ESG Economist - Dutch agriculture not on track to meet climate targets

It is well known that the agricultural sector is important in achieving net-zero emissions in 2050. Within the totality of all climate sectors, the agricultural sector occupies a special place. This is because the sector is capable of removing excess carbon from the atmosphere from other sectors. In addition, this sector almost directly faces the negative impacts of climate change in its business activities. With that, the sector benefits from targeted climate action. But the sector itself also has a major challenge to reduce its greenhouse gas emissions in the coming years. In this analysis, we first look at the situation of the agricultural sector in an EU perspective in relation to greenhouse gases and where the Netherlands stands. Then we look in more detail at the main sources of greenhouse gas emissions for the Dutch agricultural sector specifically. Furthermore, we discuss the trend of fossil energy consumption in the sector and CO2 emissions. Finally, we show a possible emission reduction path towards 2050 for this sector. The reason we outline this trajectory is to give our customers and stakeholders a better picture of how realistic the climate targets currently are. This insight helps to better understand and also follow the trajectory, but above all to make it clear what awaits us in the coming years.

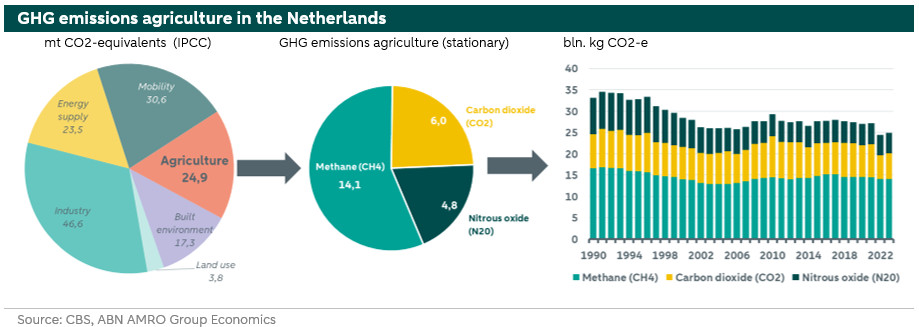

The agriculture sector is responsible for 24.9 Mt of CO2 equivalents in 2023 and this is equivalent to about 18% of annual greenhouse gas emissions in the Netherlands

According to the ESA regulation, the Netherlands must achieve a 48% reduction in emissions by 2030, compared to 2005 levels; this will ultimately also include the agriculture sector

There is still much uncertainty about the feasibility of this target for the agriculture sector

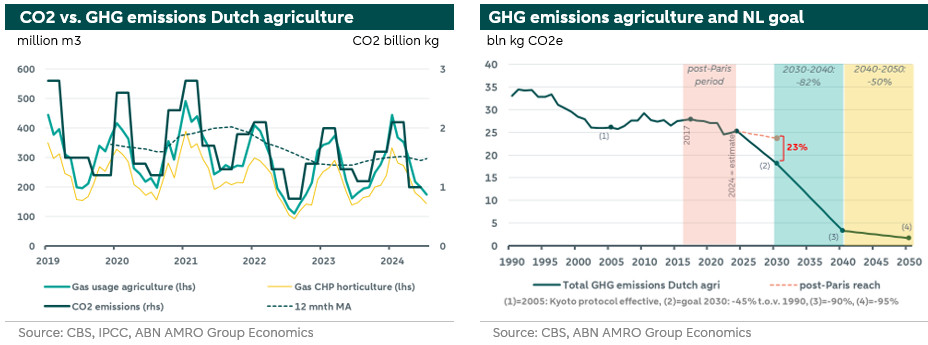

In the first 7 months of 2024, gas consumption in the sector increased by 6% year-on-year, but is still about 20% below pre-energy crisis levels (2021)

This means that a reduction in total greenhouse gases in the sector in 2024 is not likely

Based on the post-Paris trend growth, the 2030-target for the Dutch agricultural sector will not be reached, with a gap of 23%

The whole trajectory for the agriculture sector towards 2030 requires more commitment and a coordinated approach throughout the chain at all levels

Moreover, it is important that the implementation of decarbonisation options or new policy rules is done on a business-economically sound basis

Agriculture in the EU

Agriculture is one of the sectors most exposed to and directly affected by climate change. This primary production sector is highly dependent on the natural environment with many of its existing agricultural activities. Changes in temperature and precipitation patterns, as well as more extreme weather events, pose major challenges for the sector. However, the agricultural sector itself is also responsible for greenhouse gas emissions, thus contributing to climate change.

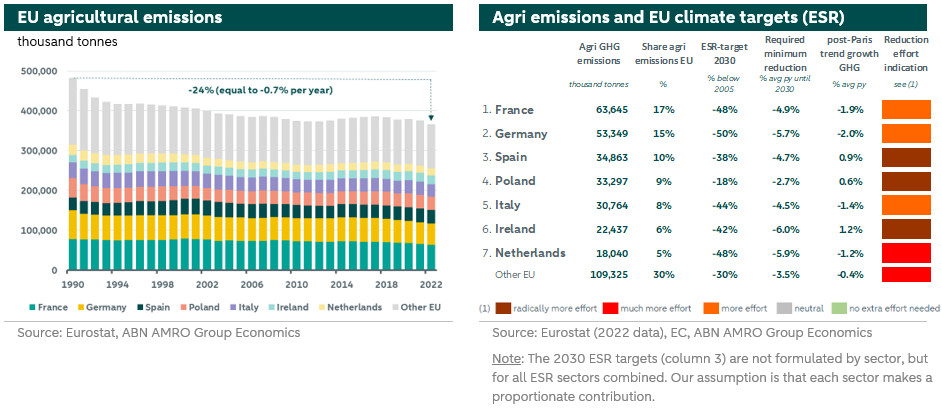

In Europe, the agricultural sector (excluding forestry and fisheries) accounts for 14% of total EU greenhouse gas emissions. These greenhouse gas emissions have decreased by 24% since 1990, or an average of 0.7% per year. France, Germany and Spain are the top 3 largest agricultural emitters, with the Netherlands occupying position 7. The top 7 countries with the most agricultural greenhouse gas emissions have a combined share of 70% of total EU agricultural emissions.

All countries in the EU are bound by the Effort Sharing Regulation (ESR), which will culminate in ETS-II. The ESR regulation sets a specific percentage reduction in greenhouse gas emissions for each EU member state by 2030 compared to 2005. These emission reductions apply to companies and sectors not covered by ETS-I. Under ESR (ETS-II), these sectors are: domestic transport (excluding aviation), buildings, the agricultural sector, small industry and waste. The ESR emission reduction rate varies by EU country and is based on gross domestic product (GDP) per capita in member states. Overall, emissions covered by ESR account for almost 60% of total EU emissions.

According to the ESR regulation, the Netherlands must achieve a 48% reduction in greenhouse gas emissions by 2030, compared to 2005 levels. Specifically, it means reducing emissions by at least 5.9% per year through 2030. This also applies to the agricultural sector, excluding greenhouse horticulture. In fact, a majority of the Dutch parliament is in favour of including greenhouse horticulture in ETS-2, only if all parties in the Energy Transition Covenant Greenhouse Horticulture 2022-2030 agree. The reason for not including greenhouse horticulture in ETS-II is that many proposed fiscal measures could well help the sector become more sustainable. This is according to a tariff study by Berenschot and Kalavasta (September 2024).

The overall task for the whole agriculture sector seems very challenging, as the sector has managed to reduce its greenhouse gas emissions by only 1.2% per year in the post-Paris period (2017 to now). A sharp acceleration is thus needed to eventually reach the target. In countries such as Spain, Poland and Ireland, however, the agricultural climate target is even more out of reach. More radical climate measures need to be taken.

Agriculture and GHG emissions in the Netherlands

The agriculture sector (stationary processes, meaning excl. mobility) is responsible for 24.9 Mt of CO2 equivalents in 2023, and this is equivalent to about 18% of annual greenhouse gas emissions in the Netherlands. There is a difference in greenhouse gas emissions in the agricultural sector compared to other sectors. Methane is responsible for a much larger share of greenhouse gas emissions. In other climate sectors, this is often CO2. Emissions through livestock (fermentation by cattle; 91% share), manure stock and escaping unburned natural gas (horticulture) have a large impact on the sector's total greenhouse gas emissions.

Methane emissions in the Netherlands are mainly caused by the agricultural sector. The sector accounts for some 62% of total methane emissions in the Netherlands. But waste processing also has a significant share at 21%. The rest comes from natural processes and from consumers. The National Methane Strategy (November 2022) states that methane emissions must be reduced by 30% by 2030 compared to 2020. This plan describes on a national level how the Netherlands will implement the methane plan ‘Global Methane Pledge’ as a result of COP 26 in 2021.

There are several ways to reduce methane emissions. In February 2022, for example, an innovative feed additive that reduces methane emissions from livestock farming was approved by the European Commission. This feed additive suppresses the enzyme in a cow's stomach that causes methane production. According to the feed additive's producer, it can reduce methane emissions by about 30% for cows. However, the net effect and actual impact on methane reduction is yet to be investigated. Next to that, de-fertilisation on a daily basis combined with green gas production from manure fermentation can also help reduce methane emissions. This also reduces CO2 emissions in the other sectors by allowing this green gas to replace fossil gas as fuel. Other possibilities include changes in food rations or developing animals that emit less methane. Several (international) projects are currently under way to identify the most efficient, feasible and cost-effective way to reduce methane.

CO2 emissions are mainly due to gas consumption in greenhouse horticulture. According to Glastuinbouw Nederland, the greenhouse horticulture sector is aiming for fossil-free cultivation in 2040. Among other things, this means replacing natural gas with green gas by 2040, supplemented by other decarbonisation options. Replacing natural gas with hydrogen for combined heat and power (CHP) is also a possibility, although this is still in the development phase. Finally, the more intensive use of other heat sources (such as ground and residual heat) is also an option to reduce CO2 from the sector.

Changing land use also affects greenhouse gas emissions. For instance, soil is - after the oceans - the largest carbon reservoir or sink. Then, in order to preserve soil fertility and fight climate change, it is important that soil health receives a lot of attention. In this context, one should then think, for example, about minimising tillage, increasing soil cover and organic matter and planting trees.

Fossil usage trend in agriculture

Total emissions from the agricultural sector are a sum of emissions from livestock, land use changes and energy consumption. Natural gas consumption has a major role in the total energy consumption of the agricultural sector. For each subsector within the agricultural sector, the level of energy consumption depends on different indicators.

In livestock farming, energy consumption is closely related to the number of animals present and form of farming. In arable farming, it depends on the amount of crops grown and also the type of crop. In addition, the use of fuels (such as diesel) for machinery, fertiliser production and, for example, onion and potato storage also produces CO2 emissions. On balance, any energy saving through, for example, implemented energy efficiency measures will result in savings for the farm, especially with today's relatively high energy prices. It reduces costs and responds to social sustainability and environmental issues.

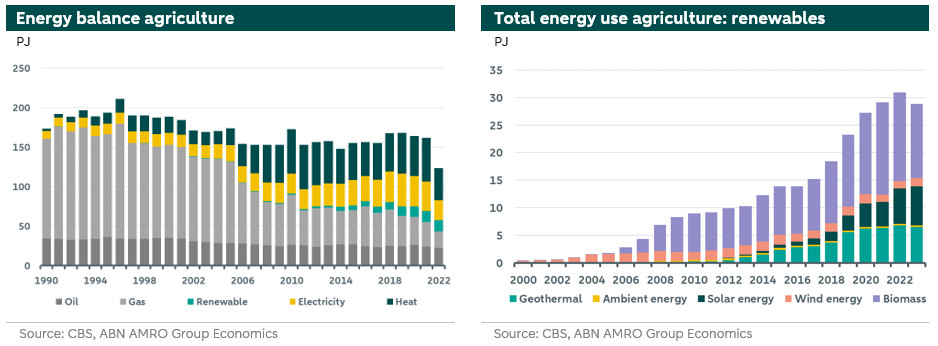

Since 1990, fossil fuel consumption in the sector has decreased significantly. Especially less natural gas consumption in particular has been influential, while petroleum consumption has only slightly decreased over the years. The decline in natural gas consumption has led to an increase in electricity, heat and, after 2010, increasingly renewable energy.

The share of the agricultural sector in total renewable energy supply is around 21% in 2023 and in final energy consumption it is 9%. Ten years ago, this was only 6% versus 2%. However, the sector has much more growth potential, given the space available for onshore wind turbines and solar panels on barn roofs. In total renewable energy consumption, biomass (such as biogas and other biofuels) has the largest share by 2023, at 46%. Solar energy follows with a 24% share and then geothermal with 22%. In the total generation of energy by solar power in the Netherlands, the agricultural sector had a 10% share in 2023. It is still relatively low, but this source has also been growing rapidly in recent years. Most solar power is generated in the province of North Brabant, followed by Gelderland. And that while most electricity deliveries take place in the provinces South Holland and North Holland, especially for horticulture. In this segment, relatively many initiatives are taking place with geothermal heat, using underground heat from deeper strata of the earth to heat greenhouses.

The deployment of renewable energy within the agricultural sector to reduce greenhouse gas emissions is a key component for the overall sector to get on to the path of net zero by 2050. As a result, the growth of renewable initiatives is going to intensify in the coming years.

The total consumption of natural gas in the agricultural sector is dominated by greenhouse horticulture. This consumption has a strong correlation with CO2 emissions, as shown in the left figure below. Due to the double dip caused by the pandemic and the energy crisis (2020-2022), gas consumption and CO2 emissions decreased more sharply. But after these crisis moments, an upward trend in both indicators is visible again. The positive signal from a climate perspective is that pre-crisis levels have not yet been reached.

The route to a climate-neutral agricultural sector can be via the reduction of emissions on the supply side (especially by measures in livestock farming and greenhouse horticulture), via adjustments in the demand for agricultural products, but also by removing greenhouse gases via negative emissions, such as reforestation or increasing carbon sequestration in agricultural soils (‘Carbon Farming’) or natural areas.

To cope with greenhouse gas emissions - but at the same time also partly with the nitrogen crisis - discussions are ongoing on reducing livestock numbers, implementing stricter manure rules and reducing nitrogen deposition in the Netherlands. Especially the problems in the manure market are getting a lot of attention. A manure law was recently passed which reduces the number of phosphate and animal rights per permit (the number of animals you are allowed to keep on a farm according to the licence), which will shrink the livestock population and thus indirectly improve the living environment (such as air and water quality). Any drastic reduction in livestock numbers is going to further reduce greenhouse gas emissions (methane) and also allow for a large part of land use to be redesigned. However, the implications of this for the dairy sector in the Netherlands, for example, could be huge.

IPCC data show that greenhouse gas emissions increased by 2% year-on-year in 2023. And in the first seven months of 2024, gas consumption in the sector increased by 6% year-on-year. The increase is steep, but ultimately total gas consumption in the sector is still about 20% below pre-energy crisis levels (2021).

Given the strong link between gas consumption and CO2 emissions, a further reduction in total greenhouse gases in the sector by 2024 seems unlikely. This makes the need for an acceleration in climate-resilient agricultural practices clear, if there is still a chance of achieving all set climate targets towards 2030 and beyond. In doing so, the European climate goals remain leading. For the sector - as for many other sectors - the set EU goals towards net-zero are ambitious and often not within reach, as shown in the right-hand figure above. In the post-Paris period (2017-now), greenhouse gas emissions in the overall sector have fallen by an average of 1% a year. Projecting this rate to the period 2025 to 2030, it becomes clear that the 2030 target will not be reached. Indeed, there would be a 23% gap. The targets after 2030 are thus far out of reach. Opportunities to reduce emissions seem sufficiently available to the sector (see also our publication ).

Despite the fact that the path to the 2030 and 2050 climate targets is very steep, the sector can still take major steps forward. For instance, the sector remains at the forefront of deploying sustainable energy production techniques such as solar panels, geothermal, biomass plants, windmills, residual heat utilisation and manure fermentation on a larger scale. This transformation will continue in the coming years and hopefully at a faster pace. The whole journey to 2030 and beyond requires more commitment and a coordinated approach throughout the chain at all levels anyway: from farms, food producers, consumers, financiers and both national and regional governments.