ESG Economist - What is the role of green ammonia in decarbonizing the world?

Ammonia is a highly toxic colourless gas with a distinct smell. It is composed of nitrogen and hydrogen. Ammonia can be produced in soil from bacterial processes and from the decomposition of organic matter. Only a very small percentage has been produced this way. Most ammonia is produced from natural gas and air. Natural gas molecules are reduced to carbon and hydrogen. The hydrogen is then purified and reacted with the nitrogen in the air to produce ammonia (Haber-Bosch process). This is called grey ammonia. If this method is combined with carbon capture and storage then this is called blue ammonia. The production of each metric tonne of grey ammonia contributes to the emission of roughly 1.9 metric tonnes of CO2 (1). Global ammonia production accounts for 1.3% of energy related CO2 emissions (2). According to the IEA, ammonia is one of the most emissions-intensive commodities produced by heavy industry, nearly twice as emission intensive as crude steel production and four times that of cement on a direct (scope 1) emissions basis. Another way of making ammonia is by using green hydrogen and nitrogen from the air. This is called green ammonia. Currently, around 70% of ammonia is used to make fertilisers with the remainder used for a wide range of industrial applications such as plastics, explosives and synthetic fibres. But it also has potential as a green energy carrier and as storage medium. In this report, we try to answer the question: What will the role of green ammonia be in decarbonising the world?

Ammonia is a carbon free fuel. It is composed of nitrogen and hydrogen. But it is a highly toxic, colourless gas with a distinct smell

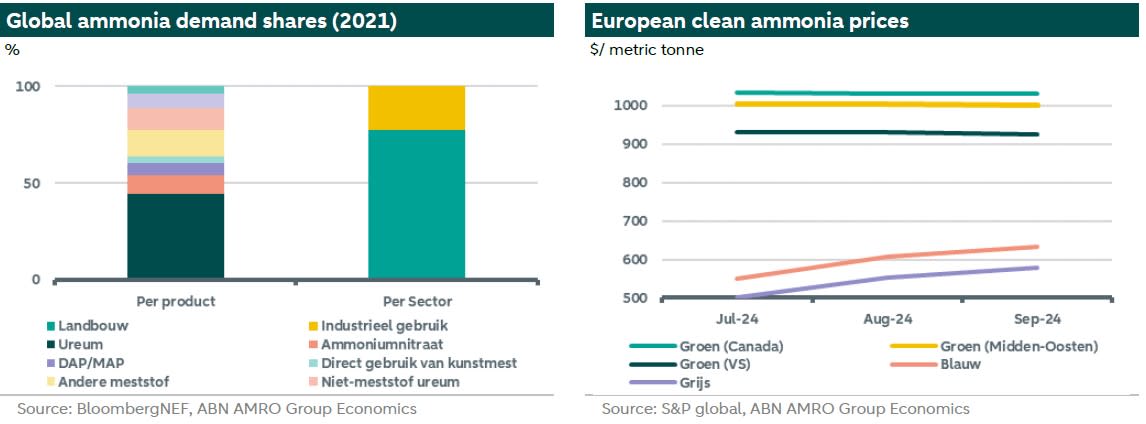

Global demand for ammonia comes to a large part from the agricultural sector, with a share of 77% for fertilizers, while only 23% is used for other industrial purposes

Ammonia has the potential to become an important zero-carbon fuel for maritime shipping, as an energy and transport carrier given its higher volumetric energy density compared to hydrogen…

…and it can also be used for power storage

Currently ammonia is produced via a mature technology (Haber-Bosch process, method of directly synthesizing ammonia from hydrogen and nitrogen)

Global ammonia production accounts for 1.3% of energy related CO2 emissions

Near-zero-emission production methods are emerging, but they have lower technical readiness levels

These routes to produce ammonia are far more expensive per tonne of ammonia produced than conventional ones depending on energy prices and other regionally varying factors

Currently supply of clean ammonia is low and there is considerable uncertainty around the projects but there is a large pipeline of sizable projects for the coming years

Supply also depends on demand. Demand will likely pick up if green ammonia becomes cost competitive

Renewable electricity is the main ingredient for producing green ammonia through electrolysis

Renewable electricity costs differ substantially in the EU making one country far more expensive than another

In 2023 the cost of green ammonia was still much higher than that of blue and grey ammonia in most countries. Grey ammonia may be impacted by higher carbon tax.

However, by 2030 green ammonia is expected to be cheaper than blue ammonia in all countries

Technologies

Currently ammonia is produced via a mature technology, but this emits a substantial amount of CO2 emissions. Near-zero-emission production methods are emerging, including electrolysis, methane pyrolysis and fossil-based technologies with carbon capture and storage (CCS) but they have lower technical readiness levels.

Several projects to produce ammonia with electrolytic hydrogen from variable renewable energy (VRE) are at advanced stages, but the variable renewable energy integration challenge remains. Therefore, the full chain of ammonia from variable renewable energy is assessed at TRL 8. According to the IEA, in the case of 100% electrolysis-based ammonia production, 2.5 times more electricity would be required in 2050 for ammonia production compared to the Net Zero Emissions by 2050 Scenario (3.5 times more than the Sustainable Development Scenario) (see more ).

The gasification of biomass or waste is also a possible technology option for near zero-emission ammonia production. But the biomass gasification for ammonia is still at the prototype stage (TRL 5). High costs and competition for sustainable biomass resources from other sectors make this technology route unlikely to play a large role (see more ). Despite this challenge there are some projects expected to reach final investment decision next year.

These emerging routes to produce ammonia are typically 10-100% more expensive per tonne of ammonia produced than conventional routes, depending on energy prices and other regionally varying factors. According to the IEA, existing and announced projects totalling nearly 8 Mt of near-zero-emission ammonia production capacity are scheduled to come online by 2030, equivalent to 3% of total capacity in 2020 (see more )

EU strategy for hydrogen-based fuels

Ammonia is a hydrogen-based fuel (see more here our ESG Economist on hydrogen). In June 2023, the European Commission adopted . The first act (see more ) defines under which conditions hydrogen, hydrogen-based fuels or other energy carriers can be considered as renewable fuels of non-biological origin (RFNBOs). Electrolysers to produce hydrogen will have to be connected to new renewable electricity production. The second act (see more ) provides a methodology for calculating life-cycle greenhouse gas emissions for RFNBOs. The methodology takes into account greenhouse gas emissions across the full lifecycle of the fuels, including upstream emissions, emissions associated with taking electricity from the grid, from processing, and those associated with transporting these fuels to the end-consumer (see more ). The two acts are inter-related and are both necessary for the fuels to be counted towards Member States' renewable energy targets. The new rules will apply to both domestic producers and international producers exporting green hydrogen to the EU (see more ). The focus is to accelerate the uptake of green hydrogen, ammonia and other derivatives in hard-to-decarbonise sectors, such as transport, and in energy-intensive industrial processes. Commission estimates that around 500 TWh of renewable electricity is needed to meet the 2030 ambition in REPowerEU of producing 10 million tonnes of renewable fuels of non-biological origin (RFNBOs). The 10 million metric tons by 2030 corresponds to 14% of total EU electricity consumption (see more ).

Demand for green ammonia

Global demand for ammonia comes to a large part from the agricultural sector, with a share of 77% for fertilizers, while only 23% is used for other industrial purposes. Zooming into specific products, urea production has the lion share with around 45% of all fertilizer production, followed by other fertilizers and non-fertilizer urea, with a proportion of 14% and 11%, respectively, as illustrated in the right-hand chart below. Noting that urea production requires CO2 as a feedstock. Ammonia has the potential to become an important zero-carbon fuel for maritime shipping, as an energy and transport carrier (see more on this below) given its higher volumetric energy density compared to hydrogen and it can also be used for energy storage.

The chart below (left) further depicts current price levels for green, blue and grey ammonia in Northern West Europe. The price of green ammonia is the lowest for that coming from the US. However, it remains more expensive compared to blue and grey ammonia. Grey ammonia is the cheapest in Europe today.

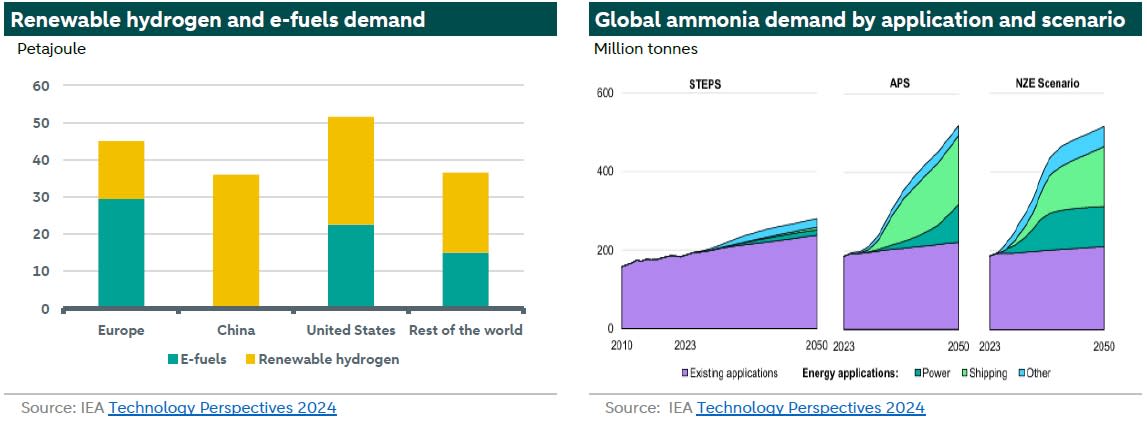

According to IEA, renewable hydrogen and e-fuels demand is expected to reach 45 PJ (see chart below) in order to meet RED III targets for RFNBO, ReFuelEU Aviation targets.

Furthermore, the IEA emphasize the role of offtake agreements for the maritime sector ammonia demand, which are estimated currently at 40PJ globally (see more ).

At the same time, global ammonia demand for energy applications is expected to increase widely along the transition horizon especially for power (storage) and shipping sectors under Announced Policies (APS) and Net Zero Emission (NZE) Scenarios, as illustrated in the right-hand chart below.

Shipping case for ammonia

Shipping carries close to 80-90% of global trade. According to the EU's EDGAR database, international shipping accounted for 1.4% of global greenhouse gas emissions in 2023. Achieving significant reductions in emissions of international maritime transport requires using both less energy (increasing energy efficiency) and cleaner types of energy (using renewable and low-carbon fuels).

On 7 July 2023, the International Maritime Organization (IMO) revised its strategy on the reduction of greenhouse gas emissions from ships. The strategy identified levels of ambition for the international shipping sector noting that technical innovation and the global introduction and availability of zero or near-zero GHG emission technologies, fuels and/or energy sources for international shipping will be integral part to achieving the overall level of ambition. The levels of ambition and indicative checkpoints should take into account the well-to-wake GHG emissions (also including methane) of marine fuels as addressed in the guidelines on lifecycle GHG intensity of marine fuels (LCA guidelines).

Since January 2024 the EU Emission Trading System (ETS) has been extended to all ships of 5,000 gross tonnage and which enter the EU ports. EU ETS is based on tank-to-wake (TtW) emissions and will initially only cover CO2 emissions. However, from 2026 methane and nitrous oxide emissions will also be included. Additionally, in January 2025 FuelEU Maritime, which aims to promote the use of renewable and low-carbon fuels will come into force. Non-compliance with the regulations will have a direct financial impact for ship owners. FuelEU Maritime tightens requirements on well-to-wake (WtW). GHG intensity limits for fuel consumed on board compared to the 2020 reference limit – and methane emissions are included from day one.

So the shipping industry is moving towards energy carriers with lower life cycle emissions such as green ammonia, biofuels, methanol and LNG (transition fuel). In this report we focus on green ammonia. Ammonia as a shipping fuel has many advantages such as no CO2 emissions when combusted as it is a carbon free fuel but also a lot of challenges. We start with the advantages.

Advantages of ammonia as a shipping fuel

One of the promising alternative shipping fuels to achieve International Maritime Organization’s (IMO) GHG emission goals is green ammonia. According to IRENA, it is estimated that reductions of life cycle GHG emission would be between 83.7% and 92.1%. Moreover, it is easier to store and to transport because ammonia becomes liquid at more ambient temperatures compared to hydrogen fuel. In addition, ammonia has a significantly higher energy volumetric density than hydrogen. This is the energy density per unit volume. So ammonia could be a good alternative for the shipping sector as it has more similarities to conventional fossil fuel sources in terms of physical characteristics (it is simple to store and transport), and as opposed to e-methanol, the production cost of e-ammonia does not depend on the costs associated with carbon capture and removal technology because it has a no-carbon content in its molecular structure.

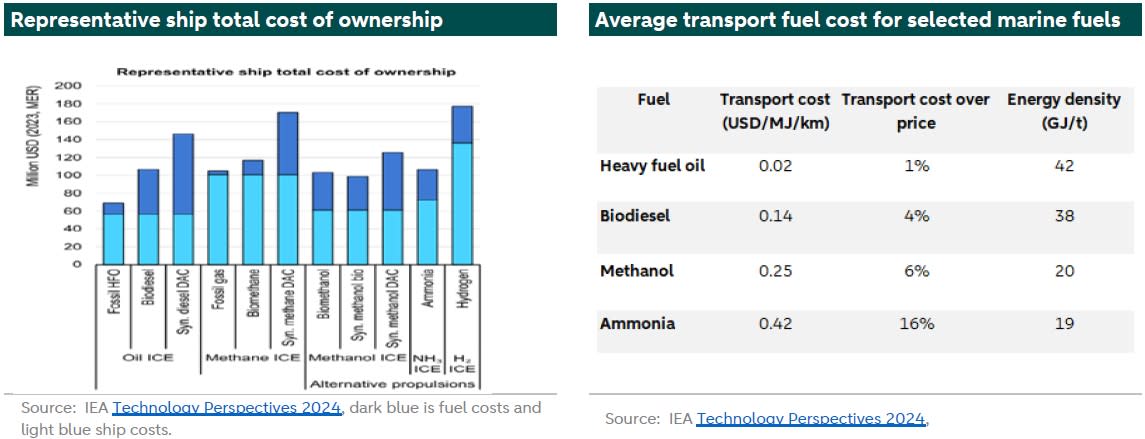

The graph below depicts the total cost of ownership of ships in the IEA Announced Pledges Scenario (APS) in 2035. The chart shows that using ammonia in an internal combustion engine is considerably cheaper than hydrogen, synthetic methanol (via direct air capture or DAC) and synthetic methane. The chart further illustrates that an ammonia ship typically requires a higher upfront investment than a methanol ship. This is the light blue part of the bar. On the short/mid-term ammonia is competing more with LNG and biofuels, however LNG will not be a long-term alternative as emission reduction targets (including methane) will increase.

Disadvantages of ammonia as a shipping fuel

But there are also disadvantages to ammonia as the future shipping fuel. First ammonia ranks lowest as a transport marine fuel with the highest transport cost and lowest energy density compared to heavy fuel oil, biodiesel and methanol (see table above on the right - graphs in the download).

Second, ammonia-fuelled ships would require between 1.6 and 2.3 times the volume of fuel compared to conventional heavy fuel oil ships. So compared to heavy fuel oil, ammonia weighs twice as much and requires three time more space to contain the same amount of energy. This needs to be considered when designing new vessels.

Third, ammonia is currently produced via natural gas so the life cycle greenhouse gas emissions are high. Even when you try to reduce emissions by having grey ammonia replace heavy fuel oil as a shipping fuel, the total life cycle emissions are still high. Therefore, ammonia should only be considered as shipping fuel if it is produced with low life cycle emissions such as green ammonia.

Fourth, ammonia can be used as a fuel for fuel cell and for an internal combustion engine. In the latter case, due to its poor ignition properties ammonia needs pilot fuels to trigger combustion in an internal combustion engine. But current technology for both ammonia fuel applications, fuel cells and internal combustion engines, are still in the development and research stages, with few real-world applications in the shipping industry at present. According to the IEA, ammonia-fuelled ship engine has a TRL of 6 (large prototype) and ammonia solid oxide fuel cell electric ship a TRL of 4-5. MAN Energy Solutions plans to deliver first engine fuelled by ammonia for installation on a new vessel in Japan and will be ready to offer ammonia-powered engines to its clients after 2027 (see and ).

Finally, using ammonia comes with safety challenges – such as low flammability, corrosion and toxicity (IRENA) and nitrous oxide (N2O) and potential ammonia slip. Ammonia slip refers to the unreacted ammonia that goes into the atmosphere. Due to its toxicity, the introduction of ammonia as fuel creates new challenges related to safe bunkering, storage, supply and consumption. Bunkering refers to the supply of fuel for use by ships including the logistics of loading and distributing the fuel among available shipboard tanks. Bunkering can be done ship-to-ship, truck-to-ship and terminal to ship and all these ways have advantages and disadvantages (see more ). The infrastructure needs to be built up. The main hurdles for using ammonia as a marine fuel is that it is a highly toxic and corrosive gas, and its use can lead to NOx and N2O emissions. However, the fact that ammonia has been used as a refrigerant gas for decades highlights that industry actors have gained significant expertise in handling it safely (see more ).

The storage case for ammonia

Recently we wrote an ESG Economist on energy storage (see more here). One of the types of energy storage is chemical storage. Chemical energy storage is energy stored in the form of chemical fuels that can be readily converted to mechanical, thermal or electrical energy for industrial and grid applications (see more ). Examples of chemical fuels are hydrogen and ammonia. Hydrogen allows the energy to be stored indefinitely. But there are challenges to hydrogen such as low round-trip efficiency of around 30-40%, much below that of other storage technologies. Hydrogen can function as chemical energy storage, but it can also be transformed into methane and ammonia. Ammonia is another potential energy carrier. There is an existing infrastructure due to its widespread use as fertilizer, but it has serious safety issues. The technical readiness levels of chemical energy storage ranges from 6 to 9.

The challenges around using ammonia for storage purposes are reflected by its low adoption in current hydrogen projects. Within a survey among hydrogen valleys in Europe, almost 22% of respondents identified ammonia as a key technology to store produced hydrogen. However, 85.4% of respondents (41 respondents) are storing hydrogen in a form of compressed hydrogen.

Supply for green ammonia

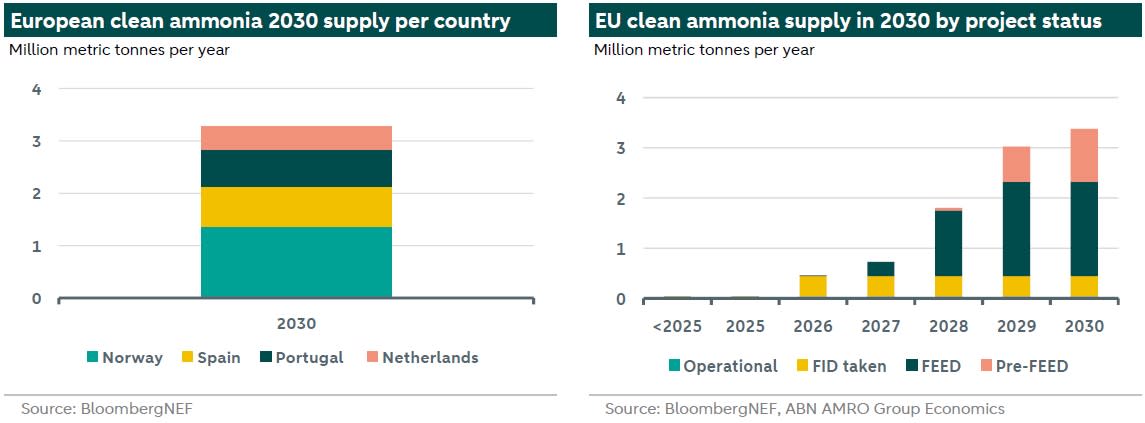

According to BloombergNEF, and based on tracked projects, most of European clean (both thermochemical and electrolysis) ammonia supply is expected to take place in Norway, with around 1.37 mmt, followed by Spain, Portugal, and the Netherlands, respectively (see left-hand chart below). However, we note that most large-scale projects for green ammonia are located outside Europe, with total European supply in 2030 representing only 10.4% of expected global supply.

More precisely, there are around 3.4 mmt of announced clean ammonia projects in Europe towards 2030, as illustrated in the chart above (right). However, only 1% of these projects are currently operational while 12% with a taken FID (final investment decision), leaving more that 87% at the FEED (front end engineering design) and Pre-FEED stages. This keeps a looming uncertainty around the realization of these projects, especially in the case of insufficiency or late emergence of demand. Thus, the challenge is to secure offtake contracts and financing for this potential production. We note that almost 20% of planned European clean ammonia capacity is based on thermochemical technology, while the remaining 80% rely on electrolysis, while most of the European announced clean ammonia projects are intended for existing uses and for shipping.

Globally, clean ammonia supply could reach 32.5 mmt by 2030, according to BloombergNEF. Policies aiming to incentivize demand such as quotas, tax credits and (import) subsidies are essential to incentivize supply and develop the market further. With current incentives, BloombergNEF estimates the trade of clean ammonia of around 11 million tons.

Infrastructure

Near-zero emissions ammonia and methanol can, in principle, be produced almost anywhere in proximity to low-cost clean electricity, water and, for methanol, CO2. There are already ports that have export terminals for these fuels, creating a window of opportunity for ports located in areas with large renewable energy resources and the required infrastructure to become major suppliers. However, having an export terminal for these fuels is not sufficient to become a low-emissions bunkering centre: first, low-emissions fuels must be available and separately stored from conventional products; second, dedicated refuelling infrastructure needs to be developed.

Additionally, new infrastructure must be deployed at a rapid speed to reach the goals of clean ammonia in time. More specifically, different transition scenarios require sharp increases in electrolyser capacity and CO2 transport and storage infrastructure by 2050. This means that installation rate for electrolysers and large capture projects (annual capture, transport and storage capacity of 1 Mt CO2 or more) need to increase substantially between now and 2050.

Costs

When comparing natural gas-based reforming production with and without CCS and electrolytic-based ammonia production, natural gas-based reforming without CCS is unsurprisingly the least-cost option in most energy price contexts and in the absence of a CO2 price. The cost of adding CCS to natural gas-based reforming is relatively modest. It increases the levelized cost of ammonia production by about 25% in typical energy price contexts and would require a CO2 price of about USD 30/t CO2 to start being cost-competitive with unabated natural gas reforming. Policies other than explicit carbon prices could similarly spur the addition of CCS, such as CO2 emission regulations or technology subsidies. Electrolysis-based ammonia production can compete with natural gas reforming in a wider limited range of contexts but is most likely to do so when electricity prices are low, natural gas prices are high and electrolyser costs low. Even in the case of low electrolyser costs, electricity prices of USD 40/MWh or lower are needed for electrolysis to become competitive. In regions with high natural gas prices (USD 10/MBtu), electrolysis could already become competitive with electricity prices of around USD 40/MWh. Such low electrolysis costs require considerable reductions in the cost of electrolysers relative to today – in the order of 60% reductions to reach about USD 400/kWe electrolyser capacity. Without such reductions in electrolyser costs, even lower electricity prices of USD 20-25/MWh would be needed. In regions with lower natural gas prices, electrolysers at today’s costs may require electricity prices below USD 5/MWh to be cost-competitive (see more ).

The chart above shows the average levelized production costs across regions (left) under the IEA’s Announced Policies Scenarios (APS). The EU has the highest cost for producing ammonia in the world mainly because of high costs of electricity, followed by North Africa with highest CAPEX costs. But there are cost competitive countries in the EU. At the same time, ammonia ranks lowest as a transport marine fuel with the highest transport cost and lowest energy density compared to other alternative fuels.

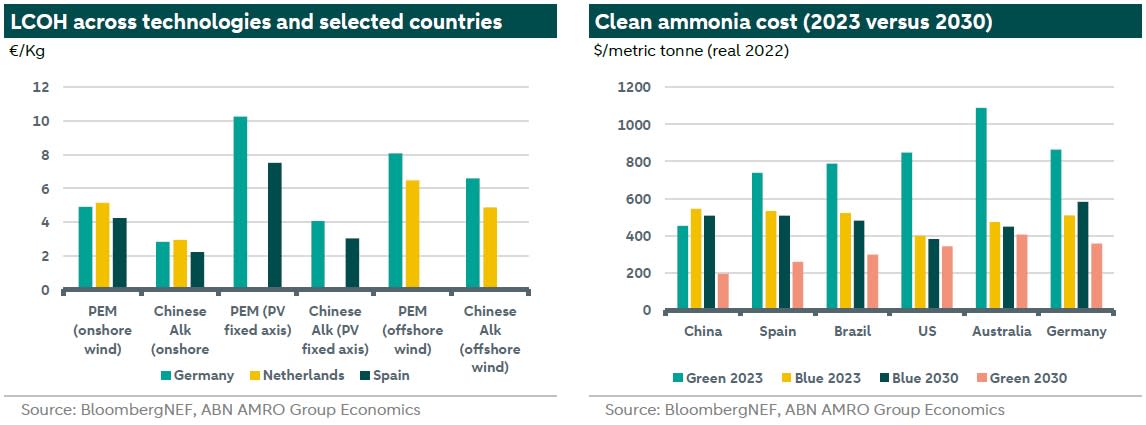

Furthermore, the cost of green hydrogen is one of the components for the cost of green ammonia. The chart below (left) shows the Levelized Cost of Hydrogen or LCOH across selected European countries, distinguishing between PEM and Chinese Alkaline electrolysers and the source of renewable power. In the EU, the LCOH is lowest for hydrogen projects using Chinese Alkaline electrolysers regardless of the source of renewable power, while projects using onshore wind power are the most competitive. This is true for all selected countries with the lowest cost in Spain. Electrolysis powered through offshore wind are most competitive in the Netherlands. Read more about green hydrogen in our previous note here.

In 2023 the cost of green ammonia was still less competitive than grey ammonia in most countries. However, by 2030 green ammonia is expected to be cheaper than blue in all countries (see right-hand chart above). Furthermore, it is expected to reach cost parity with grey ammonia in Germany by 2030, while only Brazil, Spain, and China will witness lower cost of green ammonia compared to grey.

Supporting the production of clean ammonia

There is a role for all stakeholders in accelerating the production of clean ammonia. Governments’ role is essential by designing targeted policies for clean ammonia that help reduce emissions and support the creation of a level playing field for a global market for clean ammonia, along with accelerating R&D and incentivise end-use efficiency for ammonia-based products. At the same time, ammonia producers should embrace the coming change by transitioning towards more sustainable technologies. Farmers could adopt better practices for more efficient use of fertilizers. Financial institutions and investors could use sustainable investment schemes to support deployments of technologies and infrastructure. Research and development activities should continue the improvement and innovation of new and promising technologies.

Conclusion

Ammonia is a carbon free fuel. It is composed of nitrogen and hydrogen. But it is a highly toxic, colourless gas with a distinct smell. Global demand for ammonia comes to a large part from the agricultural sector, with a share of 77% for fertilizers, while only 23% is used for other industrial purposes. Ammonia has the potential to become an important zero-carbon fuel for maritime shipping, as an energy and transport carrier given its higher volumetric energy density compared to hydrogen and it can also be used for energy storage. Currently ammonia is produced via a mature technology (Haber-Bosch process, method of directly synthesizing ammonia from hydrogen and nitrogen), but this process emits substantial amount emissions. Near-zero-emission production methods are emerging, but they have lower technical readiness levels. These routes to produce ammonia are far more expensive per tonne of ammonia produced than conventional ones. Currently supply of clean ammonia is low and there is considerable uncertainty around the projects but there is a large pipeline of sizable projects for the coming years. Supply also depends on demand. Demand will likely pick up if green ammonia becomes cost competitive. Renewable electricity is the main ingredient for producing green ammonia through electrolysis. Renewable electricity costs differ substantially in the EU making one country far more expensive than another. In 2023, the cost of green ammonia was still much higher than that of blue and grey ammonia in most countries. However, by 2030 green ammonia is expected to be cheaper than blue ammonia in almost all countries, while only Brazil, Spain, and China are expected to witness lower cost of green ammonia compared to grey.