China - Economy shows some resilience as more US tariff threats loom

Chinese economy shows resilience despite the stepping up of US import tariffs, and targeted retaliation. We expect policy makers to continue with stepwise fiscal stimulus and more monetary easing, although Beijing is keeping part of its powder dry, with more US tariffs threats looming in April.

Economy shows some resilience despite the flaring up of a tariff war with the US

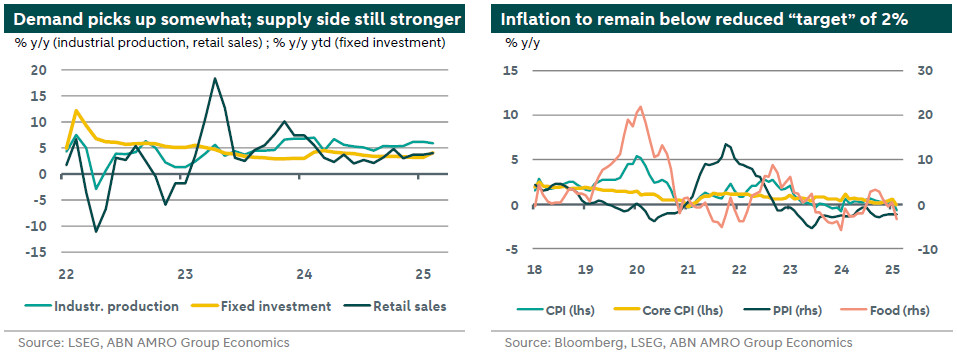

The Chinese economy is showing resilience, just as tariff tensions with the US have flared up. The US raised import tariffs on all imports from China twice by 10% in February/March, with Beijing responding immediately, but in a measured way (see here). Still, the February PMIs came in stronger than their January readings, with both manufacturing PMIs showing strong gains. Monthly activity data, combined for January/February given the annual shift in LNY timing, also came in stronger than expected (see here). The recovery is still led by the supply side. Industrial production (±6% y/y ytd, likely supported by some trade frontloading), continues to outpace retail sales and fixed investment (±4%). New lending for January/February combined also picked up on fiscal stimulus, but corporate and household lending remained weak. Other data were less convincing too. Real estate keeps weighing on Chinese growth, with property investment still deeply in contraction territory and annual growth of residential home sales turning negative again. Foreign trade was also disappointing, while the jobless rate unexpectedly rose to a two-year high of 5.4%. On the inflation side, CPI inflation turned negative again in February (-0.7% y/y), as expected and driven by base effects/food, while producer prices remained in deflation territory (-2.2%) for the 29th month in a row. We still expect inflation to pick up this year, though remaining below the inflation “target” that was cut to ±2% this year.

Stepwise fiscal stimulus continues, but part of it remains contingent on tariffs

Beijing’s commitment to more fiscal support was confirmed in early March at the NPC (see China – More tariffs, more support). The nominal budget deficit target was raised to 4% of GDP (from 3%), and the targets for local government and sovereign bonds issuance were increased as well. Taking all together, the consolidated deficit could rise by ±2pp to roughly 9-9.5% of GDP this year. Official language about the need to boost consumption has gotten louder. This is needed anyway, but also reflects the expectation that exports will lose strength this year (partly due to US tariffs). In early 2025, Beijing already extended a consumer subsidy programme. Mid-March, a new plan to boost consumption followed, with a focus on increasing real incomes while cutting costs of child, medical and elderly care (see China – Good start to 2025, Consumption support forthcoming). All in all, we expect Beijing’s stepwise fiscal stimulus to continue. Still, part of the powder will be kept dry until more is known about further US tariff plans – which we expect to be communicated in early April. Capital injections into large state and policy banks (for at least CNY400bn) are forthcoming as well. Next to this, we still assume more monetary easing (in the form of policy rate and RRR cuts), but the PBoC is not in a hurry given the latest data and looming additional tariffs. While the tariffs implemented so far still fit within our base case (increase of US import tariff rate to 45%, from currently ±30%), from April onwards China may be faced with more country-specific tariffs (linked to the findings of a US China-study), ‘secondary tariffs’ (eg tied to energy trade with Venezuela), product-specific tariffs, and with a US plan to drastically raise US port fees on China-linked vessels (see Global manufacturing, New disruptions on the horizon). All in all, we see both upside (resilience so far, more stimulus) and downside (more tariff threats) risks to our growth forecasts, which we will review in April.