Gas market monitor - Europe’s gas from boom to gloom

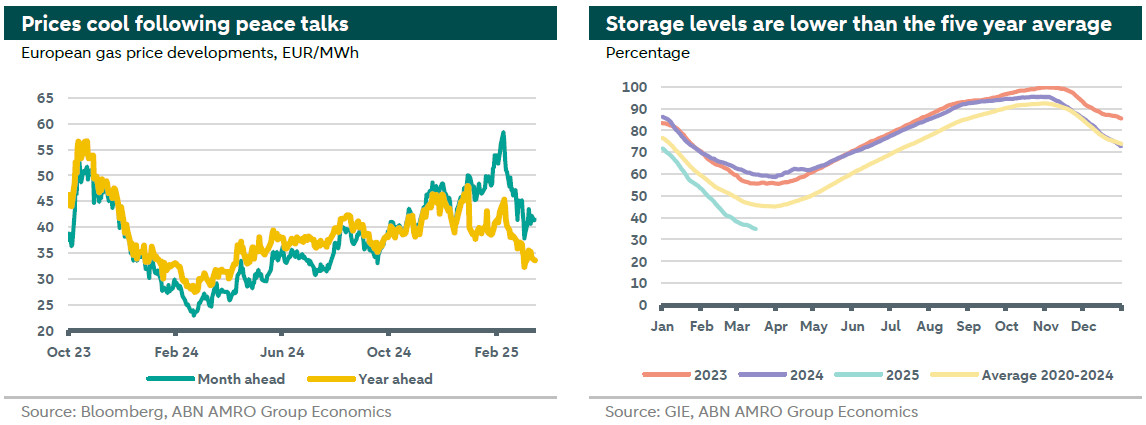

The end of the transit agreement through Ukraine in December 2024 resulted is substantially higher prices. The rally in prices was further fueled by increasing warries on the timely refill to meet regulated storage requirements (90% full by 1st of November). As a result of these factors, Europe was at the edge of a new gas crisis. But gas prices shifted course in mid-February. Several factors helped in cooling the market. The most important reasons are the ongoing peace talks to end the Ukrainian war, along with potential flexibility in of storage targets. In addition, approaching the end of the heating season with favorable weather conditions helped easing the market by mitigating the storage withdrawal rate. Accordingly, the month-ahead benchmark is back towards 40 €/MWh levels after hitting a two year high of 58.4 €/MWh in February. Since the start of March, TTF prices averaged 41.5 €/MWh for the benchmark month-ahead contract (34.4 €/MWh for the year-ahead contract. European industrial demand recovery starts to pick up but US tariffs could seriously dampen the outlook, while LNG markets remain tight and volatility is here to stay. European TTF month-ahead contract is trading around 41.5 €/MWh at the time of writing.

Gas prices fell from its two year high following peace talks, possibility of flexible storage plan, and mild weather conditions

The end of the Ukrainian war may ease sanctions on Russian energy with a possible return of gas supply to Europe, but LNG remains crucial

European industrial demand recovery is picking up but a slowdown is in the horizon due to US tariffs

Geopolitical tensions and potential US tariffs keep market volatility high; a peace agreement would lower prices

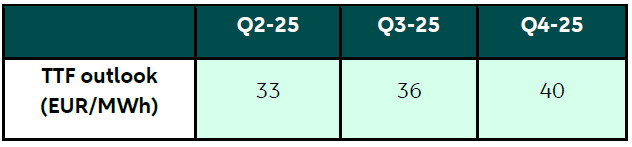

Our outlook for the year ahead TTF contract is to average 33 €/MWh in Q2

European gas market developments

As indicated above, several developments helped shifting the rally in TTF prices. First, the peace talks to end the Ukrainian war mediated by the new US administration raised hopes for a possible return of Russian flows to Europe, or at least a potential increase Russian LNG shipments. Any peace agreement could relieve or lift sanctions on Russian energy supplies. In that regards, the return of Russian pipeline gas could come through Ukraine again by signing a new transit agreement or through other pipelines like Nordstreams. In fact, there are talks about American interest to take part in returning Russian supplies through Nordstream pipelines. But only one pipeline in Nordstream 2 has the potential of delivering Russian gas because Nordstream 1 and another Nordstream 2 pipelines have been sabotaged in a mysterious attack in 2022. However, this possibility is tied to the approval of the German government as Nordstream 2 had never been operated or delivered any gas since the war erupted just before the German government authorized it.

Meanwhile, several countries requested the European Commission to relax regulated inventory targets as storage level concerns have resulted in a flipping in summer-winter spread where summer gas futures have been trading above winter gas futures, disincentivizing storage injections over summer and raising the risk of not meeting the target. The Commission is expected to announce flexible gas storage plan in April which helps bring some ease to the market [1].

Additionally, favorable weather conditions of warm temperatures and speedy wind helped decreasing storage withdrawal rate. Moreover, the resume of flows from Norway and the increase in LNG imports helped reduce market worries (see rhs below). Even though gas storage levels are still below their seasonal averages at 34.8% (see chart rhs chart above), they are expected to end the heating season with higher levels than previously anticipated, especially since we are only two weeks away from the end of the heating season. Adding to the downward pressure on prices is that the German subsidy proposal that aim to refill the storage in a timely manner even with the presence of high prices, has not gone forward.

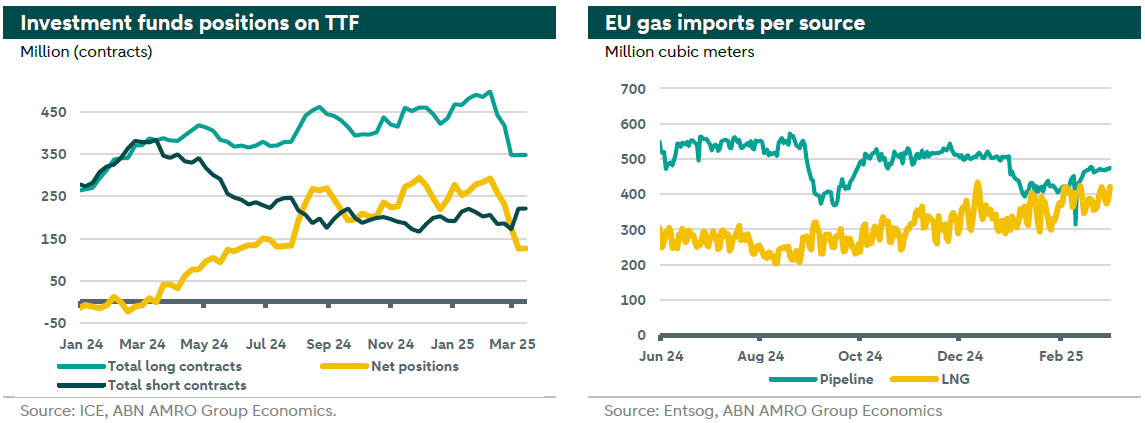

These developments explain the easing of bullish sentiments across market participants as illustrated by the decrease in net long position of investments funds in the chart below (left).

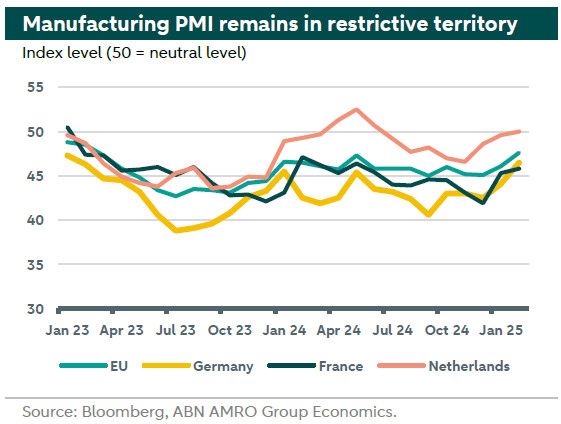

From the demand side European industrial demand recovery continues. The Eurozone composite PMI for February remained constant, just above neutral in expansionary territory at 50.2. However, the eurozone economy witnessed an expanding manufacturing activity and a shrinking in the services sector. Crucially for gas prices, manufacturing started to ramp up to 47.6 (46.6 in January). The pace of manufacturing contraction eased in main economies, most notably, with a surprising performance, in the industrial heavyweight Germany 46.5 (44.1 in January), as can be seen in the chart below. Current output and new (export) orders contributed to this improvement in the manufacturing PMI. This could be attributed to front loading impacts of the expected US tariffs under the new US administration. At the same time, these tariffs are expected to have adverse impacts on trade flows and growth in the EU (see our global outlook for 2025 ). This is foreseen to slow down the recovery in industrial demand, starting from the second half of 2025.

In addition, demand for heating purposes is expected to subdue as we approach the end of the winter season. However, adverse weather conditions, such as cold spells, heat waves, cloudy sky, or slow wind remain a source for volatility as they would increase demand and put an upward pressure on prices.

The geopolitical premium on TTF prices is down following the latest peace talks to end the Ukrainian war intermediated by the new US administration which would translate into potential return for Russian gas, less tightness and some relief to the European gas market. However, other geopolitical developments could have the opposite impact. For example, the resurgence of tensions in the Middle East with Israel resuming its war on Gaza and the escalation of tensions with Iran could result in higher gas prices. Moreover, the ambiguity surrounding the level, extent, and impacts of US tariffs against wide range of countries increases market uncertainty and add to market concerns.

Outlook

In the upcoming months, the gas market remains tight. Geopolitics continue to be the main driver for volatility especially with intended trade measures by the new US Administration affecting trade flows and growth. In addition, prices will be highly responsive to the advancement in peace talks between Russia and Ukraine. At the same time, the market will be watchful of the speed of storage refill, while it remains responsive to factors affecting demand in Europe or key LNG competitors in Asia, such as adverse weather conditions, along with any supply disruptions from key suppliers such Norway or the US.

As long as no peace deal for the Ukrainian war is reached, we expect prices to remain above their seasonal average in Q2 around 33 EUR/MWh. If a peace agreement is signed, we foresee TTF prices to decrease by at least 15% with lower volatility and less relevance of a storage timely refill. Our outlook for EU TTF year-ahead benchmark is summarized in the table below.

[1] The flexible storage plan is part of the European commission’s clean industrial deal that has lowering consumer energy prices as one of its key goals.