Eurozone - Paving the way for the first rate cut

First quarter GDP, released next week, is expected to be roughly stagnant. Disinflation in the eurozone remains on track, with inflation expected to be broadly back at 2% by the middle of the year. The ECB mentioned rate cuts explicitly in its policy statement, paving the way for a rate cut in June.

During the special European Council on 17-18 April, economic policy in Europe jumped to the top of the policy agenda. First, the by former Italian Prime Minister Enrico Letta on how to deepen the single market was published, while Mario Draghi gave a in which he teased some conclusions of his report on EU competitiveness, to be published later in 2024. To face global challenges and increase potential growth, the reports call for further integration and active industrial policy within the bloc. The reports are timely given the stagnation in the eurozone, but may fall on deaf ears given the European elections of early June will likely usher in a shift to the Eurosceptic/nationalist right.

Next week’s release of Q1 GDP growth in the eurozone will likely show ongoing stagnation in the economy. The outlook for the rest of 2024 however is improving, and growth is set to pick-up but stay below the trend rate. Private consumption is set to expand as high wage growth and falling inflation lifts real incomes, raising household confidence. Fiscal policy tightening and the still-high level of interest rates however will prevent a sharp recovery. As global trade volumes are picking up we expect this to feed through to a further bottoming out in the industrial sector, but structural headwinds such as high energy costs and decreased competitiveness are expected to keep the outlook subdued.

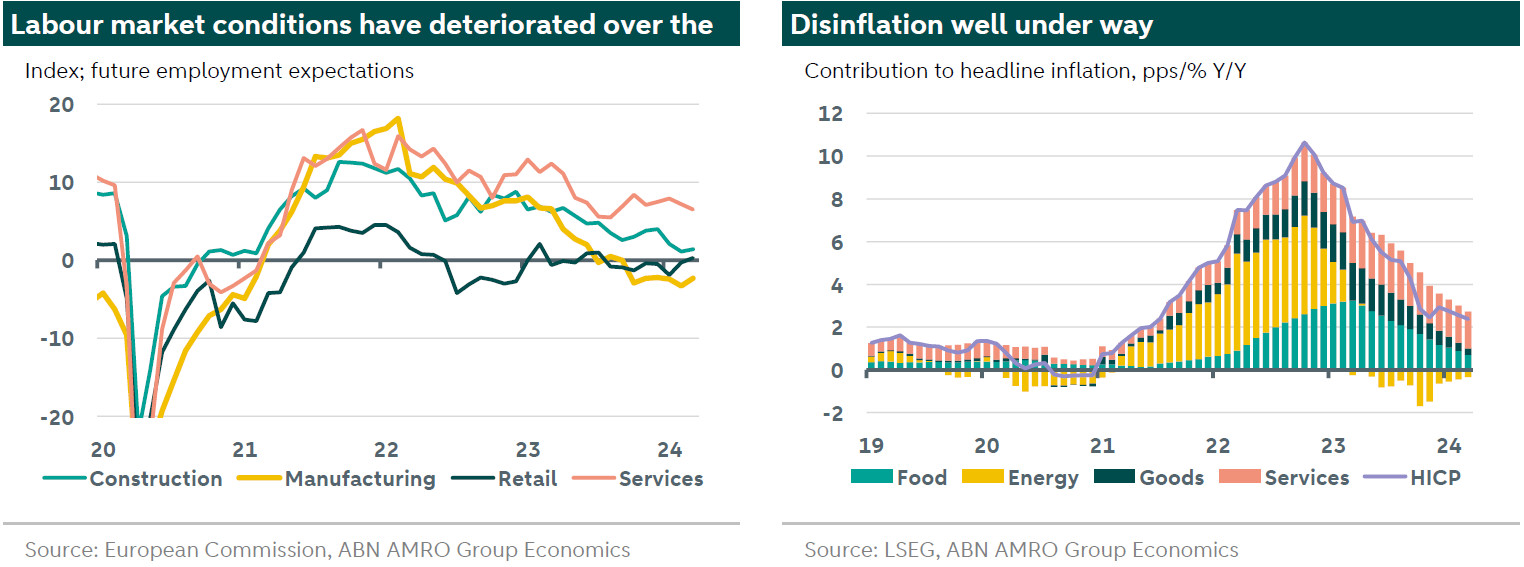

Disinflation in the meantime remains on track, with inflation still expected to be broadly back at 2% by the middle of the year. March inflation data actually surprised to the downside. Headline inflation fell to 2.4%, down from 2.6% in February, while core fell to 2.9% from 3.1%, the lowest reading since before the war in Ukraine. This was despite the timing of Easter in March this year instead of April. Easter typically puts some upward pressure on food and services inflation. With this effect absent from April onwards, services inflation is likely to softening further going forward. As indicated in a recent note (see here) we continue to expect wage growth to decline further in the coming quarters, as labour market conditions deteriorate, thereby weighing on services inflation going forward.

In the April meeting the ECB echoed the constructive outlook on inflation, indicating that ‘most measures of underlying inflation are easing, wage growth is gradually moderating and firms are absorbing part of the rise in labour costs in their profits’. Following this, in the April monetary policy statement the ECB explicitly mentioned rate cuts for the first time. It noted that if its ‘updated assessment of the inflation outlook, the dynamics of underlying inflation and the strength of monetary policy transmission were to further increase its confidence that inflation is converging to the target in a sustained manner, it would be appropriate to reduce the current level of monetary policy restriction’. Given the ECB’s communication on the inflation outlook, financing conditions and its view on underlying inflation mentioned above, these three conditions set by the ECB seem to have been largely met already (see here). As a result, we continue to think the ECB will start its rate cut cycle at the June meeting. While the ECB is not pre-committing to a particular rate path, our base case is that the ECB will cut rates at each meeting from June onwards for a total of 125bp rate cuts.