Global Monthly - China: Policy easing continues as Omicron drag builds

Qoq growth picked up in Q4, but yoy growth reached the lowest pace since first half of 2020. Near-term growth forecasts revised down on pandemic risks/Omicron. Mini rate cuts and other policy easing continues, as ‘stability’ is Beijing’s buzzword for 2022.

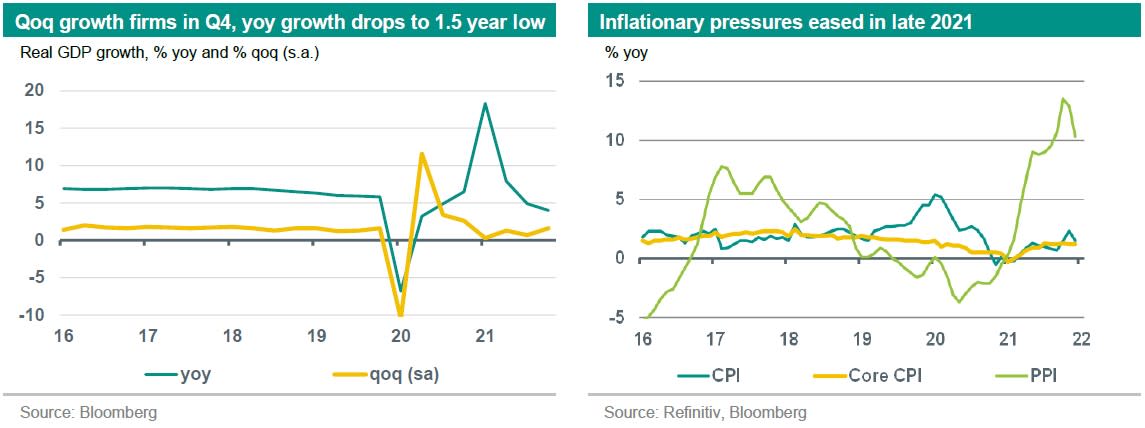

Full-year annual growth in 2021 came in at an above-trend pace of 8.1%, driven by the base effect from the initial covid-19 shock in early 2020. However, sequential growth was much less impressive last year. In line with our expectations, quarterly growth picked up in Q4, to 1.6% qoq (Q3 revised up to 0.7%). This recovery was production-led, helped by the fading of supply-side disturbances stemming from a power crunch and strict covid-19 policies over the summer. That said, annual growth in Q4 fell to 4.0% yoy, the weakest pace since 1H-2020, with drags from real estate and the pandemic persisting. We have cut our near-term growth forecasts on pandemic risks/Omicron. The impact thereof on full-year growth for 2022 is offset by some ‘payback’ later this year, and by a further policy shift from financial de-risking to (piecemeal) easing. We have cut our 2022 growth forecast marginally to 5.1% (from 5.3%), and raised our 2023 forecast to 5.3% (from 5.2%).

Omicron puts China’s strict covid-19 policies to the test

Drags from pandemic flare-ups and the highly contagious Omicron variant combined with China’s strict covid-19 policies continue to build, with uncertainty remaining high. We have seen local lockdowns (Xi’an’s city-wide lockdown was due to a Delta outbreak), and a tightening of restrictions in the run-up to the Chinese New Year period and the Beijing Winter Olympics. In late 2021, China’s covid-19 policy seems to have shifted somewhat from ‘aim for zero cases’ to ‘quickly contain local outbreaks’. Further Omicron outbreaks could put this decentralised approach to the test and lead to more widespread lockdowns and even tighter restrictions. As indicated in our , Omicron reduces the likelihood that China will ease its covid-19 policy soon. Meanwhile, related supply disturbances (some temporary production cuts, rising port congestion) adds to bottlenecks in global supply chains. At the same time, an Omicron-related delay in the rotation in global demand back to services may be beneficial for Chinese exports, which have continued to outperform during the pandemic.

Mini rate cuts and other policy easing continue, as ‘stability’ is Beijing’s buzzword for 2022

With drags from Omicron and real estate persisting and CPI inflation remaining below target, China’s (piecemeal) easing approach continues, in line with our expectations. Since December, the PBoC has cut the reserve requirement ratio (RRR) for banks by 50bp, and lowered several of its policy rates in one or more mini steps. The 1-year loan prime rate (LPR) was lowered by 15bp in two steps, to 3.70%, and the 5-year LPR by 5bp, to 4.60%. The medium-term lending rate was cut by 10bp, to 2.85%, and the 7-day reverse repo rate by 10bp, to 2.10%. We expect piecemeal monetary easing to continue in the coming months, with another 50bp reduction in bank RRRs and further mini cuts in policy rates. We also expect more fiscal support in the form of targeted tax cuts for households and firms, and easier financing conditions for local governments. Regarding real estate, we have seen some easing of policies over the past months and expect further steps going forward.