purchase contracts of new projects are regularly rescinded because the pre-sale limit of 70% has not been met. The decline in the number of building permits issued also points ahead to a decline in completions in the future. This threatens to hamper transactions in the long run, not only of new but also of existing properties for sale.

House prices have also fallen

The deterioration in housing market sentiment is reflected in the development of house prices. According to the CBS/Kadaster index, house prices in May were 5.6% lower than May last year. The average purchase price, which does not correct for differences in quality and gives a less reliable picture than the index, stood at EUR 404,000. That is more than EUR 42,000 lower than during the peak in July 2022. This puts a significant part of the price adjustment behind it. This is also evident from recent NVM figures, which are slightly ahead of those of CBS/Kadaster because they are based on the time of signing the purchase agreement instead of the time of passing at the notary. According to NVM, house prices rose 2.8% in the second quarter compared to the previous quarter. However, this was mainly because relatively many houses in the higher price segment were sold.

Interestingly, prices of older houses are falling, while prices of houses completed after the turn of the millennium are rising. This is probably because newer homes have a better energy label on average. This has added value because since the energy price hikes, buyers are paying more attention to energy consumption. Economical homes with lower energy costs are preferred. The influence of the energy label on the house price may increase further if the energy label becomes part of mortgage standards and helps determine the maximum mortgage amount. Currently it’show and when this possible adjustment could take shape.

House prices are under pressure in all regions, but have fallen most in the big cities. This is because prices in the cities have risen relatively strongly before, leaving more room for a downward correction. In addition, urban housing markets are somewhat ahead of the rest of the country, partly because homes there are traded more often and faster, but mainly because urban house prices react more violently to fluctuations in the international business cycle. The local economy there is more closely intertwined with abroad, so that a weakening of the international economy translates more quickly into urban house prices.

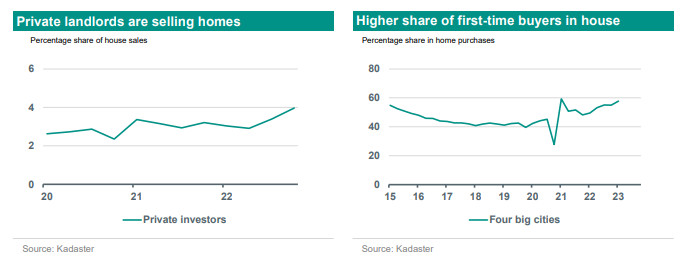

Furthermore, private landlords, who mainly operate in big cities, are taking a more cautious approach due to buyout protection, tax increases and stricter rent regulation, although the latter is less certain due to the fall of the cabinet. Meanwhile, on balance, sell more properties than they buy. Earlier, it was the other way round. In particular, landlords are abandoning relatively cheap flats with a low energy label. Whether the retreat of landlords actually affects house prices cannot be said with certainty. A recent study on the impact ofon landlords suggests that their impact on house prices is limited. In contrast, do link price increases in recent years to increased interest in house rentals.

Share of first-time buyers in transactions grows

The waning interest of private landlords offers opportunities for first-time buyers. After all, both parties tend to buy similar houses. The share of first-time buyers in housing transactions is indeed rising. However, this is not so much because first-time buyers have started buying many more houses, but because existing home owners are marking time and want to sell their house before buying a new one.

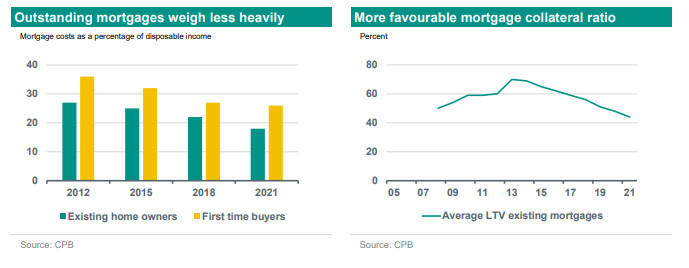

The difference in response between first-time buyers and existing home owners is noteworthy, as house purchase is ultimately more difficult for first-time buyers. Unlike first-time buyers, existing home owners can take past loans with lower interest rates into their next home. Furthermore, some existing home owners benefit from high positive equity values, partly thanks to steep price increases in the past. Also, because they are generally older, they have had more opportunity to build up savings buffers.

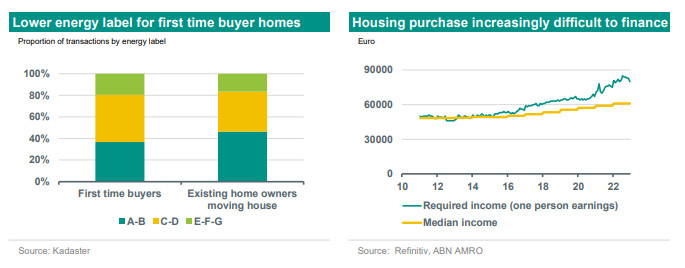

Finally, excisting home owners have on average a higher income than first-time buyers, so they can borrow more to buy a house. at current mortgage rates, only 3.4% of the 4.5 million large stock of owner-occupied houses falls within what first-time buyers can finance on the basis of one income. First time buyers with two incomes are in a better position, partly because the second income has been given greater weight in recent years when setting the maximum mortgage amount. For them, 40 per cent of the owner-occupied housing stock is within reach.

What may help first-time buyers is that they benefit faster from recent wage increases, as they are more likely to change jobs and get promoted. Then there are the increases early this year in the price ceiling for the transfer tax exemption and in the cost limit of the National Mortgage Guarantee. The latter went up from EUR 355,000 to EUR 405,000, allowing more buyers to get extra security at lower mortgage rates. Thanks to the increase, more housing transactions are again falling under the NHG limit and the NHG share of mortgage production is growing after years of decline.

The fact that despite all restrictions, the share of first-time buyers in transactions is rising indicates that the need is high. This is also evident from the age at which first-time buyers leave the parental home has risen significantly. There is a risk, however, that first-time buyers are forced to opt for relatively cheap houses with moderate energy labels and greater sustainability challenges. Furthermore, they run the risk of moving in at a less favourable time. Judging by affordability (net housing costs versus net income) and financeability (maximum loan amount versus average purchase price), the housing market is still relatively high priced. This can be seen in the chart below, which plots median income against the income needed to buy a home at the prevailing 10-year interest rate, lending standards and average purchase price. A possible consequence of this is that they will have to wait longer in the future before they can take the next step in their

IMF warns of overvaluation, but sharp correction unlikely

that house prices are overvalued in many countries. However, in our view, this need not yet lead to a sharp price correction like during the financial and euro crises. This is partly due to the shift in. Since the corona crisis, people have started working more from home. They attach more value to a comfortable home and are also willing to spend more on it. In its analysis, the IMF does not take this structural change into account.

Moreover, the price correction seems to be taking place partly through the back door. House prices have fallen much stronger in real terms, i.e. adjusted for inflation, than in nominal terms. Compared to the peak in July by 10% instead of 6%. Workers want compensation for high inflation and, given the tight labour market, have power to force wage increases. Wage increases will be relatively high in the coming years. With moderate house price developments, where net housing costs rise less than net income, owner-occupied houses will slowly become more affordable again.

A sharper price correction becomes further less likely when mortgage rates start to fall again. In response to sharply higher inflation, the European Central Bank (ECB) has revised official interest rates sharply upwards over the past year. These interest rate hikes affect economic activity with a lag. With demand weakening, inflation will gradually get back in line and the ECB can prepare to cut interest rates. Once signs of this change become stronger, 10-year government yields will start falling again. Following on from this, long-term mortgage rates may also gradually come down slightly. If mortgage rates do indeed fall, buyers will again be able to borrow more based on their income.

Whether there will actually be more borrowing space depends not only on mortgage interest rates, but also on income developments and the Nibud lending standards. It is difficult to predict in advance what the outcome of this combination of factors will be on the maximum mortgage amount to be borrowed. For now, we are taking a slight increase into account, which supports the price level.

, i.e. disposable income adjusted for inflation, is still rising. Given the tight labour market and the resulting wage increases, disposable income is expected to continue rising. This lends support to the price level. Less support comes from the Nibud lending standards, which will probably be tightened further next year. Inflation has increased households' expenses, leaving them with less money to spend on housing. Nibud looks at the average inflation rate of the previous four years when determining how much money is left for housing expenses. For the 2023 lending standards, Nibud only took into account one year of high inflation. From 2024, however, Nibud will start counting with two years of high inflation. This will likely mean that at the bottom line, there will be less money left for housing expenditure and the Nibud will have to further tighten lending standards.

Financial position of households relatively favourable

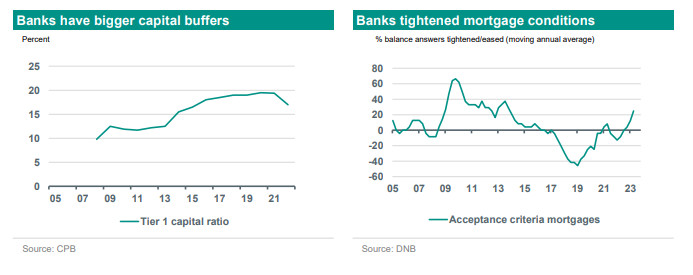

Furthermore, the of existing homeowners also provides some comfort. This has improved since the financial and euro crisis. They have lower mortgage costs relative to their income. The risk of this changing soon is limited. This is because the majority of homeowners have mortgages with long fixed-interest terms. According to DNB figures, only a quarter of mortgages will fall free in the next five years. And for those who have to refinance their mortgage, it remains to be seen whether they will lose out in monthly costs. After all, when these loans were taken out, mortgage interest rates were on average as high, if not higher than today. So, unlike in countries with on average short fixed-interest periods, mortgage borrowers face little risk of mortgage costs growing strongly after refinancing, let alone to the extent that the house might have to be sold. The risk of a sharper price correction caused by mass foreclosures is thus limited.

The threat of foreclosures is also limited by the fact that Dutch households have relatively . During the corona crisis, they could spend little, so savings increased. Even after corona, balances continued to rise. The balances provide a buffer in case of financial setbacks, such as higher grocery costs or higher mortgage interest rates. Combined with low unemployment, this keeps arrears low. According to the latest figures from the Bureau Krediet Registratie, a total of 41,600 households were in mortgage arrears in the third quarter of 2022, 12,000 less than at the beginning of 2020.

The ratio of mortgage debt to collateral value has also become more favourable in recent years, thanks to the long-time steep rise in house prices and the obligation to repay for those who want to qualify for mortgage interest relief. Thus, the risk of residual debt has decreased. the share of homeowners with residual debt would rise to 8% if house prices fell by 20% compared to the price peak in 2022. This is significantly lower than in 2013, when 30% of homeowners faced residual debt after a similar price drop. The group most at risk are young homeowners who recently bought a house without bringing in much of their own money.

No barriers to mortgage lending

Furthermore, a major cause of the sharp price correction during the financial and euro crisis is now absent. Mortgage lending is more stable than back then. Banks' financial buffers have improved over the past decade. As a result, banks are more resilient and can absorb setbacks more easily. Therefore, in case of any credit losses, banks do not have to apply the brakes as hard. The shows that while banks have tightened their underwriting criteria, the adjustment is less drastic than in 2008 and 2011. Moreover, mortgage origination risks are more spread out as many new providers have entered the mortgage market. As long as mortgage lending remains on track, transactions can continue to go ahead, contributing to stable house price development.

Finally, there is the continuing shortage of housing. The population continues to grow, mainly through migration as the Netherlands is considered an attractive country for settlement. In addition, more and more people want to live independently. The combination of a growing population and more single households creates a greater housing demand. Unfortunately, new housing construction can barely keep up with demand. Among other things, the limited availability of building land is a major obstacle. Outgoing minister Hugo de Jonge wanted to reform land policy and give municipalities more scope to expropriate more quickly. Whether this will happen is highly uncertain after the fall of the government. This also applies to other dossiers like the National Spatial Strategy. With the growing uncertainty for the construction sector, there is a growing risk that the number of housing completions will lag behind the housing demand. According to ABF Research, the statistical housing shortage has already increased by 75,000 to 390,000 last year.