Global Trade: Outlook worsens, but supply bottlenecks ease

Pandemic and war cause erratic development of world trade in past years. Outlook worsens due to global inflation wave and sharp tightening of monetary policy. Supply-demand imbalances ease again: delivery times show improvement, container tariffs drop sharply.

PM: This article has been published (in Dutch) in globe, business magazine for international trade from evofenedex.

Global trade has been greatly affected by the course of the pandemic in recent years. This year, the post-pandemic recovery of world trade is particularly threatened by the conflict in Ukraine. The sharp global rise in inflation and the sharp reaction of central banks to it is putting pressure on global growth. This also affects world trade.

Pandemic causes erratic development of world trade in past years

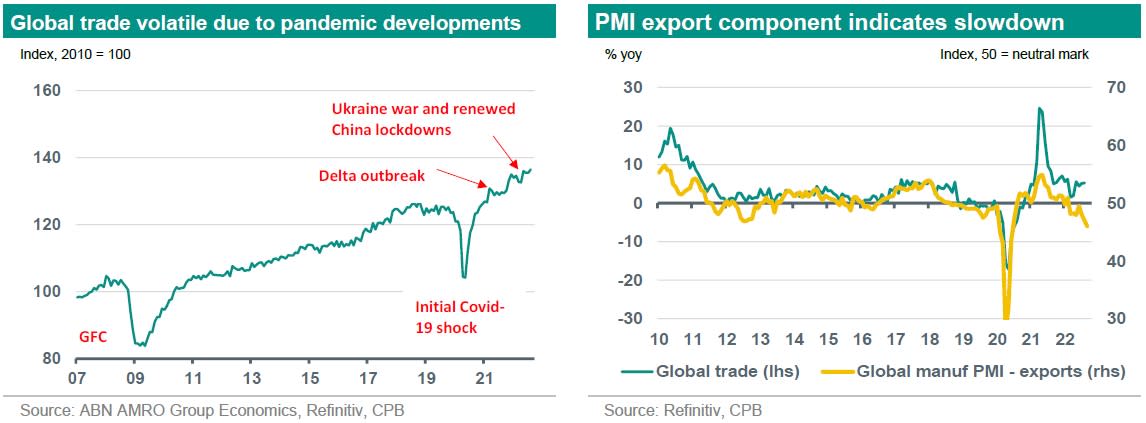

World trade has shown a volatile development in recent years, heavily influenced by the course of the corona pandemic. Global trade volumes (according to the CPB index) took a huge hit during the initial Covid-19 shock in the early 2020s, when first global manufacturing and trade powerhouse China went on lockdown and then the rest of the world. The drop in the CPB index that occurred then was similar to that during the global credit crunch (GFC) about a decade earlier.

Already during the first Covid-19 year of 2020, however, a rapid recovery occurred, thanks to the rapid realignment of production in China and a government policy-supported demand recovery in the Western world. By October 2020, the CPB index had already returned to pre-corona shock levels. After this strong rebound in world trade volumes in the first Covid-19 year, things took a bit of a turn for the worse in 2021, including the breakout of the Delta variant that led to new lockdowns. However, thanks to the base effect from the 2020, annual world trade grew by as much as 10% in 2021.

2022: Challenges from war in Ukraine and new lockdowns in China

Earlier this year, the war in Ukraine and renewed lockdowns in China due to the Omicron variant (with the world’s largest port city Shanghai in a five-week lockdown) posed serious challenges to world trade. For now, the resulting damage is much less than the blow following the initial Covid-19 shock. Although trade between Russia and the West has stalled and Russia is a very important player in the markets for energy and other commodities, Russia's position in the international trade of goods is modest. Moreover, China again managed to resolve production and transportation bottlenecks fairly quickly this year. Meanwhile, demand from Western countries initially held steady, thanks in part to a recovery from earlier lockdowns and supportive government policies. All in all, world trade growth for the first seven months of this year was at an above-average pace of around 4.5%.

Outlook worsens due to global inflation wave and sharp monetary policy tightening

Yet the outlook for world trade is deteriorating rapidly. The global economy is currently struggling with skyrocketing inflation, largely (especially in Europe) a result of increased energy prices due to the escalation of tensions with and cessation of energy flows from Russia. This has hit disposable income significantly and eroded consumer and producer confidence. In addition, central banks are reacting strongly to high inflation. The Fed and ECB have already raised policy rates by 300 and 200 basis points, respectively, this year, and we expect further hikes in the coming months – both in the US (125 bp) and in the eurozone (50 bp). Although European governments are currently trying to offset the effects of high gas and other energy prices on household purchasing power, we still expect a recession in the eurozone in late 2022/early 2023. We also expect a (mild) recession for the US. At the same time, in China, the recovery from the lockdown-related slump in the second quarter of this year is constrained by continued headwinds from stringent Covid-19 policies and problems in the real estate sector. Moreover, US-China tensions on Taiwan and tech have flared up again, and the US has prohibited the sales of advanced semiconductors and related machines to China. All in all, we think global growth is going to cool considerably. That obviously affects global trade. The decline in the export component of the global PMI (to well below the neutral level of 50) is a harbinger of this.

Supply-demand imbalances ease again: delivery times improve, container freight rates drop

In recent years, due to the pandemic, global trade was regularly disrupted by supply-side problems, such as the closure of terminals at some Chinese ports. Imbalances between global supply and demand for goods were additionally exacerbated by a shift in global demand from services to goods during the pandemic, but also as a result of stimulative monetary and fiscal policies. All this was reflected, among other things, in longer waiting times for unloading container ships, increasing delivery times in global production chains and a sharp increase in freight rates in container transport.

We developed an index to measure these types of bottlenecks and global imbalances in the supply of and demand for goods. This index showed a sharp increase during 2021, illustrating the increased imbalances between supply and demand. In recent months, however, this index indicates a sharp reduction in these imbalances, not least due to a sharp cooling on the demand side. For example, delivery times show marked improvement in recent months. Container rates have now fallen again by around 70% from their peak in the fall of 2021, although they are currently still are more than two times above the average seen in the last year before the pandemic broke out (2019). To conclude, improvements in these areas may ease the pain of the slowdown in global trade a bit for exporters and importers, and also help to slow down somewhat the inflationary spiral that is currently holding the world in its grip.