(Green) hybrid bonds by utility issuers: a good place to be right now

Issuers of green utility hybrids operate with a decent buffer in their credit metrics in the majority of cases. Utility hybrids offer attractive spreads in comparison to their senior equivalent, and there are many green hybrid bonds which also have a significant carbon reduction impact.

We take a look at some of the (green) hybrid bonds issued by European utilities issuers

We evaluate whether green hybrids trade with a greenium and we show that these instruments are very attractive from a z-spread perspective

Issuers from these hybrid instruments operate with a decent buffer in their credit metrics in the majority of cases

Utility hybrids offer attractive spreads in comparison to their senior equivalent, and there are many green hybrid bonds which also have a significant carbon reduction impact

Green hybrids trade with a strong greenium

Green hybrid bonds are structured exactly the same as green senior bonds. That is, they both follow definitions and governance practices as set out in the issuer’s Green Bond Framework, and they both commit to invest the proceeds raised towards green projects. Furthermore, although some of these instruments are structured as perpetual bonds with no defined maturity, rating agencies have never perceived them as different to regular (non-green) hybrids.

The first utility company to issue a green hybrid was TenneT, the Dutch TSO, in 2017. Since then, other peers, from the regulated and non-regulated space, have come to the market with such instruments. However, do these instruments provide a pricing advantage? That is, do green hybrids by utility issuers carry the so-called “greenium”, meaning that investors are willing to accept a higher price for these bonds vs a non-green equivalent, given their green characteristics?

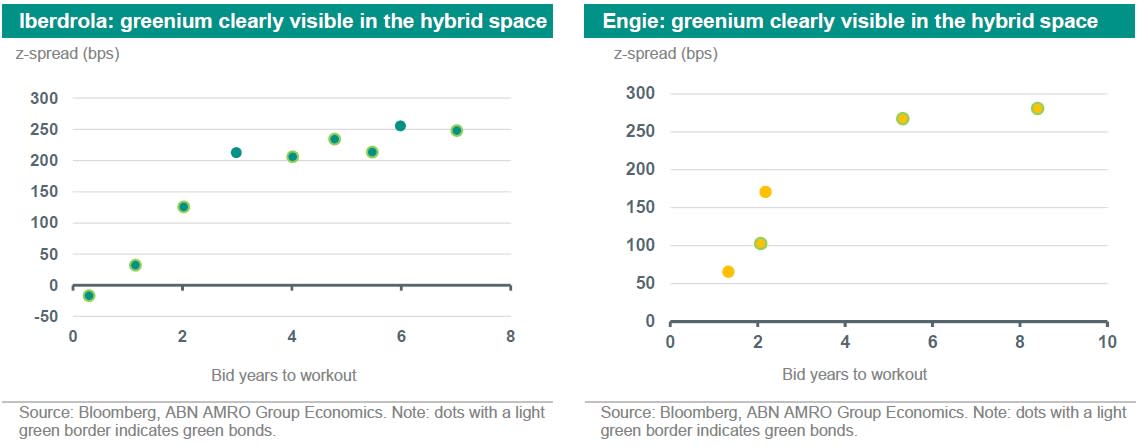

To answer this question, we have looked at the hybrid curves of Spanish utility generator Iberdrola, and its French peer Engie. The reason for choosing these two entities is that these are at the moment the only issuers in the EUR bond space that have both, green and non-green hybrids outstanding. All other utility issuers have either only green or only non-green hybrids outstanding. As shown in the chart below, there is clearly a greenium in the secondary market for these bonds. For example, the green IBESM 1.874 PerpNC4 bond trades 8bps tighter than the non-green IBESM 1.45 PerpNC3. The same is observable when looking at Engie hybrid bonds. For example, the non-green ENGIFP 1 5/8 PerpNC2 trades a whooping 70bps wider than the green ENGIFP 3 ¼ PerpNC2, with both bonds having very similar maturities. We note however that the greenium has been present but historically very small. For example, in the aforementioned example of Iberdrola, the greenium had reached 70bps in October last year, and has averaged around 20-30bps throughout 2022. Nevertheless, the presence of a greenium clearly indicates that green hybrid instruments are a strong preference for investors.

Hybrid bonds by utility issuers look very attractive, but watch out for the headroom

We broaden our scope and take a look at the entire European utilities hybrid universe (that is, not only green bonds). We are interested in evaluating whether hybrids look attractive compared to a senior unsecured bond. More specifically, we focus on (i) the spread pick-up offered by hybrids vs. same maturity senior unsecured bonds, but also (ii) whether these companies operate with a decent buffer on their credit ratings downgrade thresholds (as the hybrids would suffer most in case credit rating downgrades materialize). We also evaluate whether any of these hybrids have a yield which exceeds the issuer’s cost of equity, as this could be an indication of the bond market expecting a significant deterioration in a company’s fundamentals.

The table below summarizes a few pairs we have selected of senior and hybrid bonds of various utility issuers. The bonds included in such pairs were also issued before January 2022, as this allows us to also analyse what was the pick-up between senior and hybrids before the outbreak of the Russia-Ukraine war. In some cases, no appropriate pair was found, hence the issuer is not included in this analysis.

From the table above, we are allowed to draw two conclusions: (1) the pick-up between hybrids and senior bonds has been very attractive, from a z-spread perspective. However, (2) this is not the case when looking at outright yields. The denominator effect from the rise in base rates was strong, which reduced the yield pick-up. This ultimately means that hybrids from utility issuers are only an interesting investment in case the investor hedges the interest rate risk. However, this is already what most investors do, which makes hybrids the cheaper instrument for investors at the moment. The table above allows us to demonstrate that an investor can get similar duration risk, same credit risk (given it is the same issuers, although hybrids carry a lower rating due to subordination), but still earn up to 250bps (in case of EDF) if invested in the hybrid bond.

Nevertheless, hybrid bonds offer a higher spread than senior bonds for a reason: they also carry more risk. With that in mind, we also take a look at how much headroom these companies have in their credit rating metrics, before a downgrade takes place. We have summarized such analysis in the graph on the next page. Issuers that show a positive headroom are companies that currently have credit metrics (in this case, FFO/debt) above the downgrade threshold. This also means that companies that currently operate with negative headroom are issuers that investors should watch out for. This is because of two reasons: (i) this increases the chance of an issuer to not call the hybrid or to call but not replace a hybrid (more so in a current environment where interest rates have increased significantly), and (ii) a downgrade would require the spread on the issuer’s curve to re-adjust upwards, even more so on the hybrid instrument ultimately resulting in significant losses for investors (for example, the spreads on the hybrid bonds of EDP, where the issuer has a BBB3 composite rating P, have a pick-up of around 40-60bps to Iberdrola’s hybrid bonds, where both issuers are rated BBB+). For point (i), a good example is the Spanish company Naturgy, which recently had all of their hybrids adjusted to “no equity content” given their decision to call and not replace the hybrid. While this did not ultimately result in a downgrade, given the company’s strong fundamentals, the move did resulted in an increase of debt by EUR 750m. Another example is EDF, which has in November last year also made a similar move, and this resulted in S&P downgrading their hybrids from a BB- to a B+. Still, the graph below allows us to see that overall, utility issuers seem to be solidly positioned in their credit rating categories, with the exception of EDP and EnBW.

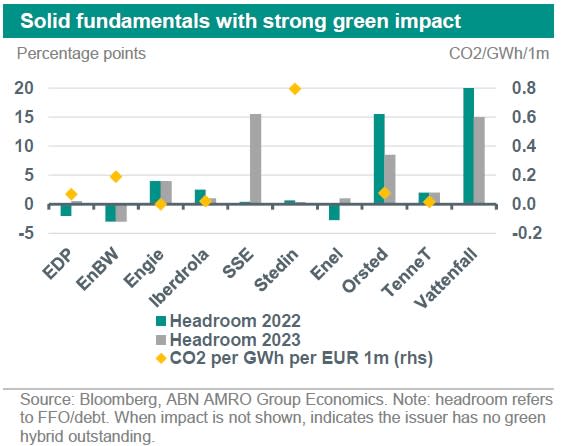

We also included in the graph above the impact of the green hybrid bonds in terms of carbon reduction. This is part of a previous analysis. Basically, investors could benefit from sitting in a solid credit name, which offers an attractive pick-up and on top of that, also has significant impact in terms of CO2 avoidance per GWh, per euro invested. The graph above shows that for example, on a comparative basis, Stedin offers a significant carbon impact on their green hybrid (this is mostly due to it being a DSO rather than a generator), which is also true for EnBW and Orsted. Orsted therefore for example stands out as an issuer with significant impact but also headroom in their credit metrics.

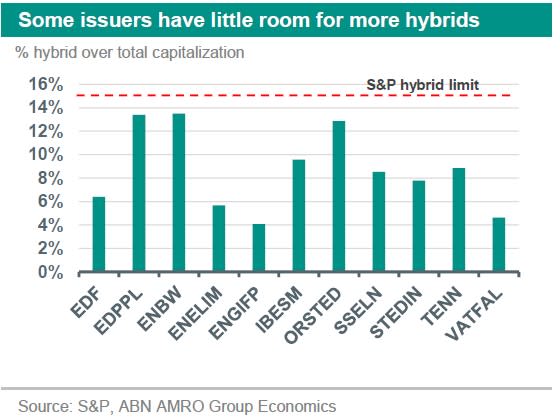

Another important factor to take into consideration is the fact that, as per S&P methodology, the total amount issued in hybrid bonds should not exceed more than 15% of the issuer’s book capitalization. If that is the case, then the hybrid bond in excess of the 15% will be assessed as having no equity content. While it is very unlikely that such a situation takes place (for example, issuers could in such a case just issue more senior bonds to increase capitalization), it is something that investors should also keep in the back of their minds. More importantly for the issuers that operate below (or very close to) their credit rating downgrade thresholds. That is because for these companies, an increase in debt would generally weigh very unfavourably for their credit metrics, and on top of that, they could have exhausted their hybrid firepower (remember – hybrid bonds with equity content are accounted for as 50% debt and 50% equity in credit metrics according to the more stringent S&P methodology).

Lastly, we have looked at whether the hybrid yield is below or above the cost of equity. We use the cost of equity as reference, as a hybrid bond yield which is higher than the corresponding cost of equity basically indicates that (i) it is priced as perpetual and (ii) that investors are expecting steep losses that the equity side is not taking into consideration. Luckily, this is not the case with any of the utility hybrid bonds, once again reinforcing the attractiveness of these instruments.

Conclusion

Utility hybrid bonds could offer investors an attractive opportunity, given that it allows for them to have same duration and same credit risk with a more attractive spread. However, investors should prefer hybrids by companies which are solidly positioned in their credit ratings and have strong fundamental profiles. Green hybrids also seem to have a strong greenium and investors could also pick the instruments that offer the largest impact in terms of carbon avoidance.