Fed to raise interest rates more rapidly

In its first policy tightening move since 2018, the Fed is widely expected to raise interest rates by 0.25% this coming Wednesday. We expect a total of seven interest rate rises in the course of 2022, as upside risks to inflation outweigh the downside risks to growth stemming from the Russia-Ukraine conflict.

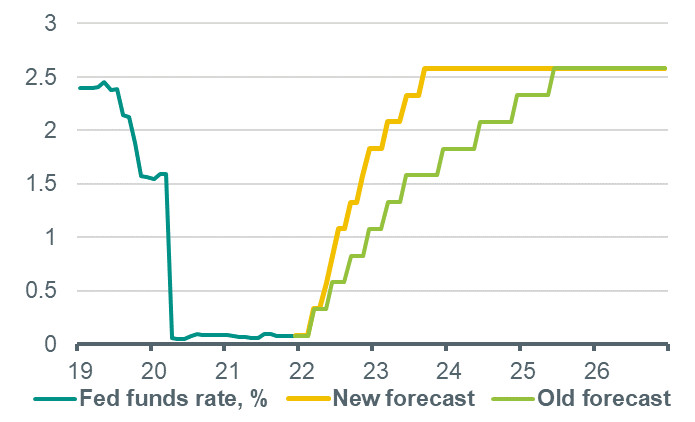

We now expect seven rate hikes in 2022

The US Federal Reserve meets this week for its March policy meeting, the outcome of which is this Wednesday, 16 March. We and consensus expect a 25bp hike, taking the target range of the fed funds rate to 0.25-0.50%. While there had been some expectation of a 50bp hike in March, market pricing of such a move has largely unwound since the Russia-Ukraine conflict broke out. However, it remains possible that some FOMC members might dissent and vote for a bigger move. Depending on how many such votes there are, this could stoke expectations for bigger moves in subsequent meetings. We think votes for a 50bp hike – if they happen – would be isolated to one or two members of the FOMC. We expect Fed Chair Powell to reiterate remarks from his Congressional testimony two weeks ago, when he said the Fed should be ‘careful’ with monetary policy in the current environment, i.e. indicating a preference for gradual (25bp) rises in the fed funds rate, though he continued to leave the door open for potentially bigger moves in future by saying the Committee is ‘prepared to hike faster if needed’. Indeed, on the spike in oil prices, he noted that while such moves typically do not have a lasting effect on inflation, that in the current environment there is a risk that it drives a further rise in inflation expectations. This is consistent with our view that, despite , the conflict makes the case even stronger for rate hikes, rather than weaker.

Given this, and alongside the persistent strength in inflation and wage growth in the US, we have brought forward significantly our rate hike expectations for the Fed; we now expect seven 25bp hikes this year, i.e. at every FOMC meeting, up from four previously. This would take the fed funds rate to 1.75-2.00% by December. For 2023, we continue to expect three rate hikes, in March, June and September. This means the Fed will reach our expectation for the terminal rate – 2.50-2.75% – already in the second half of next year, whereas previously we expected the Fed to reach this level over a year later, in early 2025. With this change to our Fed outlook, the risk around our forecast becomes more balanced, rather than tilted to the upside. On the upside, domestic inflationary pressure could prove to be more stubborn than we expect, even in the face of significantly tighter monetary and financial conditions; this could therefore require the Fed to raise rates beyond our expectation of where the terminal rate lies, and/or at a quicker pace. On the downside, the growth dampening effects of commodity price rises and the hit to real incomes could prove to be bigger than we expect, leading to a sharper reduction in demand-side inflationary pressures and to an increased risk of recession. This could cause the Fed to pause or reduce the pace of rate hikes if it judges the downside risks to growth as outweighing the upside risks to inflation. A severe tightening of financial conditions could also stay the Fed’s hand, although the bar for this continues to be much higher than in the past, given the imperative to bring inflation under control.

Fed to start shrinking balance sheet in May

Alongside the policy decision and Chair Powell’s accompanying remarks, another key focus for markets will be the publication of new macro and rates projections by the FOMC, as well as further guidance on how the Fed plans to start reducing its balance sheet. We expect upgrades to inflation forecasts and downgrades to growth forecasts on the back of recent developments. Rate hike projections are likely to increase significantly from the three 2022 hikes projected last December, but will probably fall short of the seven hikes we now expect this year. On the balance sheet, Powell indicated in his testimony that a decision on the pace of shrinkage would already come at the next FOMC meeting, one meeting sooner than he indicated in January. We continue to expect the Fed to begin allowing maturing bonds to roll off the balance sheet already in May, initially at a pace of $15bn per month, ultimately rising to a pace of $100bn per month by September. This is the maximum pace at which the balance sheet can unwind in a ‘passive’ manner. Although Powell has continued to reiterate the Fed’s preference for a balance sheet unwind that proceeds ‘in the background’, we continue to see a risk that the Fed engages in outright Treasury sales in order to speed up the process, depending on whether market conditions are conducive to this.